As technology increasingly marginalizes the use of physical money, the rise of virtual currencies, as alternatives to national fiat currencies, is perhaps inevitable. And if you are not living under a rock, by now you have heard of the king of virtual currencies: Bitcoin, a form of electronic money that can be used to purchase goods and services from growing numbers of retailers, or even converted into cash.

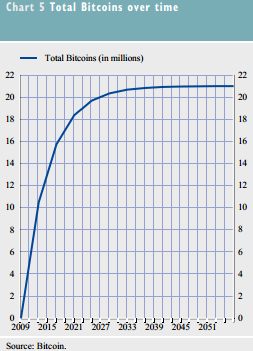

When Bitcoin was first created back in 2009, there were 21 million Bitcoins that were digitally hidden in mathematical blocks that could be unlocked by solving algorithms through a CPU-intensive, repetitive trial-and-error process. In this sense, the digital “mining” of Bitcoins is quite similar to the extraction from the earth of physical commodities, such as gold, copper, ore, or coal.

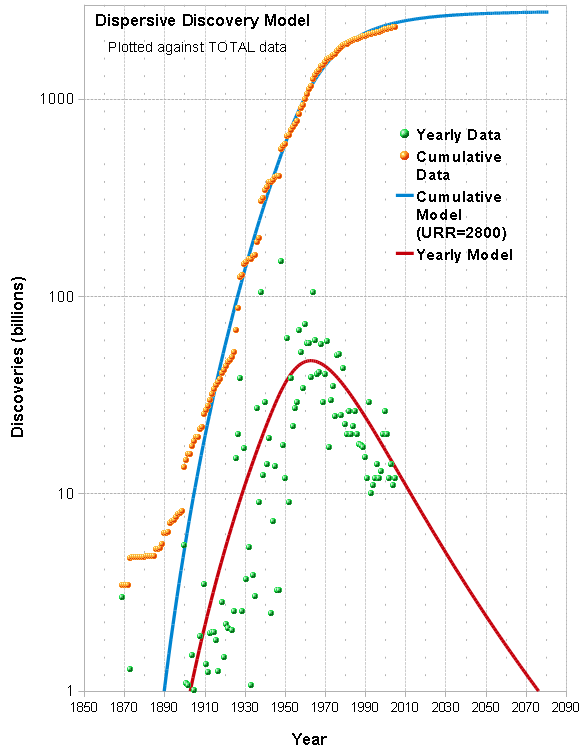

In physical mining, miners always target the highest quality, most easily accessed reserves first, in order to maximize their profits. Over time, as the resource gets depleted, mining conditions become more challenging, margins get squeezed and the rate of production shrinks, as miners must go to ever greater lengths to obtain a given amount of the commodity. Eventually, the resource becomes fully depleted, and no further production is possible.

Bitcoin mining is similar: as the easy reserves are mined out, the rate of mining decreases geometrically , with an approximately 50% reduction every four years. The number of Bitcoins is set to reach a limit of 21mm Bitcoins somewhere around 2040.

Compare the graph above to the cumulative production curve for oil, another commodity that today is moving along a similar development/resource depletion curve:

An obvious feature of commodities generally is that resources are finite, which eventually must lead to decreases in the rate of production (as indicated in the graphs above). For example, with respect to oil, many are likely familiar with “Hubbert’s Peak,” (the peak in the red oil production rate curve, above) which describes the notion that the rate of U.S. oil production peaked around 1970.

It is often said that Bitcoin’s commodity-like market structure, with its finite supply, appeals to libertarians of the Austrian School of economics, who believe inflation relates to growth of the money supply, rather than to an increase in the general price level.

Ludwig Von Mises believed a critical feature of any successful medium of exchange is that it must have a high stock to flow ratio: that is, the incremental creation of new monetary units must be low relative to existing holdings. Certainly this will be increasingly true for Bitcoin; ultimately, if the number of Bitcoin units is capped, at that point there should be no inflation.

Austrian School adherents like that Bitcoins are not produced by central banks (which can’t indiscriminately produce them). Bitcoins also have the advantage that they are not backed by any government (which may fail to honor its commitments), and don’t comply with financial laws (which might lead to their unfair confiscation). Instead, Bitcoin uses proof-of-work systems, and cryptography to facilitate peer-to-peer transactions.

So what are the economics with respect to mining Bitcoins? A recent Arstechnica article suggests that the returns are strong: http://arstechnica.com/gadgets/2013/06/how-a-total-n00b-mined-700-in-bitcoins/

According to the author, the Butterfly Labs Bitcoin miner can yield 0.1 Bitcoin per hour. Taking this back-of-the-envelope estimate, and plugging in a recent Bitcoin exchange rate, we get:

Aye caramba! This seems too good to be true. There are certainly risks to consider, including liquidity and, increasingly, legal risks, which call into question whether Bitcoin is a reliable source of value.

Additionally, if the Bitcoin price crashes, or mining becomes more expensive, mining may be quickly rendered unprofitable at current electricity rates.

While we have our doubts, others are more sanguine. Consider that the Winklevoss twins, of facebook fame, have filed with the SEC to create a Bitcoin

ETF: http://calvinayre.com/2013/07/02/business/winklevoss-twins-file-bitcoin-trust-with-the-sec/.

We look forward to watching from the sidelines as Cameron and Tyler take their shot with Bitcoin.

Regardless of how it plays out, as with their Facebook adventure it promises to be entertaining.

About the Author: David Foulke

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.