Interested in starting an ETF? Interested in converting a managed account, hedge fund, or mutual fund into an ETF? Simply want to learn more about the process of launching an ETF? This piece is an introduction to ETF white label services, the industry term for a firm that helps an “ETF-prenuer” bring an idea to the public market.

We will map out the following:

- the typical use cases for an ETF,

- the basic process to launch an ETF,

- the high-level costs of launching an ETF,

- and the niche group of specialized providers who can help you bring an ETF to market.

Editor’s Note: there is a podcast version of this post, which is a nice follow-up to reading this article. Recently, we did a follow-up podcast with Pat Cleary. Audio/visual learners should check these out.

Before we dive in on ETF white label services, we’ll share our story of how we ended up in the ETF business.

The Alpha Architect story

Not many people know the history of Alpha Architect. I’ll spare you the details because it involves 3 failed attempts in the asset management business, including the launch of a small value quant hedge fund in September 2008. Great timing, eh? Building a solid investment strategy is one thing. Building a solid investment business adds a set of challenges.

After getting punched in the face several times, we finally caught a lucky break. Alpha Architect was formed in July 2010 and was eventually seeded by a huge family office in 2012. Several years later, we launched an ETF business via angel funding from an SMA client in late 2014. We essentially took the investment strategies from separately managed accounts (private) to the world via ETFs (public) as we believe ETFs were a superior structure.

Fast forward to 2020. We’ve managed to spend a decade strategically minimizing the chance we ever have to get a real job, and I’ve managed to lose 95% of my hair. Some may not consider this success, but hey, we are living our adventure, and we don’t have to file TPS reports, so not all is lost!

All joking aside, why bore you with our history? We want to emphasize that we strongly empathize with entrepreneurs and the challenges they face to get a financial services business started. We’ve been there. But now that we’ve survived for a decade in a cutthroat business, we sometimes forget just how challenging the world can be for new business owners who seek to bring their ideas to the financial marketplace.

Case in point: Perth Tolle.

I originally ran into Perth at an ETF.com conference in Florida. Perth pitched me on her passion for ETFs, her passion for freedom, and her desire to combine the two concepts. I was 50% sold. Freedom sounded great.(1) However, I was a bit sour on the other 50% — the whole “launching an ETF” aspect of the deal. After bearing witness to the insane competition in the ETF industry, along with the high fixed costs of launching an ETF, the prospects of launching someone else’s ETF idea weren’t exciting. I politely told Perth, “No thanks.”

Fast forward to 2018. Perth continued to express her passion for launching an ETF. I kept providing obstacles: “Where’s your funding?” “Where are your investors?” “Do you know how terrible the ETF business is these days?”

And then I provided excuses: “We don’t want to open our ETF platform. We don’t have the bandwidth to deal with this right now.” The back and forth continued. Perth was the hungry entrepreneur, I was Mr. No.

But to Perth’s credit, she addressed every obstacle we put in front of her: she raised operating capital and identified some heavy-hitting investors. She convinced us we could open our ETF operating platform and help ETF-prenuers enter the game. We were sold. Alpha Architect was going to enter the so-called “ETF white-label business” and offer our infrastructure and know-how to help ETF-preneurs fulfill their dreams.

Why Launch an ETF?

The ETF structure is certainly not a panacea, and every investment delivery vehicle has different strengths and weaknesses.

Here are some basic costs and benefits of the ETF wrapper versus other investment vehicles:

- Potential costs

- High fixed costs (i.e., a magnitude more expensive than launching an LP or SMA)

- High transparency (i.e., the world will know what you own)

- Distribution transparency challenges (i.e., hard to identify who sold what)

- Potential benefits

- Transparency (i.e., the world will know what you own). This can be positive or negative depending on the audience.

- Tax efficiency (i.e., the potential to defer capital gains on equity, bond, and options instruments via in-kind transactions)

- Market access (i.e., type in a ticker, and the buyer is now a proud owner of your investment strategy)

- Operational efficiency (i.e., one can manage a tactical strategy via one ETF versus 1,000 SMA accounts)

Case Studies

Here are the typical use cases we have seen:

- Asset manager (e.g., hedge fund manager or mutual fund manager) with an active stock selection strategy looking to gain operational efficiency and the tax advantages of the ETF

- Note that we can turn hedge funds into ETFs in a tax-free transaction. Multiple restrictions apply, but it is possible.

- RIA looking to simplify its trading operations and improve tax-efficiency

- It is now possible under certain circumstances to transform a managed account book into an ETF in a tax-efficient manner.

- Research and development firms with unique intellectual property and a broad audience that seek to monetize their IP via asset management

What are the Basic Requirements for Launching an ETF?

The process for launching an ETF can be broken into four phases:

- Planning

- Pre-launch

- Launch

- Ongoing management.

We include some generic timelines for each phase, but these vary wildly depending on the situation. On one extreme, if you are squared away, and we have some luck on the responsiveness of regulators, we can get an ETF launched in 3-4 months. On the other hand, if you require more coaching, are trying to do something extremely innovative, and have bad luck on the regulator front, it might take 12 months + to launch an ETF.

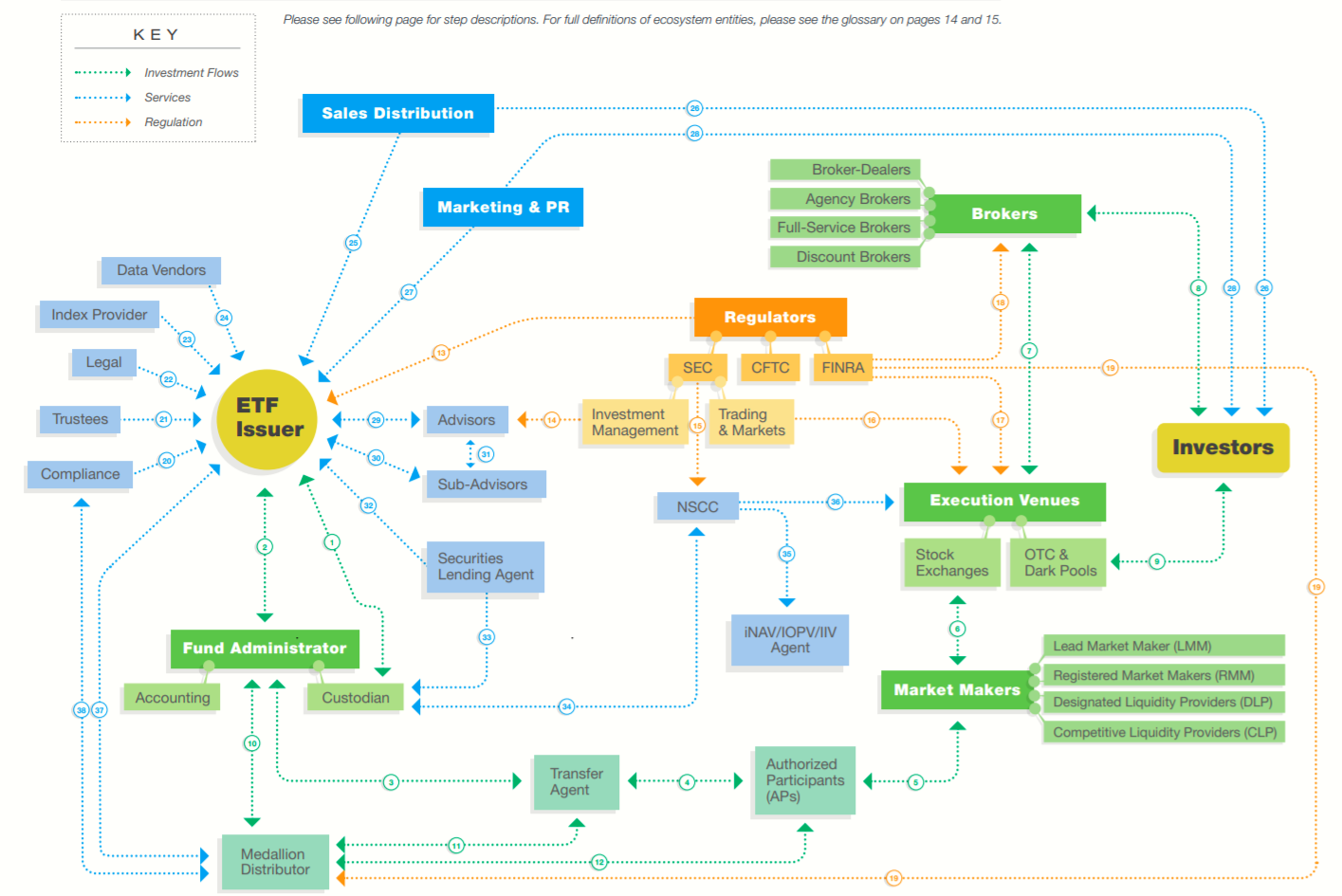

Arro Financial Communications has a great piece outlining the various aspects of the ETF ecosystem and how they all fit together. The graphic below is a snapshot and highlights the complexity involved.

As a potential ETF-prenuer, just know that our job is to deal with the mess below; your job is to build interest in your intellectual property and identify capital to fund your ETF adventure.

Below, I outline each of these phases and how we would tackle them. Other parties likely follow a similar path.

1. ETF Planning Phase (0 to 6 months)

- Implementation Timeline

- Regulatory workplan

- Marketing/Distribution workplan

- Economics, pro forma finalization

- Contracting, licensing as needed

- Competitor analysis (Is this product unique? How should it be priced? Why has it not been launched already? etc.)

2. ETF Pre-Launch Phase (2 to 6 months)

Pre-launch is the second phase of bringing an ETF to market. This phase is fairly work-intensive for our side and your side. Be prepared to put the time in so your ETF launch is a success. A few of the items we’ll take care of in this phase are as follows:

- Index creation/data construction (this is only a requirement if you choose the Index path versus the active path)(2)

- Registration/prospectus drafting (a heavy legal lift)

- Iteration with regulatory agencies (i.e., SEC). This process can vary depending on the idiosyncrasies of the SEC.

- Data controls established

- Vendor management (who are we using for the various pieces that require outsourcing)

- Board approval, Trustee engagement (we present your idea to our Board, which has ultimate authority on whether or not we can launch your strategy)

3. ETF Launch Phase (1 month)

The launch is the third phase of bringing an ETF to market. At this point, the plan is in motion, and it is time to execute. A few of the items we’ll take care of in this phase are as follows:

- Basket Creation

- Exchange listing completion (coordinate with CBOE, Nasdaq, or NYSE)

- Marketing coordination (prepare websites, factsheets, etc.)

- Capital markets management

- Seed capital deployment(3)

- Index coordination (as required)

4. ETF Management Phase (Ongoing)

Ongoing management of the ETF is the final phase of the ETF process. We are officially live, and it is time to share your wonderful idea with the investing public. A few of the items we’ll take care of in this phase are as follows:

- Vendor management

- Printing/filing

- Regulatory disclosures

- Liquidity assessments and filings(4)

- Ongoing marketing

- Invoicing/vendor payments

- Trading and execution

- Dedicated compliance team supported by external counsel

How Much Does it Cost to Launch an ETF via an ETF White Label Platform?

Launching an ETF is a highly complex operation with many moving pieces, which means the precise cost estimate will depend highly on the situation. However, the items below will give the aspiring ETF entrepreneur the ballpark all-in costs for a standard US-equity-only, quarterly-rebalanced, in-kind ETF. These costs are associated with the “white-label” option.(5)

We break our cost estimates into 4 components:

- Start-up costs

- Fixed costs

- Initial variable costs

- Scale variable costs

1. Start-Up ETF Costs:

Start-up costs cover all the costs of the initial consultations during the planning and pre-launch phase and the costs to get the legal and compliance documentation prepared and finalized. The all-in costs for a non-frills, fairly generic fund are typically around $50,000, but this figure can vary wildly depending on several factors. The costs for an ETF start-up can easily range from $40k to $150k+.

Here is a rough breakdown of the items included:

- Launch fee

- Registration Statement

- SEC Filings/XBRL

- Board meeting/Prep

2. Fixed ETF Costs:

We have tried to make the pricing on ETF white label as transparent as possible. In our own experience, the pricing typically involves some sort of fixed element, with a million footnotes highlighting random “nickel and dime” costs. Well, when you add up the nickels and dimes, they end up being material costs. So, our fixed costs estimate internalizes and underwrites everything into one simple figure (if you want a more detailed assessment, reach out).

All-in, you are looking at around $175k to $200k+/year (But this can range from $190k to $300k+). If you are looking to trade in international markets where custody costs are presumably higher, the costs will increase. Also, if the ETF cannot be traded “in-kind” there will likely be additional costs. Of course, there are other circumstances where the fixed costs could be lower. Again, this is a high-level estimate and a starting point for a discussion. We always seek to deliver affordability, so ETF sponsors have the best chance to survive in the ETF business!

The key elements included in these fixed costs:

- Trust infrastructure

- Fund compliance/legal

- Insurance

- Advisor compliance/legal support

- Portfolio management services

- Audit/Tax

- Fund administration

- General consulting/guidance

3. Initial Variable ETF Costs:

In addition to the fixed costs, there are several variable costs that we pass through to ETF servicing clients. These costs grow with your fund and are ‘triggered’ from day 1.

These include the following:

- Custody costs

- Marketing material review costs from our broker/dealer partner and FINRA

- SEC fees (24f-2 fees)

- Printing fees

- Independent Trustee Counsel fees (as it relates to your specific ETF)

We typically advise that these costs will be around $15k to $25k/year but can vary considerably depending on your unique situation.

4. Scale Variable ETF Costs:

In the beginning, an ETF operation is dominated by fixed costs and the variable costs mentioned above, however, at scale, there are additional variable costs.

As part of our pricing schedule, we pass through scale variable costs that cover the costs we incur from our own operations and service providers. These costs also cover higher insurance costs, adding portfolio management complexity and other costs that naturally scale with more AUM.

The scale variable costs are additional costs on top of the fixed costs and variable costs mentioned above:

- 6-15+ bps on AUM above $100M and below $250M

- 4-15+ bps on AUM above $250M and below $500M

- 4-12+ bps on AUM above $500M

- 3-8+bps on AUM above $1B

A Quick Example of ETF profit/loss

Let’s say you launch an ETF, the fund scales to $400mm, and you charge 50bps (an incredibly smashing success). We will also assume you are in the mid-range on the estimates above.

Here is the generic profit/loss breakdown:

- Revenue = 50bps* 400mm = $2mm

- Servicing costs: $225k fixed costs + 8bps(250mm-100mm)+6bps*(400mm-250mm) = 225k +120k + 90k = 435k

- Variable costs: $10k custody + $400 * (129.80) + 15k marketing materials (6) = 77k

- Gross profits = $2mm – 435k – 77k = ~1.5mm

Again, the discussion above is meant to get the aspiring ETF-prenuer oriented on the ballpark costs they can expect to face when launching an ETF.

The key takeaway is that launching an ETF is not a simple or cheap operation. Before tackling this endeavor, you’ll want to have the operating capital necessary to manage operations for at least 3 years and have a reasonable ability to attract new investors over time.

Who Can Help You Launch an ETF?

The ability to provide full-spectrum ETF white-label services is a fairly unique skill set, so the options available are fairly limited. Launching an ETF is akin to getting married, so you should rely heavily on the incentives and integrity of the service provider.

We recommend you talk to several ETF white-label providers and ensure there is a good cultural fit. When you partner with an ETF white-label provider, you are effectively entering a strategic relationship. As many in the industry have learned (e.g., HACK), the ETF servicing counterparty is critical to your long-term success as an ETF sponsor.(7)

We are also big believers in “skin in the game” regarding ETF white-label providers. Does your provider have their own funds on their platform? This helps align incentives between the white-label service provider and the ETF sponsor. Platforms provided by fund administration groups and custody banks may have incentives that are not aligned with the ETF sponsor.

Finally, one needs to consider how much brain damage one will incur when dealing with an ETF white-label provider. Some providers are “one-stop shops” (like us), and others are a “hodge-podge” of service providers. Some providers will present you with multiple invoices; some will provide you with a single invoice (like us). Some providers will require a full-time employee to manage the ETF white-label provider simply; some will require a part-time effort, at best (like us).

In short, costs are always important, but they aren’t the most important aspect when considering a strategic partner in the ETF business.

ETF White-Label Services Providers

Our own services (i.e., ETF Architect): obviously, we know this offering the best because we offer it and use it for our funds! We lean on our technical know-how and current ETF operations to provide what we believe to be the most affordable and transparent ETF white-label service in the market. However, if you are looking for dedicated direct distribution/sales support on your product, we may not be the best option. We can connect you with various providers/individuals that specialize in marketing products for 3rd parties. Still, we will not focus on selling your product (see the option below if you are looking for dedicated distribution services in addition to white-label services).

Tidal ETF services: Mike Venuto et al. offer white-label services with a comprehensive offering similar to ours. Their platform includes strategic guidance, product planning, trust, and fund services, legal support, operations support, marketing and research, sales, and distribution support services. They also offer access to the ETF Think Tank, which shares ETF Ideas, thought leadership, strategies, tools & growth tactics. If you are looking for ETF services plus heavy support on sales and distribution, we recommend you talk to Mike and explore their offering (contact us, and we’ll put you in touch directly).

US Bank ETF Services: Mike Castino and his team offer their services via the US Bank series trust. Like our platform, they focus on affordable access to the ETF market but do not provide distribution and portfolio management services. Also, because their platform is a shared platform across many funds, flexibility is fairly limited. That said, if you are looking for a service offering directly from a custody bank, the US Bank offering is the best on the market, in our opinion.

The options above will end up being roughly the same cost, depending on the services required. There are some additional options on the market, including Exchange Traded Concepts and the ETF Manager’s Group. Still, we are less familiar with these firms and their offering (our understanding is they are generally more expensive but can offer additional services).

If you are bold, you can always build your own vertically integrated ETF shop. The up-front costs to create an enterprise with full ETF trading and execution capabilities, professional compliance/operations support, and the numerous systems and know-how required to facilitate a professional ETF operation are substantial (i.e., millions of dollars). Not to mention the ongoing costs of operations. That said, with enough money and enough gusto, you can achieve anything. We’ve proven that to be the case; however, just because something is possible doesn’t mean it is a recommended course of action.

Finally, you can also explore a hybrid DIY/outsource solution. You could build your Trust and compliance and outsource the complex ETF portfolio management via a sub-advisory relationship with either Vident (speak with Amrita) or Penserra. These firms are highly professional and do a great job managing the brain damage associated with ETF portfolio management.

If you are interested in going the full “DIY route” or partial DIY, we can help point you in the right direction. Reach out.

Conclusion on ETF white label services

We believe the tax efficiency, transparency, and low-cost nature of the ETF structure will ensure that the investment vehicle remains a favorite for investors in the future. Setting up an ETF is a serious endeavor that requires a full commitment. We encourage asset managers and financial advisors to explore the vehicle as a potential way to enhance their client experience. We fine-tune their value proposition in a highly competitive market. Please reach out if you have any questions — we are here to help, and we seek to support all ETFprenuers!

The contact form is below:

References[+]

| ↑1 | Semper Fi, Do or Die, Hang ’em High on Eighth and I! |

|---|---|

| ↑2 | Note that there are trade-offs between going down the index ETF route and the active ETF route. The index route has some potential marketing freedom benefits (index providers are not regulated by the SEC), but there are also some limitations with this approach. If you choose the active ETF route, you will serve as a discretionary or a non-discretionary sub-advisor to the fund. This role requires you to maintain an SEC registration and conform to more common compliance & regulatory requirements. We can walk you through the nuance as we get into the process. |

| ↑3 | Seed capital is provided by a broker/dealer serving as an authorized participant in the fund. The minimum seed is 100k shares, typically priced at $25/share, so you are looking at a 2.5mm seed initially. We will coordinate with our AP partners to solve this crucial process component. |

| ↑4 | This includes N-Port filings. We can provide N-Port filing services to registered funds at a much lower cost than the competition. Please contact us for more information. |

| ↑5 | If one decides to start from scratch and create their own Trust structure, trading and execution capability, compliance/legal infrastructure, and so forth, the costs will quickly get into the “millions of dollars” range. |

| ↑6 | SEC rate is currently 129.80 per million dollars AUM |

| ↑7 | This risk is arguably limited since our friend Andrew Chanin and Nasdaq were successful in their lawsuit against the white-label provider |

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.