Many consider smart beta to be a revolution in the asset management industry. For example, Bloomberg ran an article, “Funds Run by Robots Now Accounts for $400 Billion,” which caught our attention.

According to this article, “Smart beta,” is one of the fastest growing segments of ETFs, accounting for nearly 20% of all assets in domestic ETFs as of the end of 2014.

The “secret sauce” of smart beta is its use of alternative weighting schemes to capture premiums associated with factors such as size, value, momentum, low volatility, and so on.

Unfortunately, academic researchers are having difficulty finding the secret sauce associated with smart beta. For us, this finding is unsurprising, since other researchers have already highlighted that many so-called factors are likely false. Nonetheless, we highlight a new research paper by Denys Glushkov, which dives deep into the data and concludes that the benefits of smart beta are questionable.

A quote from Denys:

Using a comprehensive sample of 164 domestic equity Smart Beta (SB) ETFs during 2003-2014 period…I find no evidence that SB ETFs significantly outperform their risk-adjusted passive benchmarks.

Ouch…

How Smart are “Smart Beta” ETFs?

Denys Glushkov conducts a comprehensive analysis of relative performance and factor timing of “Smart Beta” ETFs. A version of the paper can be found here.

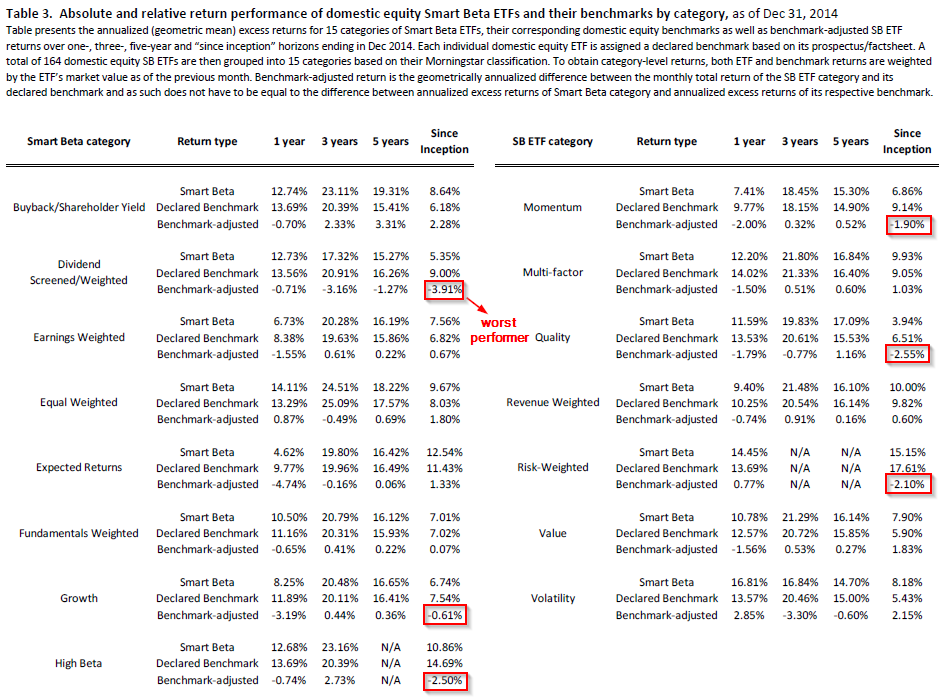

In order to see how smart “Smart Beta” really is, this paper uses 164 domestic equity “Smart Beta” ETFs from 2003 to 2014 as the test sample. It categorizes each ETF into 15 category portfolios based on common factors, and then compares them with passive index benchmarks.

This paper use 3 types of benchmarks:

- Self-declared benchmark by the ETF provider;

- Risk-adjusted version of the self-declared benchmark;

- A blended benchmark constructed as an annually rebalanced combination of passive existing funds representing the broad stock market and various factor exposures (size and value).

Finding 1: Performance isn’t great

- 60% of “Smart Beta” categories (9 out of 15) outperformed their raw declared benchmarks from 2003 to 2014.

- Only one category (Value) significantly outperformed its risk-adjusted benchmark as measured by Jensen’s alpha.

- None of the “Smart Beta” categories significantly outperformed the blended benchmark.

- One of the most popular categories, dividend-oriented ETFs, significantly underperformed the benchmark by an annualized -3.81% (t=1.73)

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Please see disclosures for additional information. Additional information regarding the construction of these results is available upon request.

Finding 2: “Good times” vs “Bad times”

- During periods of negative benchmark returns (“bad times”), none of the categories beat their risk-adjusted benchmarks;

- Even during periods of positive benchmark returns (“good times”), the same categories dramatically underperform the same benchmarks.

Finding 3: Factor Exposures

The author runs multi-factor regressions to test the factor exposure of 15 smart beta categories. The six factors used in the regressions are: size, value and momentum, quality, beta and volatility. The paper finds the following:

- Most “Smart Beta” portfolios, except dividend-oriented strategies, have significant positive exposure on the size factor, which indicates that “Smart Beta” ETFs tend to hold smaller stocks.

- Most “Smart Beta” portfolios, except Fundamentals-weighted ETFs strategies, have either insignificant or significant negative exposures to the value factor.

- Overall, “Smart Beta” ETFs do exhibit significant factor exposures, but those exposures are not always consistent.

Takeaways:

We agree that “Smart Beta” can be replicated via allocations to passive products. We also find that smart beta is essentially an expensive way to access active management, which we discuss in our post, Smart Beta is more expensive than you think.

Interesting tidbit: my friends at the Investor’s Podcast–Stig and Preston–have a pretty cool set of lectures for folks looking to figure out the ETF landscape.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.