Just got done perusing the latest issue of the Journal of Finance . As is the typical case, 50% of the articles can be read if you have a PhD in math, but the other 50% are readable. Kinda.

Here is a really surprising one: Investment consultant recommendations are effectively worthless, on average.

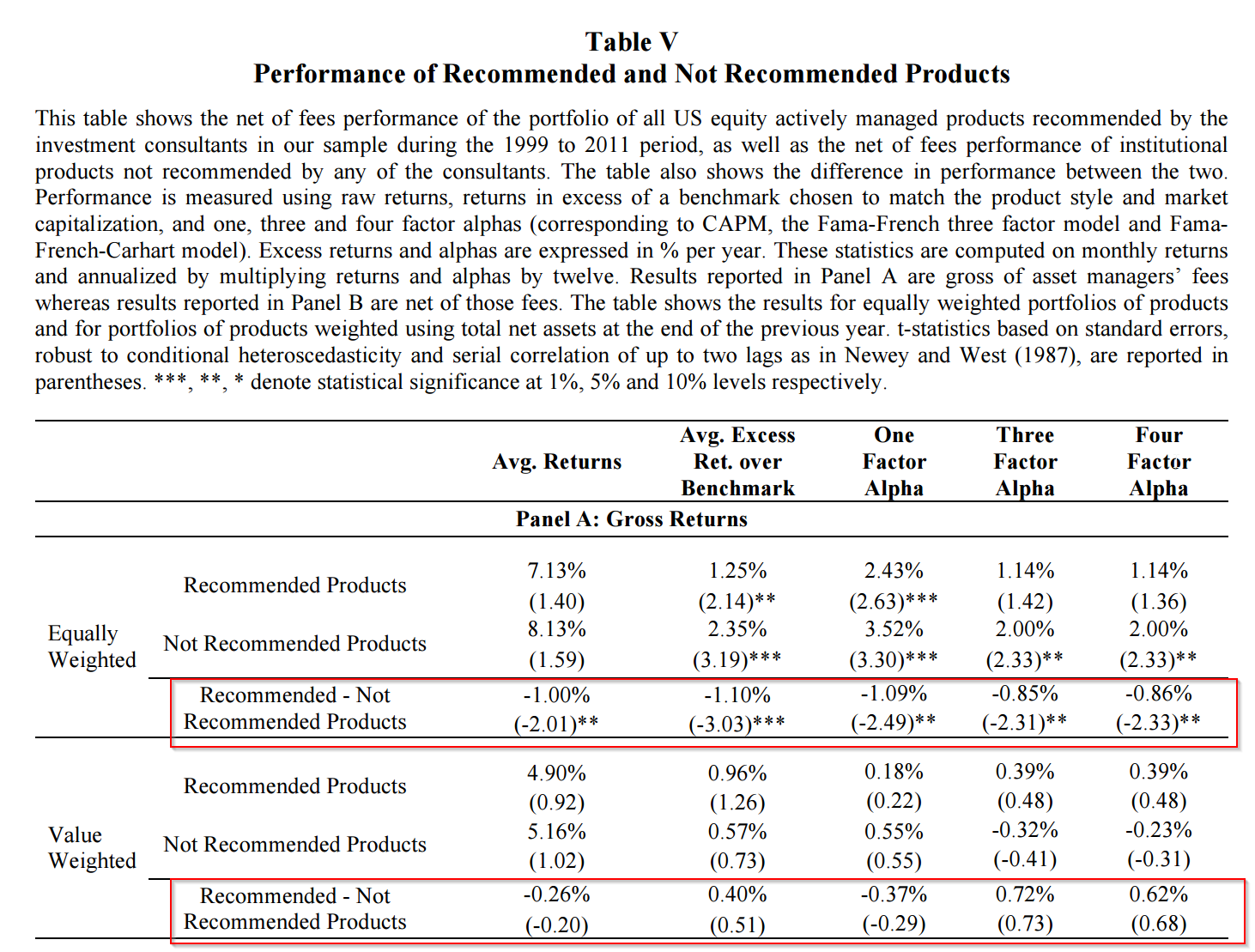

Similar to the retail advisory space, the institutional consultant service providers likely add value via their role as a money doctor, not in their role as a “manager picker.”

Picking Winners? Investment Consultants’ Recommendations of Fund Managers

Investment consultants advise institutional investors on their choice of fund manager. Focusing on U.S. actively managed equity funds, we analyze the factors that drive consultants’ recommendations, what impact these recommendations have on flows, and how well the recommended funds perform. We find that investment consultants’ recommendations of funds are driven largely by soft factors, rather than the funds’ past performance, and that their recommendations have a very significant effect on fund flows. However, we find no evidence that these recommendations add value, suggesting that the search for winners, encouraged and guided by investment consultants, is fruitless.

Here is the key table from the paper highlighting that the spread in performance between recommended and not-recommended funds is flat, and arguably negative if you equal-weight the recommendations.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.