We’ve outlined the fundamentals of long-term return projection models in a recent post:

http://alphaarchitect.com/2012/12/projected-15-year-sp-500-returns/

Butler|Philbrick|Gordillo and Associates have a great post that focuses on the “Shiller” or “Hussman” models for return forecasting

http://gestaltu.blogspot.com/2013/04/valuation-based-equity-market-forecasts.html

Empiritrage has a detailed report outlining a more sophisticated way of forecasting long-term returns:

Here is some chart porn:

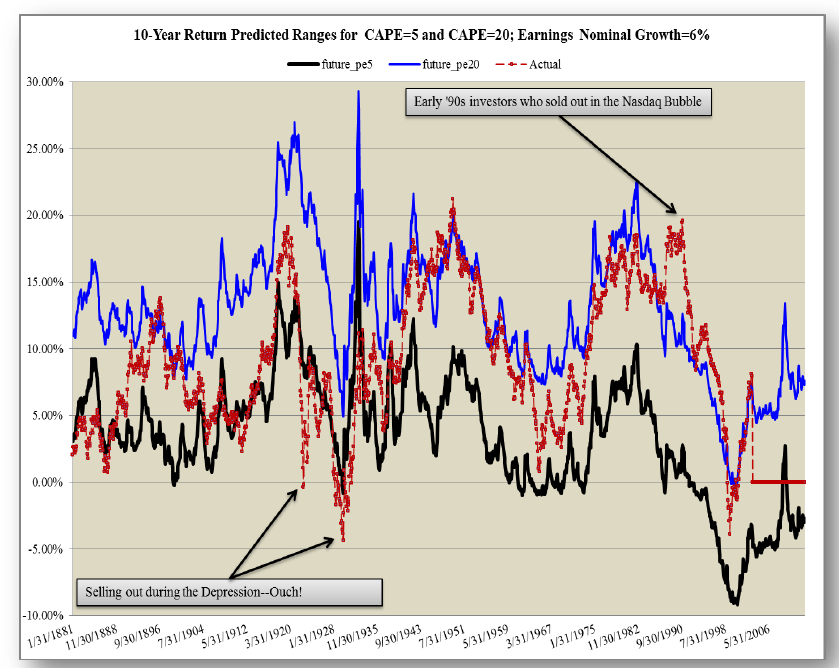

First, a look at the “Hussman” model for long-term returns. This model assumes a peak-to-peak earnings growth, inputs the current P/E and div yield, and then generates low and high return bounds based on future P/Es.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

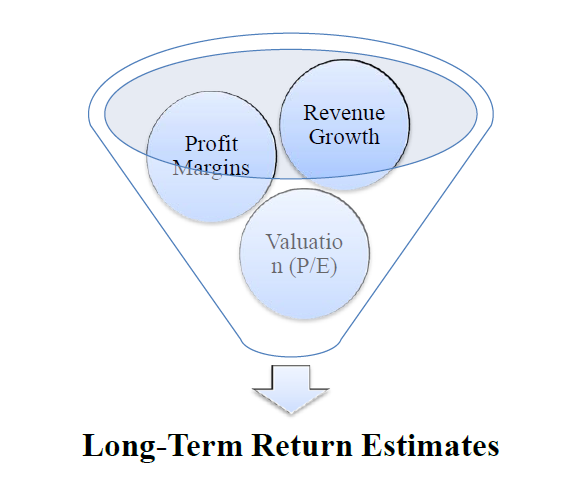

Another approach is to model the dynamics of revenue growth, profit margins, and valuations, and then simulate what the economy might look like under certain assumptions. The benefit of this approach is the incorporation of mean-reverting profit margins and valuation ratios directly into the model.

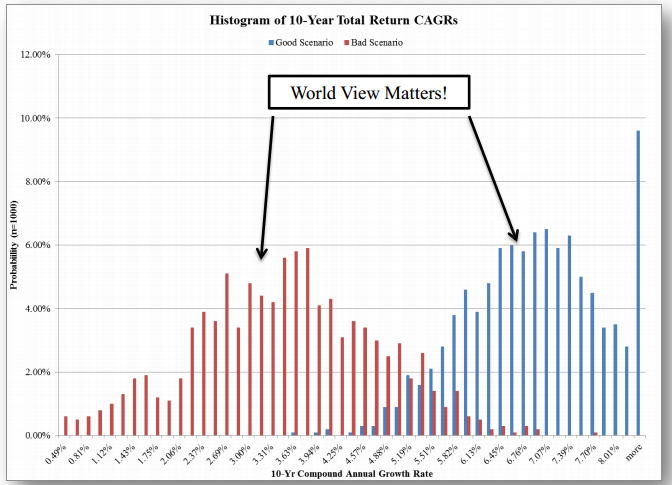

Here are some baseline results:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.