Cross-Asset Skew

- Nick Baltas and Gabriel Salinas

- Working Paper, SSRN

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

In the search for more and better factors, this article examines the cross-sectional relationship between historical skewness (see Jack’s post here) and the returns on a robust set of assets and documents the premium for taking on skewness risk. The authors construct long/short portfolios across four global asset classes including equity indices, government bonds, commodities, and currencies observed during the 1990-2017 time period. Long portfolios are comprised of securities with a negative skew or least positive. Short portfolios are comprised of securities with a positive skew or least negative. For each of the 4 asset classes, daily returns are calculated from futures and forward prices. The skewness metric is the estimated Pearson’s moment coefficient of skewness for each asset, at the end of each month, using a 12-month rolling window. Robustness checks include tests with alternative skewness metrics; and with varying degrees of the estimation window of the skewness metrics.

- Is there a relationship between skewness and future returns?

- Does the skewness premium survive when commonly accepted risk factors are taken into account?

- Theoretically, why would investors show a preference for skewness?

What are the Academic Insights?

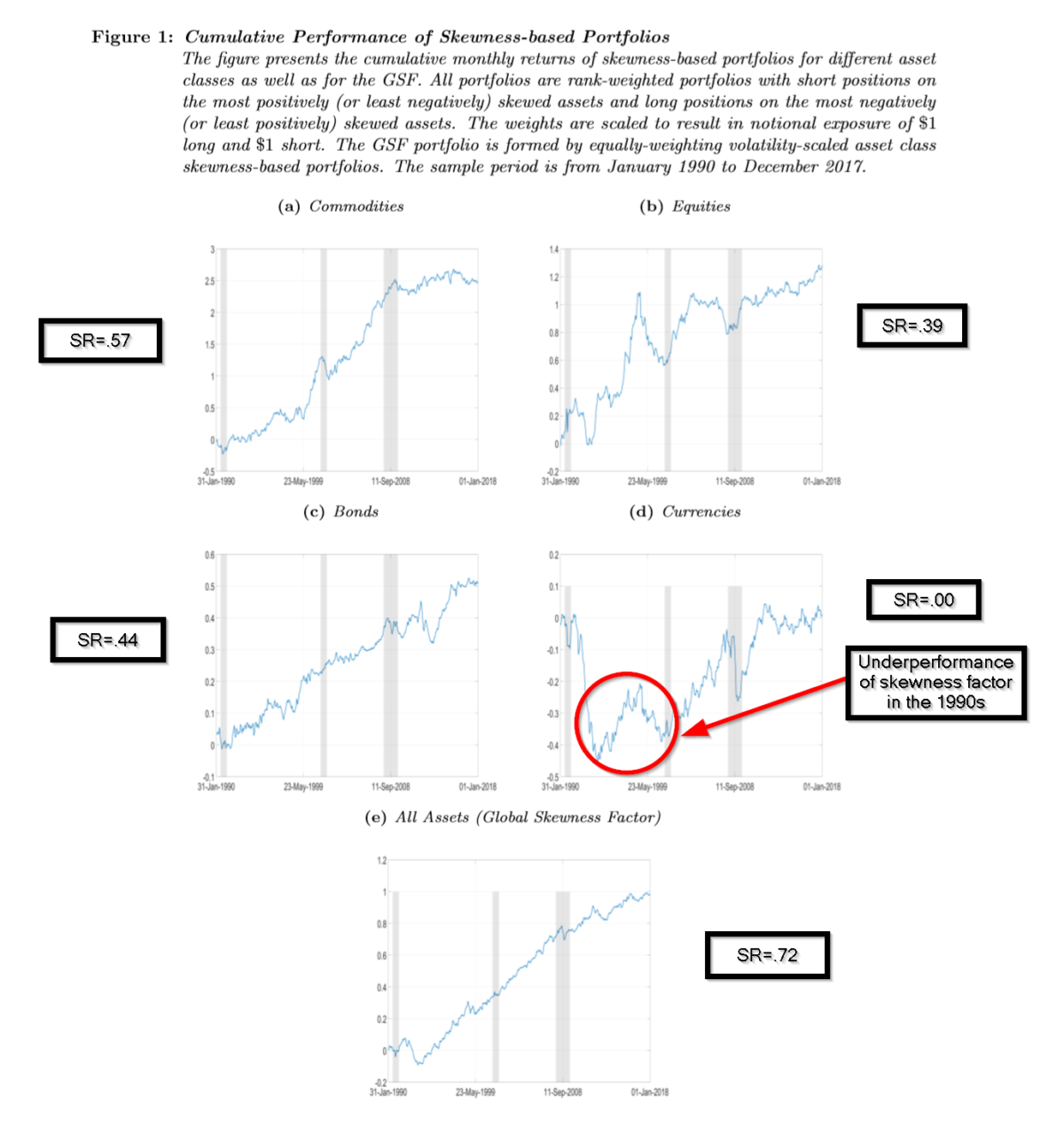

- YES. Generally speaking, taking on skewness risk is systematically rewarded within and across global asset classes. Negative skewness is associated with positive excess returns with significant Sharpe Ratios (SR) for all asset classes with the exception of currencies. The results are reported in Figure 1. However, it is interesting that the skewness portfolios exhibit very low correlations across asset classes: .13 for equities and bonds; .14 for equities and currencies, suggesting the value of diversifying skewness portfolios across asset classes and global markets. The impact on volatility from combining skewness portfolios can be seen in the SR (.72) for the Global Skewness Factor (GSF) portfolio, a cross-asset diversified global portfolio.

- YES. Controlling for commonly accepted risk factors (value, momentum, and carry), leaves the skewness factor intact and statistically significant. The authors also conduct mean-variance spanning tests by constructing efficient multifactor portfolios within and across asset classes. They report a positive allocation to the skewness factor for portfolios that include value, momentum, and carry. For example, the minimum-variance portfolio contained a positive allocation of at least 10%.

- 3 REASONS. (1) Investors (most likely retail investors?), may have an illogical desire for assets with “lottery-like” characteristics that cannot be arbitraged away due to short-selling restrictions (Mitton and Vorkink, 2007; Bali, Cakici, and Whitelaw, 2011); (2) Investor behavior may overprice positively skewed securities. For example, behavior that overestimates events with a low probability of occurrence, with a consequent reluctance to short positively skewed securities in order to avoid the chance of large negative returns. Similarly, investors would be unwilling to invest in negative skew securities in favor of shorting the same in order to reap a possible large positive return (Barberis and Huang, 2008); (3) Selective hedging depending on an investor’s view of the need to hedge. Positively (negatively) skewed securities would exhibit a net long (short) hedging demand (Stulz, 1996). For example, commodity traders tend to construct more long (short) hedges in positive (negative) skewed commodities.

Why does it matter?

The main takeaway from this article is the documentation of skewness as a factor explaining the cross-section of security returns. Taking on skewness risk is apparently well-compensated within and across global asset classes, which adds to the considerable literature (should I say “zoo”?) on factors. What is interesting about this piece is the nod to the theoretical basis for why the skew premium might exist. There appears to be considerable work published on the dynamics of investor preference for skewness, which is not only a relief but also imparts confidence in the results.

The most important chart from the paper

Abstract

We find that realized skewness is a significant indicator of returns across a range of assets from different asset classes, namely commodities, government bonds, equity indices and currencies. Taking on skewness risk is broadly compensated within, but more substantially across asset classes. Portfolios in these four asset classes with long positions on most negatively (or least positively) skewed assets and short positions on least negatively (or most positively) skewed assets generate on average a Sharpe ratio of 0.35 between 1990 and 2017. We find little evidence of a common risk driver among these portfolios, to the extent that their combination benefits substantially from diversification, delivering a Sharpe ratio of 0.72. The patterns are not subsumed by other known factors that drive returns, such as value, momentum or carry factors and, consequently, mean-variance efficient multi-factor portfolios assign a positive weight to skewness. Our results remain robust to different measures of skewness and across sub-samples.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.