Do Stars Shine? Comparing the Performance Persistence of Star Sell-Side Analysts Listed by Institutional Investor, the Wall Street Journal, and StarMine

- Yury O. Kucheev, Felipe Ruiz and Tomas Sorensson

- Journal of Financial Research Studies

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

- Can investors profitably trade on the stock recommendations of security analysts that are ranked by the WSJ, Institutional Investor and Thomson-Reuters StarMine?

- Does the choice of the ranking agency matter? That is, are the selection criteria used to rank security analysts more or less, superior and persistent in identifying “star” analysts?

What are the Academic Insights?

Constructing a database of Star analyst designations collected from Institutional Investor, the Wall Street Journal and StarMine for the period 2003 to 2014, the authors document the differences in profitability of following Star and nonStar analyst recommendations as an investment strategy.

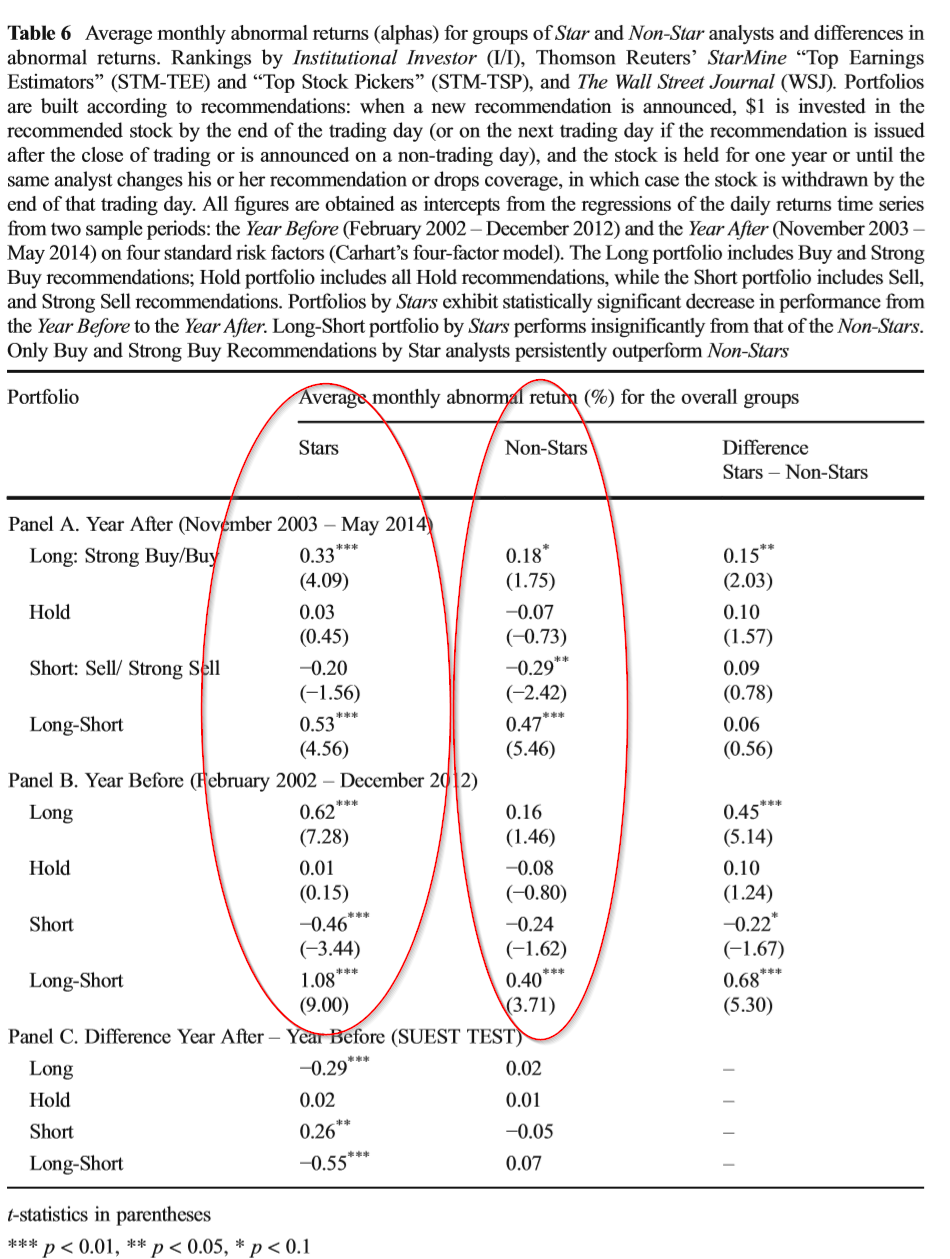

- YES. During the entire year post designation as a Star analyst, following the Strong Buy and Buy recommendations issued by the Star analysts produced a monthly alpha of 0.33% for vs. all nonStars at 0.18%, across all ranking agencies. All other recommendations (Hold, Sell, Strong Sell) exhibited no differences during the year following the election to Star status.

- YES. An examination of the group of Star analysts revealed that StarMine Stars generated a monthly alpha of 0.97%, the WSJ Stars produced an alpha of 0.63%, and Institutional Investor Stars came in last reporting 0.14% alpha. ONE CAVEAT: No adjustments for transactions costs were made in the study.

Why does it matter?

This study provides evidence that investors who follow the Buy and Strong Buy recommendations of Star analysts will outperform on a risk adjusted basis, for at least one year post election to the Star ranking. More importantly, the choice of ranking agency, and therefore the ranking methodology utilized, matters in a substantial and significant way. The superior performance of the StarMine Stars indicates the necessity of making superior earnings forecasts in order to make successful “stock picks” —which is inherent in their ranking methodology.

The most important chart from the paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

We investigate the profitability persistence of the investment recommendations from analysts listed in four different star rankings, Institutional Investor magazine, StarMine’s Top Earnings Estimators, and Top Stock Pickers, and The Wall Street Journal, and show the predictive power of each evaluation methodology. We found that only Buy and Strong Buy recommendations from the entire group of Star analysts outperform those of the Non-Stars in the year after election, while Sell and Strong Sell recommendations performed as those of the Non Stars. We document that the highest average monthly abnormal return of holding a long-short portfolio, 0.97 %, is obtained by following the recommendations of the group of star sell-side analysts rated by StarMine’s Top Earnings Estimators during the period from 2003 to 2014. Since earnings are one of the main drivers of stock prices, the results obtained are in line with the notion that focusing on superior earnings forecasts is one of the top requirements for successful stock picks.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.