Charlie Munger, Warren Buffett’s right-hand-man and Vice Chairman of Berkshire Hathaway, has said the following regarding behavioral economics:

How could economics not be behavioral? If it isn’t behavioral, what the hell is it?

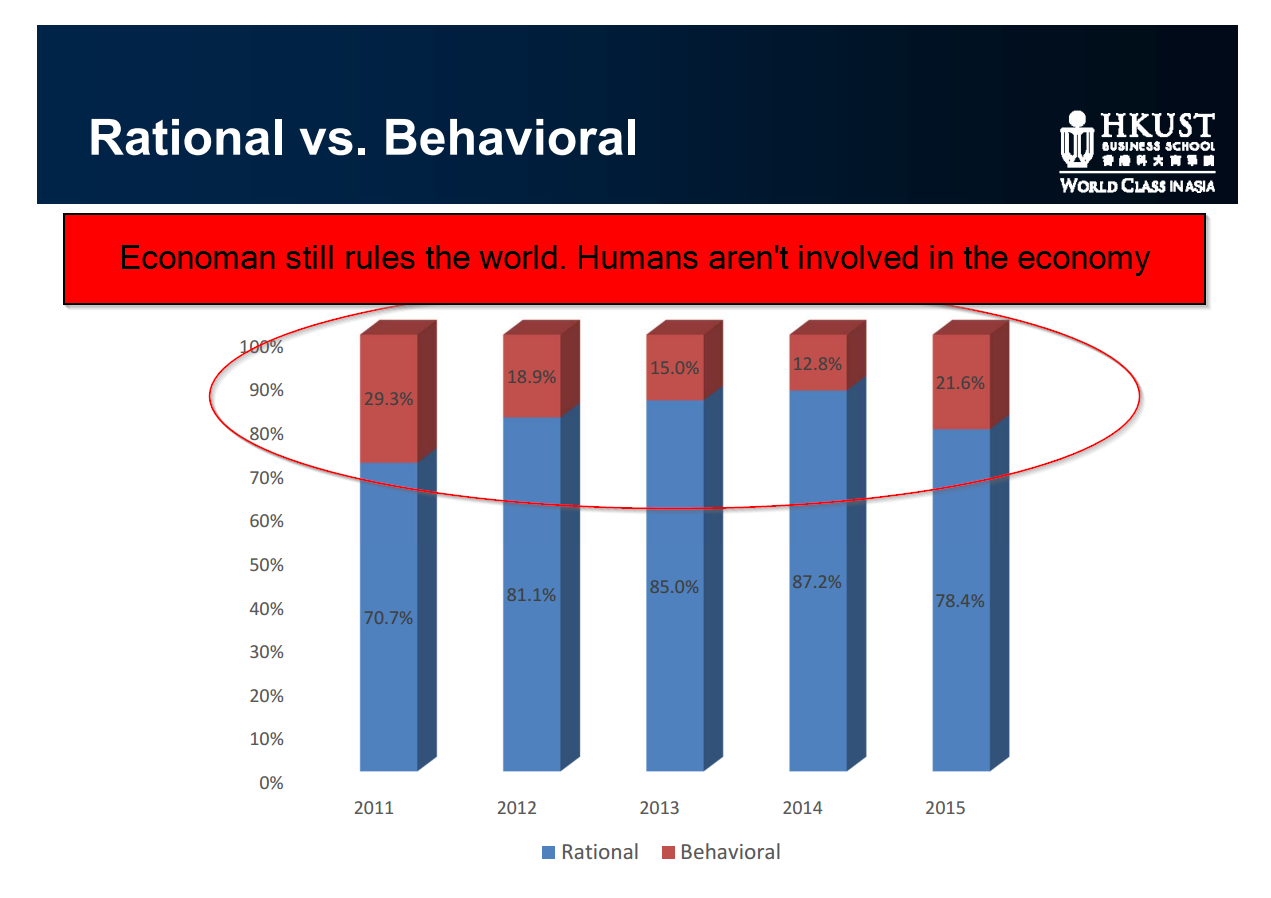

Apparently, academic researchers don’t agree. A crew of PhD students at HKUST summarize the articles being published in top-tier economic and finance publications over the past 5 years.

Perhaps not surprisingly, the academic literature (as proxied via the Journal of Finance) overwhelming sticks to their guns when it comes to understanding “agents” in the economy. Papers focused on “rational” finance outnumber “behavioral” finance 4 to 1. Or as Dick Thaler might say, “The econs are winning.”

The good news is we help fill the void and try and highlight interesting papers focused on behavioral finance. Our treatise on the subject is here.

The HKUST PhD students also find a bunch of interesting things that summarize the status of academic finance research.

Here are a summary of the points highlighted in the paper:

- The journals are not as US-centric as commonly believed in Asia.

- The number of authors per article is trending up, with the mean being about 2.6.

- Classification is very difficult. There are more papers published which are not only intra-discipline but also inter-disciplinary. Macro-banking-finance is the hottest inter-disciplinary topic.

- The ratio between theory to empirical is highest in RFS (about 1:2) and lowest in JFQA (about 1:6). No trends are discernible in asset pricing, but less theory papers are being published in corporate finance.

- In corporate finance, the dominance of the old chestnuts – capital structure and corporate governance – is trending down. M&A is popular. Links between markets, banks and firms is a hot new area.

- In asset pricing, identification of new sources of risk, and pricing of non-equity assets are hot new areas.

- In investments, hedge funds, venture capital and private equity are hot.

- High frequency trading has resuscitated the market microstructure area.

- Niche areas like household finance, culture and finance, politics and finance, labor and finance, media and finance, networks and finance, are not niche anymore.

- Amongst finance journals, JF is No 1 followed by the RFS.

- Top non-finance journals like the AER, JPE, QJE and Management Science publish many finance papers. With the notable exception of QJE, these journals now have lower impact factors than the top 3 finance journals.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.