From January 2017 through March 2020, the value premium, defined by HML (the return of high book-to-market stocks minus the return of low book-to-market stocks experienced a drawdown of 42 percent.(1) If we extend the period back to January 2007, the drawdown of about 51 percent is the largest ever. There have been many attempts to explain the reason for the dramatic underperformance; we’ve even covered some research on the topic here and here. However, none hold up to a thorough analysis of the data. For example, Ronen Israel, Kristoffer Laursen, and Scott Richardson of AQR Capital Management, authors of the March 2020 paper “Is (Systematic) Value Investing Dead?(2)” analyzed five explanations that have been offered for the “death of the value premium” and found all of them wanting. AQR founder Cliff Asness, in his May 2020 paper of the same name, also examined several other possible explanations and found that none explain value’s underperformance. One explanation is that the interest rate environment—the low level of interest rates, falling bond yields and/or the flattening yield curve—since the Great Financial Crisis explains value’s underperformance, the logic being that growth stocks are longer-duration assets than value stocks and thus benefit more from falling rates.

Thomas Maloney and Tobias Moskowitz contribute to our understanding of the impact of interest rates on the value premium with their May 2020 study “Value and Interest Rates: Are rates to blame for value’s torments?” They began by noting:

Changes in real or nominal interest rates are often accompanied by (or are often a response to) changes in expected inflation and/or changes in expected economic growth, and hence expected cashflows are often changing as well. There may also be a change in the required risk premium which is the other (and often larger) component of the discount rate. All of these components have their own dynamics and are likely simultaneously being affected by macroeconomic conditions in possibly different ways. These confounding effects make it extremely difficult to identify what impact interest rates should have on value and growth portfolios.

As an example, they added:

Interest rate changes reflect economic conditions which almost surely are reflected in cash flows and risk premia, too, and the combined effect from these changes may dominate the duration effect.

Because of these complexities, the authors turned to an empirical evaluation of value’s sensitivity to interest rates. They noted:

The data informs us of the net impact of all the interacting variables associated with interest rate regimes and value returns. The downside is that associating the results with any particular theory is challenging since multiple effects are likely at play.

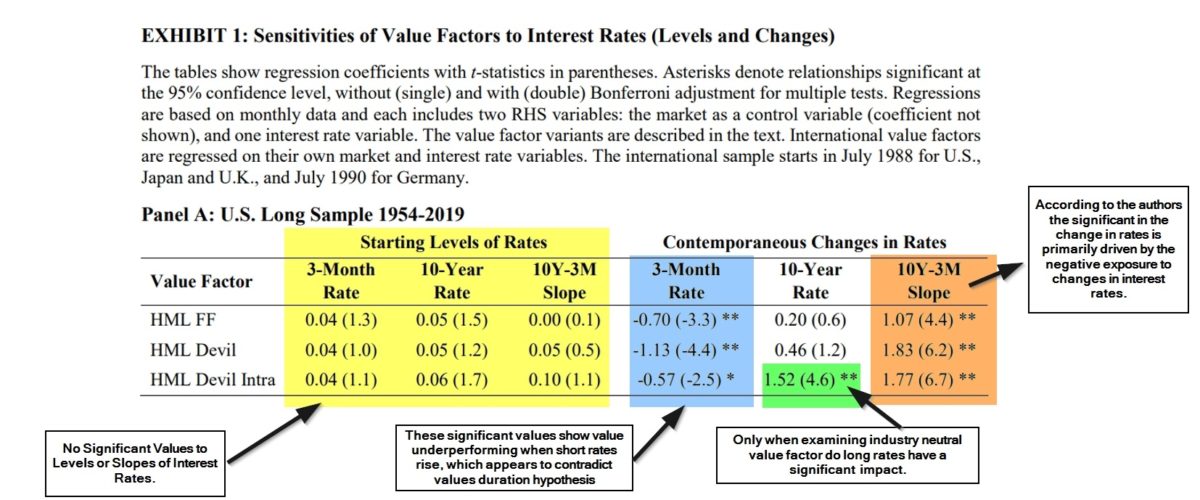

Their data sample included U.S., German, U.K., and Japanese stock and bond markets. For short-term rates, they used the three-month bill, and for long-term rates (and the slope of the curve) they used the 10-year security. They considered levels as well as rates of change in the levels. They also used multiple value metrics, including a composite, for the value premium. The U.S. data sample runs from 1954 through 2019. The international sample begins in 1988.

Following is a summary of their findings:

- The relationship between value factor returns and the interest rate environment is not robust. Different choices for interest rate variables, different measurements and implementations of value, and different samples through time and across markets deliver varying results.

- Despite some eye-catching patterns in recent data, particularly those related to changes in bond yields or the yield curve slope, the economic significance of any relationship is small and not robust in other samples.

- The strongest and most statistically reliable result is between changes in the slope of the yield curve and value returns. However, the economic significance of even this relationship is weak.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

- Debt levels do not seem responsible for value’s sensitivities to long rate changes and slope changes. In addition, although value firms have tended to be more indebted over the long term, they have not been so over the past decade.

- Value firms have tended to be more distressed over the long term but less so during the past decade when performance suffered. This is the reverse of what we would have expected—a much larger exposure to distress over the recent decade.

- The international results are weaker than they are for the U.S. Specifically, Japan has by far the highest average value return during the sample period and the lowest interest rates.

- There is little evidence of predictive relationships useful for the tactical timing of the value premium.

Of particular interest was that Maloney and Moskowitz had some findings which conflicted with theories proposed for value’s underperformance. For example, they found “some significant sensitivities of value factors to contemporaneous interest rate changes in the short and long rates, and also to changes in the slope of the yield curve. Specifically, value factors underperform when short rates contemporaneously increase.” This conflicts with the duration theory hypothesis (covered here and here) that rising rates should be bad for longer duration growth stocks, not shorter duration value stocks. The authors then noted:

“It could be consistent with value being a proxy for financially distressed firms, but this interpretation is complicated by the fact that short rates tend to rise during benign economic environments when distressed firms are unlikely to suffer disproportionately.”

As an out-of-sample test the authors also examined the U.S. for the period 1926-1953, using quarterly instead of monthly data due to availability. Their findings were similar.

Their findings led Maloney and Moskowitz to conclude: “The performance of value is not easily assessed based on the interest rate environment, and that factor timing strategies based on interest rate-related signals are likely to perform poorly.” They added: “The interest rate regime offers little insight into value’s prospects.” The authors also concluded: “The clear implication is that the low-yield environment that pervaded the last decade and continues in 2020 says very little about the past performance or future prospects of value investing.”

Summary

Changes in either the level of interest rates or the slope of the yield curve fail to explain any significant portion of value’s underperformance over the past decade. Nor do they explain value’s sharp drawdown in the first quarter of 2020. While we like to find good economic explanations for factor performance, the only explanation for value’s underperformance has been the dramatic change in the relative prices investors have been willing to pay for growth stocks versus value stocks—what John Bogle called the “speculative return.” This is a repeat of what happened to the value premium at the end of the last millennium. Today, the spread in valuations is now at about the 100th percentile around the globe. And valuations are the best, though far from a perfect, predictor of future returns. The bottom line is that there doesn’t seem to be any evidence supporting the belief that the value premium is dead. The evidence supports the view that it is far more likely to be dormant, awaiting an awakening.

Post Script

In his study “What Happens to Stocks when Interest Rates Rise?” published in the Summer 2018 issue of The Journal of Investing, Andrew L. Berkin examined the relationship between interest rates and various factors. He found that stocks have had a wide range of returns both positive and negative during times of rising rates. He also found that for most factors, including value as defined by the metric HML (the return of stocks with high book-to-market ratios minus the return of stocks with low book-to-market ratios), there was no distinguishing pattern looking at interest rates a variety of ways (such as long term, short term, spread, level, and change). The main exception was dividend yield, which tended to do well in the same year when rates fall (and vice-versa when they rise). A simple explanation is investors reaching for yield. However, results are reversed the following year: high (low) dividend yield stocks do relatively poorly (well) in the year after rates fall.

References[+]

| ↑1 | The team at Buckingham Wealth Partners reviewed these results and found similar results, concluding: From January 2017 through March 2020, the value premium experienced a drawdown of 42 percent. If we extend the period back to January 2007, the drawdown of about 51 percent is the largest ever. In addition, when looking at the value factor itself based on the univariate sort, the numbers remained consistent with a drawdown of 47 percent from January 2017 through March 2020, and a drawdown of 59 percent from January 2007 through March 2020. The team also found that using the univariate sort, high book-to-market stocks lost 22.7 percent in total returns from January 2017 through March 2020. Low book-to-market stocks returned 49.1 percent in total returns over the same period, for a relative underperformance of 71.8 percent. From January 2007, high book-to-market returned 32.4 percent (total return) versus 246 percent for low book-to-market, for a relative underperformance of 213.6 percent. |

|---|---|

| ↑2 | Look for a summary of this paper from Tommi on the Alpha Architect Blog |

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.