A Re-Examination of the Super Bowl Stock Market Predictor

- Jeffery A. Born and Yousra Acherqui

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our free Academic Alpha Database!

Abstract:

Krueger and Kennedy (1990) [KK] were the first to empirically document the remarkable stock market predictive power of the winner of the Super Bowl. The “model” predicts that the stock market would rise when the Super Bowl is won by a team from the old NFL, but would fall if the game was won by a member of the old AFL. This model correctly predicted the direction of five different market indices 20 times in the first 22 games (91% accuracy). An examination of the subsequent 24 games finds the model no longer possess abnormal predictive ability. When we examine the model’s returns earned after the winner of the Super Bowl is known, we find them reduced, especially in the period examined by KK. We also find the ability of the SBPM to predict the direction of subsequent change in the SP500 and the DJIA collapses to virtually zero since the publication of the KK article.

Data Sources:

N/A

Alpha Highlight:

The super bowl tactical asset indicator “works”…until it doesn’t…

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Strategy Summary:

- Paper re-examines the Super Bowl Prediction model (SBPM) documented in 1990.

- Prediction is that markets will rise if a member of the “old NFL” wins the game, while markets will decline if a member of the “old AFL” wins the game.

- Paper finds the following:

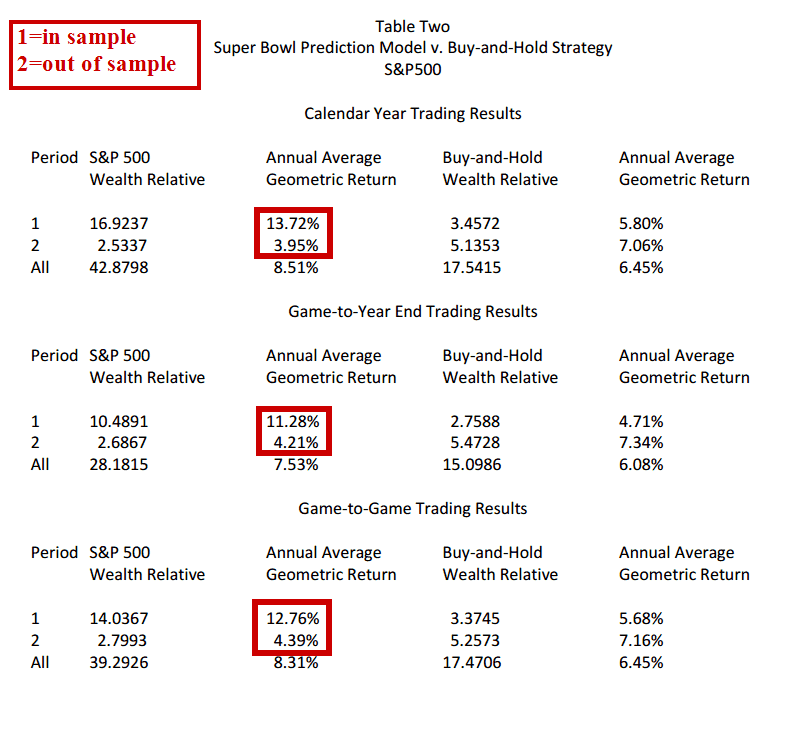

- During the original sample period (1966-1987) the SBPM (13.72% CAGR) outperforms a simple buy-and-hold strategy (5.80% CAGR) in the SP500.

- However, this was partly driven by the January effect. The original prediction assumed buying or selling at the close of Dec. 31st of year t based on the winner of the game in year t+1.

- One way to correct for this would be to have the model buy/sell the day after the game, and hold until the end of the year or until the winner the next year. When only holding until the end of the year, the CAGR for the original time period falls (1966-1987) from 13.72% (when including the returns from Jan 1 until the game) to 11.28%.

- During the more recent time period (1988 – 2012), the SBPM (3.95% CAGR) underperforms a simple buy-and-hold strategy (7.06% CAGR) for the SP500.

- Results are similar for the DJIA, with the SBPM outperforming in the first time period, while the simple buy-and-hold outperforms in the more recent time period.

- Last, paper finds (not surpirisingly) that the winner of the game does not Granger cause (statistical test of causality) market performance, and that the market performance does not Granger cause the winner of the game.

- During the original sample period (1966-1987) the SBPM (13.72% CAGR) outperforms a simple buy-and-hold strategy (5.80% CAGR) in the SP500.

Commentary:

- Paper highlights how the January effect can influence returns to random strategies.

- Shows how causality tests (Granger causality) can be used to explain which way the causation goes (or in this case, confirm our intuition that a winner of a football game should not effect the stock market and vice versa!).

Go Cowboys!

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.