Introduction to Finance: Class 8

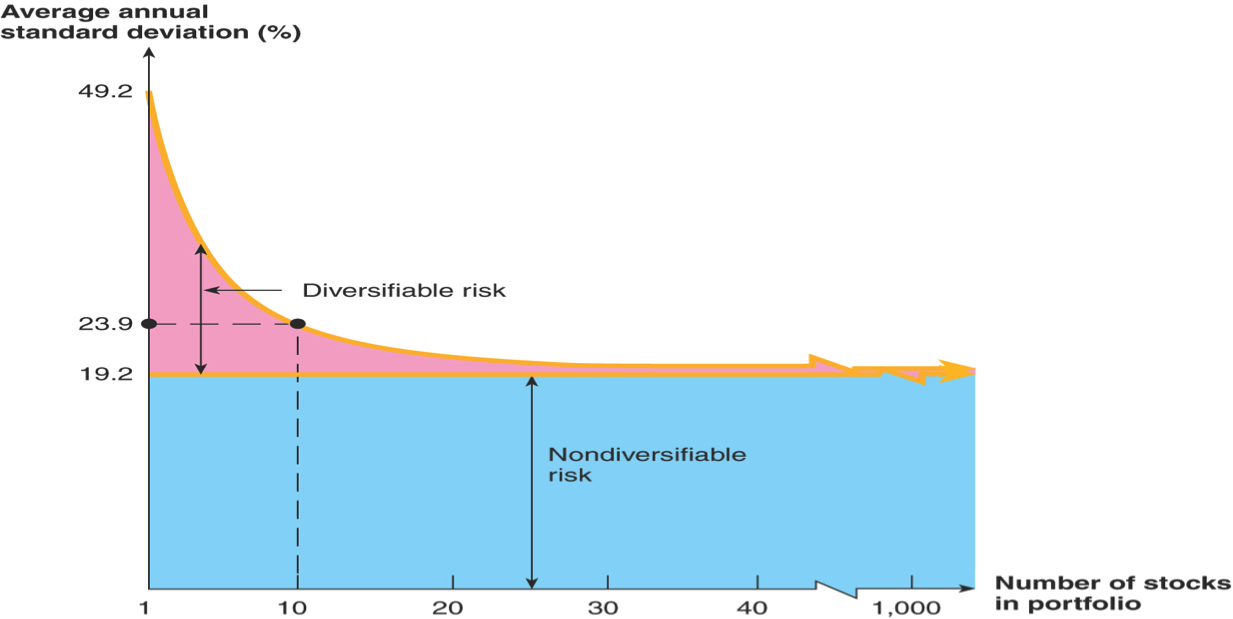

Introduction to Finance: Class 8 Risks & Returns What are risks & returns? When it comes to financial matters, we all know what risk is -- the possibility of losing your hard-earned cash. And most [...]

If you didn't find what you were looking for, try a new search!

Introduction to Finance: Class 8 Risks & Returns What are risks & returns? When it comes to financial matters, we all know what risk is -- the possibility of losing your hard-earned cash. And most [...]

Introduction to Finance: Class 7 Lessons from Capital Market History What is a capital market? Capital markets channel savings and investment between suppliers of capital such as retail investors and institutional investors, and users of capital [...]

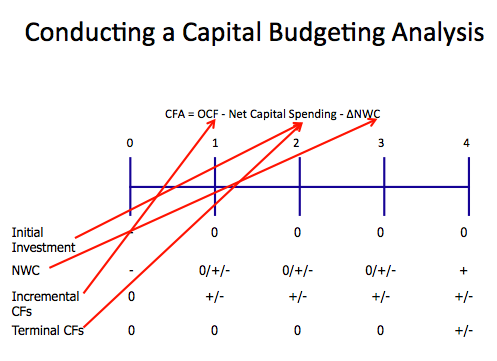

Introduction to Finance: Class 6 Making Capital Investment Decisions Where to begin? Capital investment decisions also can be called ‘capital budgeting’ in financial terms. Capital investment decisions aim includes allotting the capital investment funds of the firm [...]

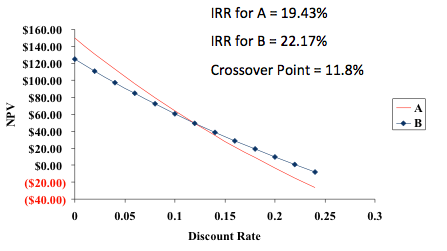

Introduction to Finance: Class 5 Net Present Value & Other Investment Criteria What is net present value? The difference between the present value of cash inflows and the present value of cash outflows. NPV is [...]

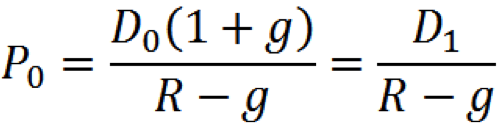

Introduction to Finance: Class 4 Stock Valuation What is stock valuation? There are many ways to determine the value or worth of a stock (refamiliarize yourself with what a stock is). Each stock is different, [...]

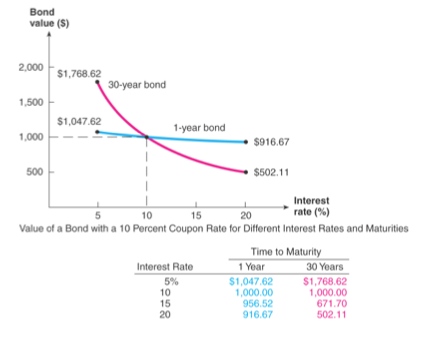

Introduction to Finance: Class 3 Bonds & Interest Rates What are bonds? What is an interest rate? Check this out: Introduction to Bonds Video Interest Rates Video Key Concepts: Bonds Bond Basics Why Bonds? Bond [...]

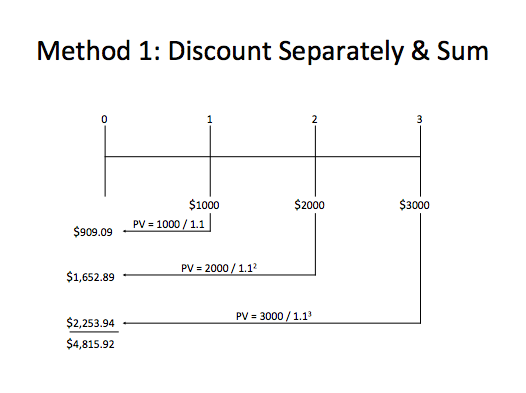

Introduction to Finance: Class 2 Discounted Cash Flow Valuation What is a discounted cash flow valuation? Discounted cash flow (DCF) is a valuation method used to estimate the attractiveness of an investment opportunity. DCF analysis [...]

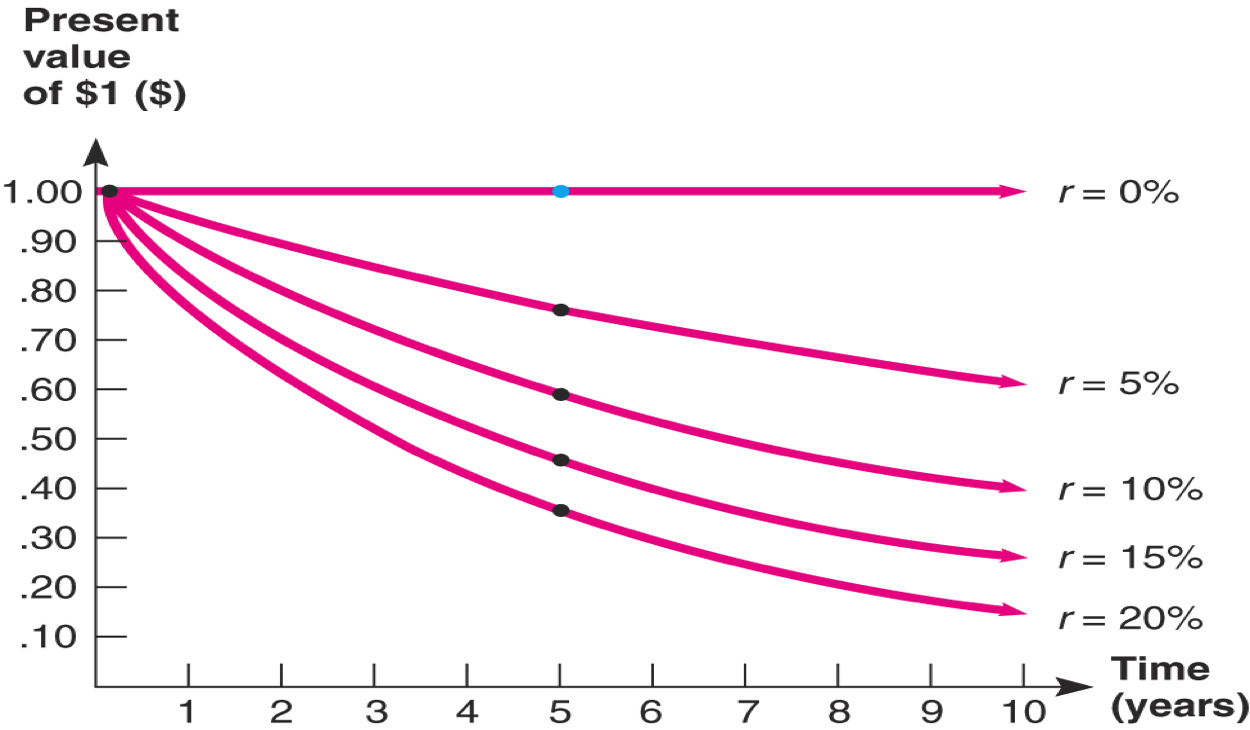

Introduction to Finance: Class 1 Time Value of Money What is the time value of money? Simply put, the value of money is dependent upon time. The purchasing power of money varies with time. Time [...]

In the first part of our series, “Introduction to Behavioral Finance – Part 1: Behavioral Bias,” we explored several market anomalies, and the first required condition for the real-life implementability of many quantitative strategies: the existence of human behavioral biases. In this Part 2 of our series, we consider a related question following from our Keynes example: given that certain behavioral biases can affect investors, how can it be that their effects persist in markets so we can take advantage of them? This would seem to contravene the notion of efficient markets, and leads to the second required condition for implementing a tradable strategy: limits to arbitrage.

In this blog post, Part 1 of our two part series on Behavioral Finance, we explore human behavioral biases, how they affect us as investors, and how they are reflected in the stock market. In Part 2 of our series, we will explore the second required ingredient for profiting from behavioral bias: Limits of Arbitrage. Human behavior is diverse and complex and, unfortunately, despite our best intentions, it is not always governed exclusively by rationality. In particular, our judgment and decision-making can be significantly affected by intuition, a form of abstract, automatic thinking that can override our reason. Decades of research in psychology have shown that intuition is often systematically biased, and follows identifiable patterns, causing us to reach conclusions that are predictable wrong, since they are based on our gut or instincts, rather than on logic. An important aspect of behavioral biases is that they affect us in areas of our lives where it is very important that we be purely rational, such as in investing. In this blog post, we highlight a number of behavioral biases, and specifically how they can affect investors. Before getting into the specifics, we wanted to review some background we hope will be informative, and put the biases into an appropriate investing context.