A Survey of Low Volatility Strategies

- Tzee-man Chow, Jason C. Hsu, Li-Ian Kuo, and Feifei Li

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our free Academic Alpha Database!

Abstract:

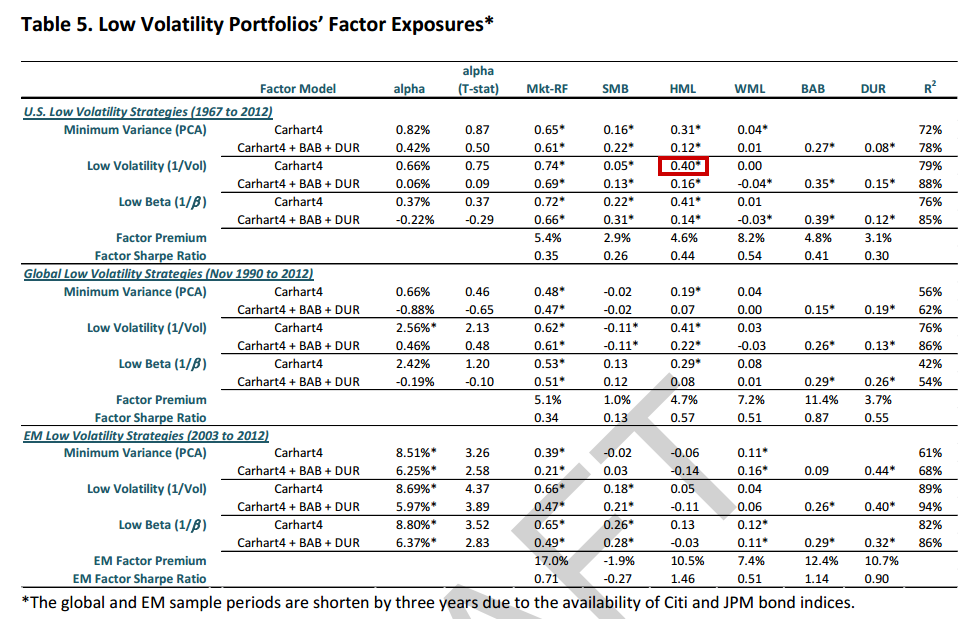

This paper replicates various low volatility strategies and examines their historical performance using U.S., global developed markets, and emerging markets data. In our sample, low volatility strategies outperformed their corresponding cap-weighted market indexes due to exposure to the value, betting against beta (BAB), and duration factors. The reduction in volatility is driven by a substantial reduction in the portfolios’ market beta. Different approaches to constructing low volatility portfolios, whether optimization or heuristic based, result in similar factor exposures and therefore similar long-term risk-return performance. For long-term investors, low volatility strategies can contribute to a considerably more diversified equity portfolio which earns equity returns from multiple premium sources instead of market beta alone.

While the lower risk and higher return seem persistent and robust across geographies and over time, we identify flaws with naïve constructions of low volatility portfolios. First, naïve low volatility strategies tend to have very high turnover and low liquidity, which can erode returns significantly. They also have very concentrated country/industry allocations, which neither provide sensible economic exposures nor find theoretical support in the more recent literature on the within-country/industry low volatility effect. Additionally, there is concern that low volatility stocks could become expensive, a development which would eliminate their performance advantage. This highlights the potential danger of a portfolio construction methodology that is unaware of the fundamentals of the constituent stocks — after all, low volatility investing is useful only if it comes with superior risk-adjusted performance. That many naïve low volatility portfolios are no longer value portfolios today bodes poorly for their prospective returns. More thoughtful portfolio construction research is necessary to produce low volatility portfolios that are more likely to repeat the historical outperformance with reasonable economic exposure and adequate investability.

Data Sources:

CRSP/Datastream

Alpha Highlight:

Lose access to value premium, lose access to excess returns?

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Strategy Summary:

- Outlines methodolgy to construct low-volatility portfolio

- This low volatility portfolio has higher CAGR, lower volatility, and higher Sharpe ratio compared to Cap-Weighted benchmark.

- However, there are numerous downfalls for the low volatility strategy. They include:

- Large tracking error relative to the benchmark (around 9-10% in the U.S.).

- Overweighting specific sectors compared to the benchmark. Low volatility portfolios have exposures to around 4.75 sectors in the U.S., as opposed to 9.59 sectors for the benchmark.

- Higher turnover (from 19-45% for low volatility strategies in U.S. compared to 4.42% for benchmark).

- Low volatility strategies trade less liquid stocks (comparing Bid-Ask spread in table 6).

Commentary:

- Interesting thoughts and analysis on the “low volatility” anomaly

- Nice discussions and rebuttals from Eric Falkenstein:

Is low volatility a value strategy in drag?

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.