Every quarter, boards across America wrestle with the complex question of dividend policy.

Perhaps the company has excess cash that should be paid out as a dividend? Or perhaps cash should be directed to high NPV projects? It’s a nuanced debate, which is why we were somewhat surprised to see a recent Slate article that reached a categorical conclusion: “Dividends are Evil.”

The Slate article describes dividends as a “strictly inferior option to using corporate cash on a share buyback.” As the article points out, however, “In comparing buybacks with dividends, the only real disadvantage is that buybacks look unattractive when stock market prices are relatively high.”

This latter point (buybacks for high-priced stocks are unattractive) is certainly true. Consider what happened to GE in the late 2000s. During 2007, GE repurchased approximately $12 billion in stock, when it traded in the $35-$40 per share range. Next, during the 2008 crisis, GE reissued $12 billion of stock at approximately $22 per share. That was pretty clearly a value-destroying round trip for GE shareholders.

Today, GE trades at a 4.4% EBITDA/EV yield, which strikes us as pretty expensive. Given the high price, and the black eye GE received on the 2007-08 equity round trip horror show discussed above, we don’t think it would be unreasonable for GE not to pursue a buyback at current prices.

The Slate article continues:

A CEO could, of course, simply admit that his company’s share price is high already and so the time has come for patience. But with executive compensation excessively linked to short-term stock price movements managers rarely have an incentive to call for patience.

The impatient move that would benefit the economy would be for a cash-rich firm with an already high share price to invest. Hire more people and do more stuff, upgrade the training of your existing workforce, reward your better employees with raises and bonuses so they don’t go elsewhere, cut prices to build customer loyalty. That’s how profits lead to rising incomes, and how rising incomes lead to demand for the stuff businesses sell.

It seems reasonable to infer that the author would agree a share repurchase by GE at current prices is probably a poor use of capital. We know that GE recently raised its dividend by 16%, and it also seems reasonable to infer that the author would think this too is a bad idea.

So what should GE do with that cash? The article suggests it would make sense to invest that capital, instead of paying it out in the form of dividends. The logic is that if GE simply invested more, that would result in higher earnings for the company and the best economic outcome overall (assuming GE has positive NPV projects). In a struggling economy, investment will drive a recovery. This seems reasonable.

So do lower dividend payouts tend to increase earnings growth, thus supporting the economy?

Quant heavyweight Cliff Asness has observed that in times of low payout ratios (thus low dividends), in the aggregate, market observers often predict that this implies higher earnings growth in the future. Conversely, in times when payout ratios are high, and capital is paid out instead of reinvested, earnings should grow slowly in subsequent years.

Again, this logic seems to make sense: if companies retain earnings and plow them back into promising projects, earnings growth should be higher in the future; conversely, if companies don’t see any growth opportunities, they will push cash back to shareholders and future earnings shouldn’t experience robust growth.

Stories are great, and all humans grave a coherent narrative, but is this really how the world works from an empirical standpoint?

One thing we like about Asness is that he is an empiricist. In a 2001 paper, “Does Dividend Policy Foretell Earnings Growth?” Robert Arnott and Asness weigh in with some evidence related to the question of how payout ratios affected subsequent earnings growth.

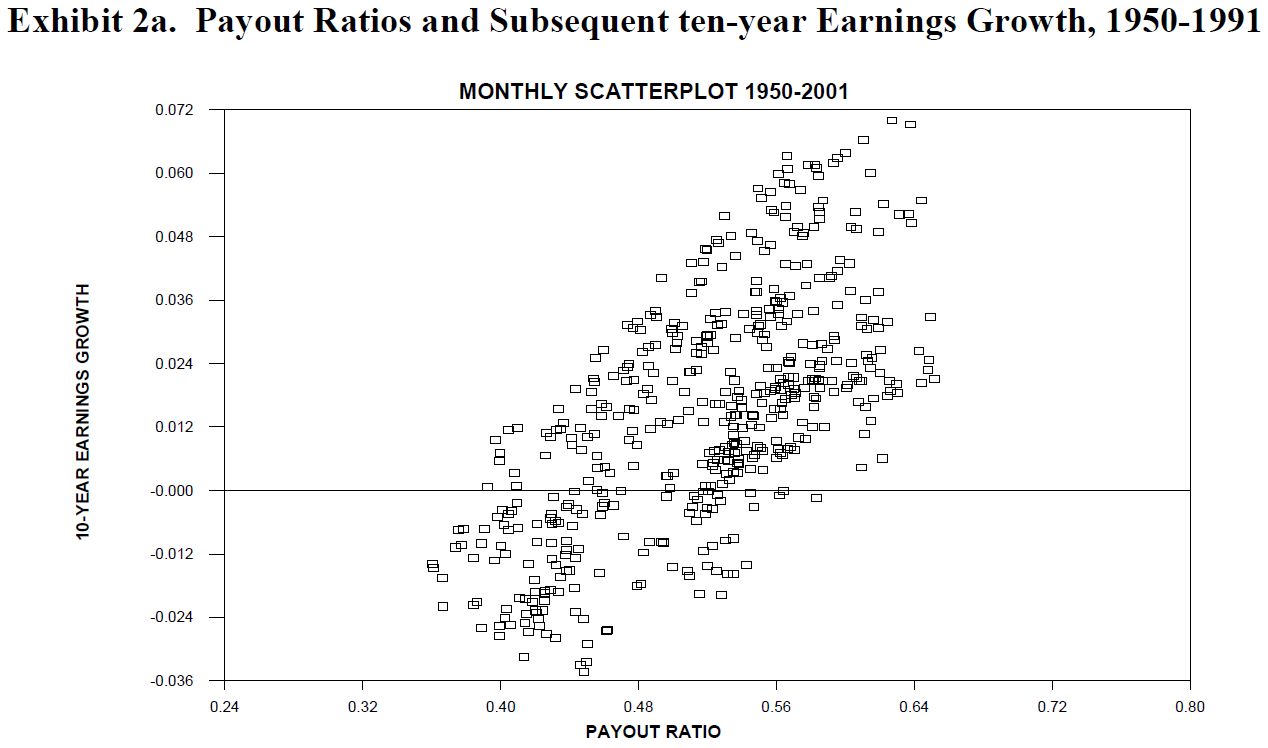

Arnott and Asness looked at historical payout ratios and earnings growth of stocks broadly representative of the market. Below is a scatterplot showing payout ratios and subsequent ten-year earnings growth from 1950-1991:

The evidence seems to indicate there is a positive relationship between payout ratio and future earnings growth. That is, higher dividend payout ratios seem to predict higher growth, while lower payout ratios predict lower growth – the opposite of what we expected.

They suggest a few hypotheses for why this might be true:

- Since managers don’t like to cut dividends, if they are concerned about the sustainability of earnings in the future they would not offer a higher dividend today; a higher payout ratio is a signal that they think future prospects look poor.

- When earnings are not paid out, cash is used to finance poor investments (malinvestment), leading to reduced earnings growth.

- When managers hold cash, it may signal “empire building,” where managers try to increase their power, rather than benefit shareholders.

So are dividends evil?

Arnott and Assness’s analysis suggests that if a firm like GE has extra cash, there may be some reasonable arguments for why they should pay that cash out as dividends, rather than hold it or invest it in disastrous projects that could destroy value.

In a world where malinvestment and empire-building are pervasive, dividends might provide a valuable signal about a firm’s shareholder policies.

Perhaps the question of whether dividends are evil may not be so clear-cut as some believe.

About the Author: David Foulke

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.