The world of withholding tax recovery on foreign dividends and interest is woven with intricacies, challenges, and a general lack of transparency. This is mainly due to its complexities and the cumbersome process involved in achieving successful refunds. Often left in the hands of custodians to battle it out, refund potential of up to 30% is still lost. This article intends to shed more light on the withholding tax reclaim process by providing an example of how withholding taxes are suffered on foreign investments and how maximum withholding tax refunds can be achieved.(1) We are going to run through an example of a dividend payment occurring in France in which we recover the full amount withheld by foreign governments utilizing:

- Double Tax Treaty Claim

- European Court of Justice Claim

Editor’s note: we use the services provided by Julia’s firm in our own business and only recently learned about the details on how to maximize foreign dividend withholding tax refunds on behalf of one’s clients. Our assumption was that your custodian would take care of this — which some do to a certain extent, but as we’ve learned more, one can’t rely on the custodian to do the job. We recommend all investors and fiduciaries investigate how their service providers (custodians and fund sponsors) are dealing with these issues. Blank stares are probably not an acceptable answer.

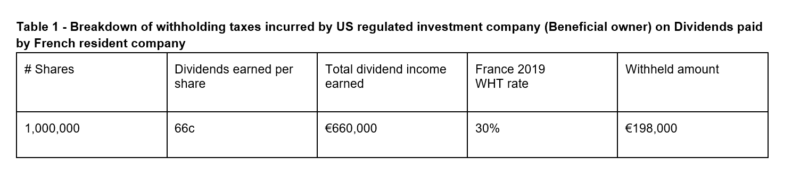

Example of Foreign Direct Investment in Total SA

In this scenario, assume a US regulated investment company (RIC) owns 1 million shares in Total SA, a publicly listed company traded on the French stock exchange. The US fund earned 66c per share on the first 2019 interim dividend of Total SA paid on October 1st, 2019. The fund therefore earned a total dividend of €660,000.

However, the US fund did not receive the full €660,000 because these dividends are seen as French earnings and are thus subject to a 30% statutory withholding tax (the rate has been reduced to 28% for dividends paid from 2020 onwards). The tax would have been withheld by the French paying company and remitted to the French tax authorities. The US RIC would have received only 70% of the total dividend, i.e. €462,000. The tax is withheld before dividend payment to the beneficiaries takes place as it would be practically impossible for the French tax authorities to collect this tax from ultimate shareholders following dividend payment, due to the number of beneficiaries in the payment chain as well as the geographical dispersion of shareholders.

In addition to the French withholding tax, the US RIC would still be liable to pay US income tax on their French dividends due to the principle of worldwide taxation for residents, and hence double taxation would occur. The financial impact of double taxation erodes the returns from offshore dividends and makes foreign investment less desirable. Therefore, if France wants to secure US investment in its companies and vice versa, there needs to be some give and take to reduce or eliminate this double taxation.

1. The USA-France Double Taxation Treaty

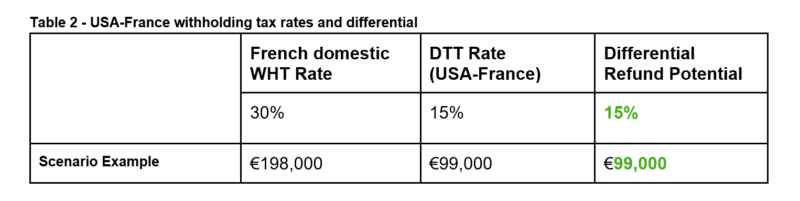

The main goal of double tax treaties is to remove impediments to international trade and investment. In the absence of such agreements, investors would be reluctant to engage in cross-border trade. The USA-France double taxation treaty (“Convention between the government of the United States of America and the Government of the French Republic for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion With Respect to Taxes On Income and Capital”, effective date: 1 January 1996) sets out to reduce double taxation on transactions between residents of France and the United States. This is done by limiting taxing rights on different categories of income and assigning specific rights to each Contracting State with regards to the taxation of income. Generally, where dividends are concerned, this is achieved through allowing primary (full) taxing rights in the country of residence and a secondary (limited) taxing right in the country of investment. In our example, this would allow the Internal Revenue Service full taxing rights on the French sourced income but would limit the ability of the French tax authorities to tax this same income.

Reduced Withholding Tax Rates

Article 10 of the USA-France double taxation treaty (DTT) specifically deals with the taxing rights for dividend income. The treaty states that if the beneficial owner of the dividends is a resident in the United States, the French tax so charged shall not exceed 15% of the gross amount of the dividends in other cases.

(Article 10, Paragraph 2, Section B)

Therefore, if our US RIC is considered to be a US resident in terms of the DTT, the French tax should have been levied at 15% as opposed to 30%, which creates a refund opportunity for the difference. Please note that there are situations where documentation can be provided in advance of the dividend payment to secure the reduced withholding tax rate at the dividend payment date. This process is referred to as relief at source and is available in some investment jurisdictions. However, where the tax has been charged at the statutory rate, there is a refund opportunity for the difference between statutory and treaty prescribed tax rate.

It is clear that a refund opportunity (of €99,000) exists for the US investment company in our example. The next task would be to determine the US company’s eligibility for a refund.

Identifying Eligibility for Refund

Article 4 of the USA-France DTT determines the criteria of residency and who is eligible for treaty benefits. In terms of Article 4, the following (amongst others) are regarded as residents of the United States and therefore eligible for refunds:

A United States regulated investment company, a real estate investment trust, and a real estate mortgage investment conduit; and any similar investment entities agreed upon by the competent authorities in both France and the United States.Article 4, Paragraph 2, Biii

To continue using our example, our US investment firm would fall into Article 4(c) and would, therefore, be entitled to the withholding tax benefits and reduced withholding tax granted by the USA-France double taxation treaty.

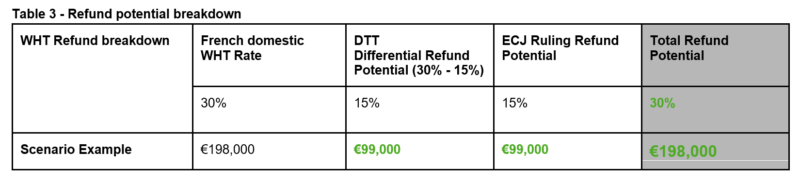

WTax files claims with the French tax authorities to recover tax charged in excess of the prescribed treaty rate. The DTT claim would therefore reduce the withholding tax suffered from 30% to 15%.

At this point, the US investment firm is still incurring 15% in French withholding taxes. WTax files claims to eliminate this final 15% French withholding tax using established court precedent based on the principles of discrimination of foreign investors.

2. European Court of Justice (ECJ) Claims

What is the European Court of Justice in the context of Withholding Taxes?

All countries that form part of the 27-Member States of the European Union (EU) are subject to the laws and regulations set by the EU. The Treaty on European Union (TEU) and the Treaty on the Functioning of the European Union (TFEU) are the two main sources of EU law.

The role of the European Court of Justice is to interpret EU law and ensure it is applied in the same way in all 27 EU countries. To this end, the Court confirms the legality of the actions of the EU institutions, ensures the Member States comply with their obligations and interprets EU law at the request of national courts.

Although it is at each country’s discretion to set its own direct taxation rules, these rules cannot contravene the principles established in the EU community laws (the TEU and the TFEU mentioned above). Member States are bound to their commitment to the EU community under the treaties. Therefore, National Direct Tax provisions must not compromise the freedoms enshrined in the EU Treaties.

The European Court has the power to settle legal disputes between Member States, EU institutions, businesses and individuals. If the court confirms that a State has failed to fulfill its obligations, the State is required to put an end to the infringement immediately.

Claiming Withholding Taxes through ECJ Claims

When the Member States tax domestic investment funds differently than foreign investment funds on the same type of income, this constitutes discriminatory tax practice and is often unjustified. This often results in less favorable treatment between residents and non-residents in comparable situations.

These tax practices are contradictory to the principle of free movement of capital within the EU. Article 63 of the Treaty of the Functioning of the European Union (TFEU) sets out the principles of the free flow of capital and states that restrictions on the movement of capital within the EU and between the EU and any third-party countries are prohibited. Article 65 of TFEU sets out that different tax treatments are allowed for foreign entities, only in situations where the tax provisions distinguish between i) taxpayers who are non-resident or ii) based on the place where their capital is invested, as long as it does not constitute a means of arbitrary discrimination or a disguised restriction on the free movement of capital and payments as defined in Article 63.

The European Court of Justice Rulings

There have been a number of milestone judgments issued by the European Court of Justice which have paved the way for additional withholding tax recovery, in excess of treaty-based claims. The premise for these cases was that foreign funds should not be taxed less favorably than comparable local funds as this would be against the principles of the free movement of capital as outlined in Article 63 of the Treaty on the Functioning of the European Union. The cases initially involved various EU member states where it was ruled that treating comparable mutual funds from various EU member states differently would constitute discrimination, which cannot be justified. As French investment funds do not suffer withholding taxes on French-sourced dividends, it must be considered whether the taxation of the same dividends in the hands of comparable foreign investment funds is discriminatory. We base this analysis on precedents established in various court cases.

With respect to investment funds, the European Court of Justice issued a number of ground-breaking cases, we have summarized one of the key cases below:

2012 – France; Joint Santander judgement (C-338/11/C347-11) vs France

On 10 May 2012, the ECJ confirmed that if the French tax authorities did not pay out the French WHT on outbound dividends to non-residents, this constituted a restriction on the free movement of capital, to the extent that France does not tax domestic UCITS funds. Their reference in their ruling to the specific term UCITS clarified the applicability of the ruling to all types of UCITS funds, irrespective of their form (e.g. FCP or SICAV). The inclusion of third-party countries (non-EU) in Article 63 ensures that investment funds domiciled in non-EU States are also entitled to claim non-discriminatory withholding tax treatment.

US RIC Investment Fund Claiming French Withholding Tax Based on ECJ Rulings

The ECJ rulings created an opportunity for third party countries to submit and obtain full refunds, based on this reclaim mechanism.

To expand, US RICs should not be taxed differently to French investment funds on French sourced income if it can be proven that the US RIC is comparable to the French investment fund. As French investment funds do not suffer French withholding tax on French dividends, comparable US RICs should not suffer French withholding tax on the same dividends. WTax files claims on this premise by preparing detailed comparability analyses between local and foreign investment structures and utilizes this argument to substantiate a claim for the full amount of withholding tax suffered in France.

Our US investment firm can apply for a withholding tax refund based on the principles laid out in the above mentioned cases. The US investment firm can therefore recoup 100% of the withholding taxes due to them.

The Complexities of ECJ Claims

ECJ claims are the most neglected withholding tax refund mechanism. The claims are highly complex and require a deep knowledge of the legislation and governing rules in place to achieve refunds. Furthermore, in most cases, custodians (who are often an investor’s go-to point for DTT claims) are generally unable to help with ECJ claims. Some countries still need to recognize the discrimination as identified in the relevant court cases and are therefore not refunding claims at present. However, it is important to submit claims to safeguard the investor’s right to a withholding tax refund as these claims are statute barred and could potentially expire. In our example, if the 2019 withholding tax remains unclaimed, the recovery opportunity will be lost at the end of 2021.

Conclusion

The above scenario’s intention was to give you a practical walk-through of the legislative workings and decision-making process that occurs when processing withholding tax refund claims using both the DTT and ECJ reclaim mechanisms. Although the process is complex, material improvements in fund performance can be seen through withholding tax recovery.

About the Author: Julia Bricker

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.