Conventional wisdom can be defined as ideas that are so accepted that they go unquestioned. Unfortunately, conventional wisdom is often wrong. Two great examples are that millions of people once believed the conventional wisdom that the Earth is flat, and millions also believed that the Earth is the center of the universe.

Much of today’s conventional wisdom about investing is also wrong.

The Tax Efficiency of Long/Short Investment Strategies

Today, we’ll look at the conventional wisdom that the tax burden of an investment strategy increases with its turnover — high-turnover strategies exhibit a higher propensity to realize capital gains. In addition, short-selling is perceived to be particularly tax-inefficient, because the realized capital gains on short positions are generally taxed at the higher short-term capital gain tax rate, regardless of the holding period of the short positions.

Clemens Sialm and Nathan Sosner contribute to the literature on the tax efficiency of long-short strategies with their January 2017 paper, “Taxes, Shorting, and Active Management.” Sialm and Sosner studied the consequences of short-selling in the context of quantitative investment strategies that individual investors hold in taxable accounts. They computed the tax burden of a quantitative fund manager who follows a combined value and momentum strategy. Combining value and momentum strategies is particularly beneficial because these strategies tend to exhibit negative correlation. Their model combined value and momentum with equal risk weights and targeted a tracking error of 4 percent. The authors implemented tax awareness through a penalty term that incorporates tax costs into the portfolio’s objective function. The study’s sample period is from 1985 to 2015.

The following is a summary of their findings:

- Short positions not only allow investors to benefit from the anticipated underperformance of securities, but they also create tax benefits because they enhance the opportunities to time capital gain realizations.

- The presence of short positions gives investment strategies additional opportunities for realizing capital losses in up markets, when capital losses from long positions are scarce. Up markets are also when investors tend to have more abundant capital gains, making the realization of capital losses in these periods particularly valuable.

- Long-short strategies increase the opportunity to realize short-term losses, which are particularly beneficial because the short-term capital gains tax rate is substantially higher than the long-term rate, and the realized short-term losses will first be used to offset highly taxed short-term capital gains.

- The relaxation of short-selling constraints generates tax benefits because a portfolio’s long positions tend to generate long-term capital gains, which are taxed at relatively low rates, whereas the short positions tend to generate short-term capital losses, which offset short-term capital gains taxed at relatively high rates.

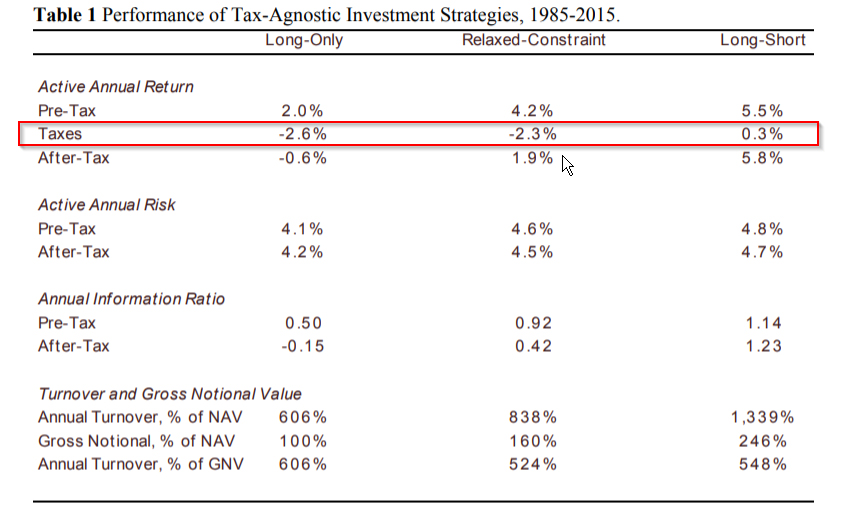

Specifically, the authors found that,

…if the strategy is managed as a long-only portfolio, it generates a tax burden of 2.6% per year. On the other hand, if the strategy is managed as a relaxed-constraint portfolio that combines a 130% long exposure with a 30% short exposure, its tax burden reduces to 2.3% per year. For a long-short strategy, the tax burden turns into a tax benefit of 0.3% per year.

The table below (from the source paper) outlines these results:

They also found that,

…the investor can further enhance the tax benefits by deferring the realization of capital gains and accelerating the realization of capital losses. As compared to the tax-agnostic approach, such tax-aware asset management reduces the annual tax burden of the long-only strategy from 2.6% to 0.7%, turns the annual 2.3% tax burden of the relaxed-constraint strategy into a 0.9% tax benefit, and increases the tax benefit of the long-short strategy from 0.3% to 6.1% per year.

Tax-aware strategies also significantly reduce the turnover of long-short strategies because they reduce capital gains realizations (delaying realization until short-term gains become long-term), and, thus, trading costs.

It’s important to note that Sialm and Sosner’s results are, “specific to investors who realize sufficient short- and long-term capital gains from other investment sources. The reduction in the taxes is smaller if the portfolios are structured as mutual funds according to the Investment Company Act of 1940 or if the investor does not have any other capital gains in the portfolio. In these cases, the remaining capital losses need to be carried forward to future years, which will likely reduce the benefits of capital loss realizations.”

However, despite the reduced tax benefits of using limited offsets, they also found:

a significant reduction in the tax burden in strategies that take advantage of short selling and tax awareness. For example, a tax-agnostic long-only strategy generates tax costs of 2.9% per year, whereas a tax-agnostic long-short strategy generates tax costs of only 0.7% per year despite a higher pre-tax active return. Furthermore, introducing tax awareness generates a tax benefit of 0.5% for a long-short strategy. This small benefit occurs primarily due to the fact that dividends obtained on the long positions qualify for the dividend tax rate, whereas in-lieu dividend payments on the short positions can be deducted from ordinary income emanating from cash used to finance the long-short portfolio. Thus, tax-awareness and short-selling can also enhance after-tax returns for investors who have limited opportunities to offset capital gains realizations.

Additionally, Sialm and Sosner noted that their examples, “assume that the portfolio does not experience any inflows or outflows of funds. Inflows provide additional opportunities to reduce the tax burden of future portfolio rebalancing since these funds are used to purchase new positions and thus increase the cost basis of a portfolio with embedded unrealized capital gains. On the other hand, outflows, if not managed in a tax-efficient manner, may trigger additional taxes as the investor needs to liquidate positions and potentially realize capital gains.”

Sialm and Sosner concluded that their results show quantitative investment strategies that take advantage of short-selling can generate superior after-tax performance by significantly reducing the tax burden, and can even generate tax benefits if executed with an eye toward tax awareness.

Another finding to note is that, “on average the tax benefits of tax-aware strategies come from short positions. Moreover, these tax benefits are positively correlated with market returns meaning that the short positions generate tax losses exactly at the time when other investments in the investor’s portfolio are likely to be at a gain.”

Importantly, they also found that their conclusions, “are robust to the target level of active risk, to transaction and financing costs, to the level of tax aversion, and to the historical variation in tax rates.”

Conclusion

Summarizing, Sialm and Sosner demonstrate that the conventional wisdom on the tax-efficiency of long-short strategies is wrong, having found that, as previously noted, the tax benefits of tax-aware strategies come, on average, from short positions. In addition, they found that “these tax benefits are positively correlated with market returns meaning that the short positions generate tax losses exactly at the time when other investments in the investor’s portfolio are likely to be at a gain.” Their evidence demonstrates, “that short-selling is a valuable tool for a taxable investor. While portfolio design decisions – market beta, level of risk and tax aversion, and turnover and leverage – might vary, the presence of short positions is likely to enhance after-tax returns and to interact favorably with explicit tax awareness.”

These findings have important implications for investors willing to consider leverage and shorting as part of their equity strategies. AQR’s launch of four Relax Constrained (130/30) equity strategies seems to be putting this research to work, seeking to reduce distributions and preserve as much pre-tax excess return as possible. (Full disclosure: My firm, Buckingham Strategic Wealth, recommends AQR funds in constructing client portfolios.) Overall, mutual fund investors could see a reduction in distributions, and investors capable of investing in private vehicles (LP’s) could find a way to offset capital gains from elsewhere in their portfolio — all good developments for the taxable investor, especially in a lower expected return environment. Last but not least, there are other interesting tax-efficient alternative solutions that leverage the ETF structure (see here for an explanation of the tax efficiency of ETFs). The Alpha Architect Long/Short Index is an example of this approach.

Bottom line? Long-short equity strategies are typically tax-inefficient, however, these strategies can be tax-efficient, if implemented with tax-efficiency in mind.

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.