Equity Issuance and Returns to Distressed Firms

- James L Park

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our free Academic Alpha Database!

Abstract:

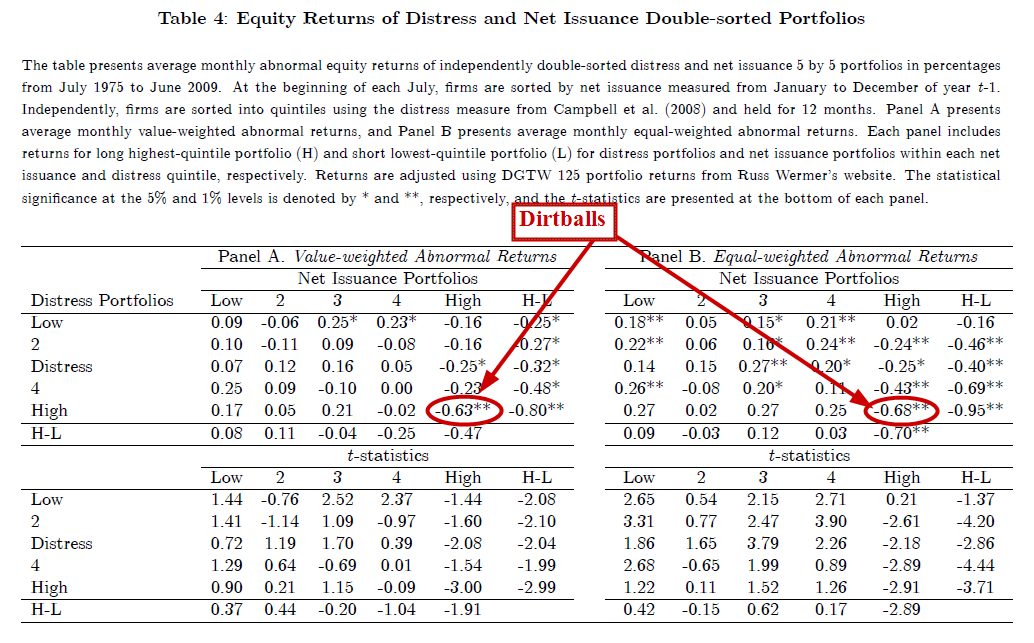

Previous literature is inconclusive about whether distressed firms issue equity. Using a portfolio approach to all traded firms, I find a strong positive relationship between distress and equity issuance. When the cross-section of firms is sorted by degree of distress, the mean monthly net issuance rate increases monotonically from 0.10% for the safest decile portfolio to 1.13% for the most distressed. Using a large database that includes both public and private issuance, I find that the hump-shape distribution of public issuance and the monotonically increasing distribution of private issuance together represent the increasing CRSP issuance population in the cross-section of distress. Moreover, I find that the low abnormal returns of distressed firms are concentrated in those firms that issue the most equity. Thus, the positive relationship between equity issuance is important in understanding the equity issuance and return patterns of distressed firms.

Data Sources:

SDC Platinum and Placement Tracker. CRSP/Compustat. 1975-2009

Alpha Highlight:

Distressed high equity issuance stocks are terrible for your investment health.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Strategy Summary:

- Calculate distress using logit estimates from Campbell et al.

- Calculate issuance.

- Identify the most distress and the highest issuance.

- Avoid these stocks like the plague.

Commentary:

- Complicated methodology.

- Can one make money on the short side?

Who wants to buy distress issuers?

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.