Human bias in algorithmic trading

- John Broussard, Andrei Nikiforov

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category!

Abstract:

This paper documents a stark periodicity in intraday volume and in the number of trades. We find activity in both variables spikes by about 20% at regular intervals of 5 or 10 minutes throughout the trading day. We argue that this activity is the result of algorithmic trading influenced by human traders/programmers’ behavioral bias to transact on round time marks. An alternative explanation, that algorithms choose to concentrate their trades in time to take advantage of lower costs or to protect themselves from better informed traders, is not supported.

Data Sources:

Nanex, 2003 to 2006.

Alpha Highlight:

Trading takes place at specific time intervals. Why didn’t the programmer tell the algo to trade at random times?

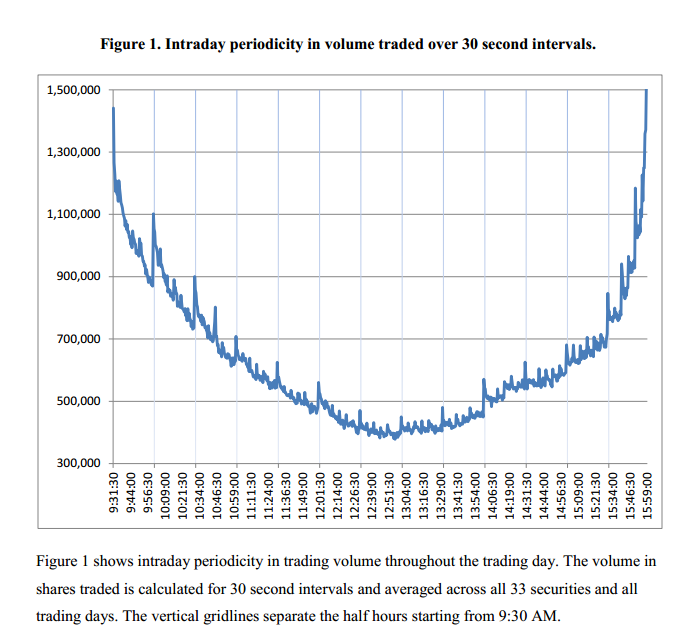

Trading volume spikes every 5 or 10 minutes and returns to normal volumes 30 seconds later.

Strategy Summary:

- Paper finds that trading activity explodes on round time marks, such as every half hour.

- Trading data (from Nanex) are quoted from 30 liquid U.S. stocks and 3 ETFs from April 17, 2003 to Oct 18, 2006, or a total of 882 trading days.

- Figure 1 shows aggregate volume exhibits U-shaped pattern with sharp spikes in every 5 to 10 minutes.

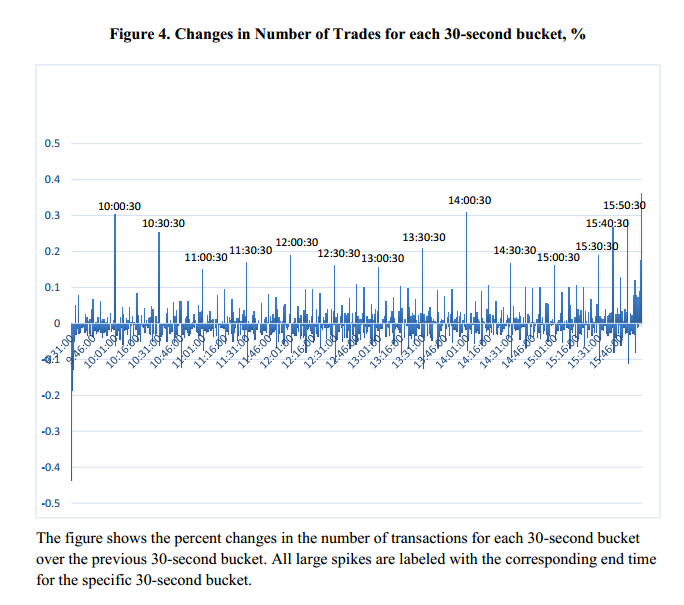

- Figure 2 shows percent changes in volume for each 30-second and spikes occur at highly regular intervals (30 minutes apart).

- Trading data (from Nanex) are quoted from 30 liquid U.S. stocks and 3 ETFs from April 17, 2003 to Oct 18, 2006, or a total of 882 trading days.

- Paper then tests two competing hypotheses to explain this increased activity.

- Hypothesis 1: Round Numbers Hypothesis

- Theory is that humans have a tendency towards round numbers when faced with decisions.

- Test: Paper regresses the volume and trade variables on various non-overlapping time dummies to examine whether clustering is progressively more intense as the markers on the time line becomes more and more round.

- Time dummies correspond to round hour marks (10:00 AM), half-hour marks (10:30 AM), fifteen minutes marks (9:45 AM and 10:15 AM), ten minutes marks (9:40 AM and 10:10 AM), and 5 minutes marks (9:55 AM and 10:05 AM).

- Table 2 shows average volume increases on the corresponding time marks, indicating that humans tend to prefer round numbers.

- Hypothesis 2: Rational Concentration Hypothesis

- Theory is that liquidity traders tend to cluster trading to protect themselves from better informed rivals (insiders) and take advantage of increased liquidity and reduced transaction costs.

- Test: Paper calculates 5 measures of transaction costs and 1 measure of price impact (see p11) and then, regresses each liquidity variable on various time dummies to check whether there is a significant improving in liquidity on the round time marks.

- Table 3 shows that five measures of liquidity do not change in any significant way during the spikes (fails to support hypothesis 2).

- Results: Inclined to attribute the clustering to the human preference for round numbers rather than to a rational optimizing activity of traders and their algorithms.

- Hypothesis 1: Round Numbers Hypothesis

Strategy Commentary:

- Documents the behavioral bias the people prefer to use round numbers when faced with a task in an uncertain environment.

- Good summary of the literature with examples of humans’ bias towards round numbers (in financial economics, psychology, and marketing).

- This paper makes sense! When was the last time you scheduled a meeting at a time not ending in a 0 or 5?

- Recommend meeting at 9:37 and see what reaction you get.

Wonder how many “algo hunters” are taking advantage of this already?

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.