Core Research Categories

Click Here for Category Archive

Betting Against Beta: New Insights

April 28th, 2022|

2022 Democratize Quant Conference Recap and Materials

March 25th, 2022|

Our 5th Annual Democratize Quant 2022 is Live. Sign-up!

March 9th, 2022|

New Accounting Standards and Factor Investing

March 7th, 2022|

Is The Value Premium Smaller Than We Thought?

February 3rd, 2022|

Factor Investing in Sovereign Bond Markets

January 13th, 2022|

Click Here for Category Archive

Novel explanations for risk-based option momentum

April 25th, 2023|

How factor exposure changes over time: a study of Information Decay

April 17th, 2023|

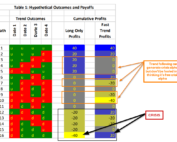

Combining Reversals with Time-Series Momentum Strategies

April 7th, 2023|

Can We Improve Momentum Factor Investing via Salience Theory?

March 6th, 2023|

Does Momentum work in Option Markets?

November 21st, 2022|

Is there a theoretical foundation behind industry and factor momentum

November 14th, 2022|

Click Here for Category Archive

Smart Money Indicator Rebuttal

February 28th, 2020|

Daily vs. Monthly Trend-Following Rules…Plus Some DIY Tools!

April 7th, 2020|

Trend Following is Everywhere

April 23rd, 2020|

How Trend Following Strategies Shape Return Distributions

June 29th, 2020|

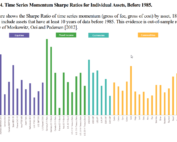

Time Series Momentum: Theory and Evidence

June 30th, 2020|

Click Here for Category Archive

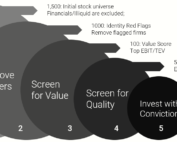

The Quantitative Value Investing Philosophy

October 7th, 2014|

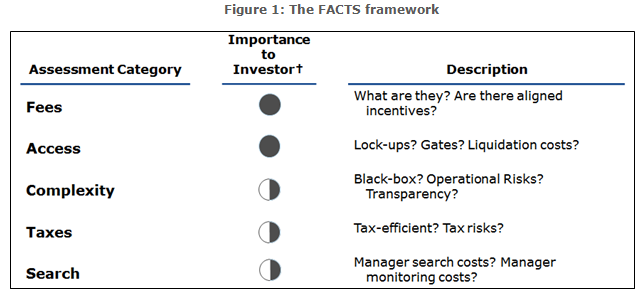

A Framework for Investment Manager Selection: Stick to the FACTS

September 16th, 2014|

Our Value Proposition: Affordable Alpha

September 16th, 2014|

A Simulation Study on Simple Moving Average Rules

July 28th, 2014|

Momentum Investing: Ride Winners and Cut Losers. Period.

July 16th, 2014|

How to Build Expected Return Forecasting Models

July 14th, 2014|