Core Research Categories

Click Here for Category Archive

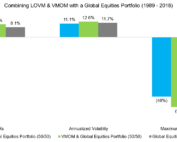

Low Volatility-Momentum Versus Value-Momentum Factor Portfolios

March 13th, 2020|

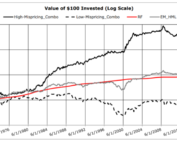

The Massive Performance Divergence Between Large Growth and Small Value Stocks

February 21st, 2020|

Factor Investing Update: An Analysis of 2019 International Factor Returns

February 19th, 2020|

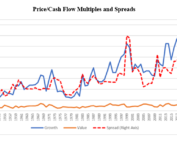

Enterprise Multiples and Expected Stock Returns

January 21st, 2020|

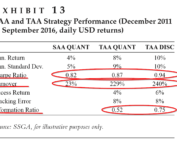

Asset Allocation vs. Factor Allocation—Can We Build a Unified Method?

December 30th, 2019|

Click Here for Category Archive

Accruals and Momentum and Their Implications for Factor Investors

September 17th, 2020|

Cross-Asset Signals and Time-Series Momentum

August 6th, 2020|

Fundamental Momentum, the Carry Trade, and Currency Returns

July 23rd, 2020|

Left Tail Risk and Left Tail Momentum

July 14th, 2020|

Combining Momentum with Long-Term Reversal

July 3rd, 2020|

Value Factor Diversification: Is Quality Better Than Momentum?

June 26th, 2020|