Jason Zweig’s book, “Your Money and Your Brain” highlights an interesting conversation with Harry Markowitz. Dr. Markowitz is a Nobel Prize winner and his work on mean-variance-analysis laid the foundation for all of modern portfolio theory.

Not too shabby for a financial economist.

We’ll come back to the quote in a moment, but first let’s review some general observations on Markowitz’s mathematically sophisticated approach to asset allocation.

Although Markowitz did win a Nobel Prize, and this was partly based on his elegant mathematical solution to identifying mean-variance efficient portfolios, a funny thing happened when his ideas were applied in the real world: mean-variance performed poorly.

The fact that a Nobel-Prize winning idea translated into a no-value-add-situation for investors is something to keep in mind when considering any optimization method for asset allocation.

The cautionary tale regarding mean-variance-based model performance heavily influenced the lecture I gave a few weeks ago at the Morningstar ETF conference where I presented the following slides.

My key takeaway from the chat was that COMPLEXITY DOES NOT EQUAL VALUE.

I supported this statement by highlighting that a variety of complex tactical asset allocation frameworks can’t stand toe-to-toe with the simple 1/n, or equal-weight asset allocation model.

Why Do Complex Models Fail?

Estimating the covariance matrix is notoriously unstable, so therefore, the “optimized” weights spit out from a model influenced by an unstable covariance matrix would also end up being unstable and unreliable. (For a detailed discussion of this issue, you can review the “Complexity” section in this post from about a month ago)

The proof is in the pudding: equal-weight allocations seem to reliably beat complicated allocations.

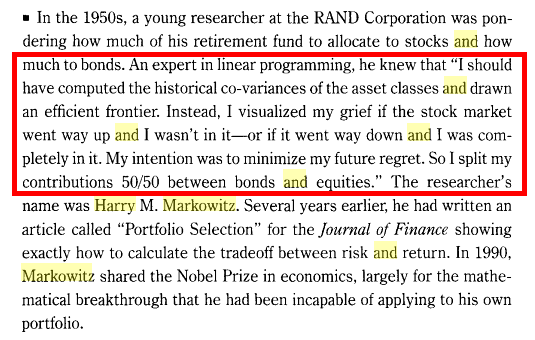

Not soon after the Morningstar event, one of my partners–Jack Vogel–ran across a quote by Harry Markowitz that was fairly amusing:

I should have computed the historical covariance of the asset classes and drawn an efficient frontier…I split my contributions 50/50 between bonds and equities.

In this context, Markowitz’s discussion is meant to highlight the power of behavior over reason. Markowitz pokes fun at himself: he knew he should have followed his own elegant model, but instead he ignored it. There’s an irony here: in light of a few more decades of out-of-sample evidence, it turns out his behaviorally-driven decision (i.e., equal-weight simplicity) probably really was the correct approach after all.

So the founder of modern portfolio theory uses an equal-weight allocation. And one of the central assumptions underlying mean-variance optimization is that investors care about risk and return trade-offs. Yet, as Markowitz highlights, his decision-making framework has little to do with risk and return trade-offs. In the year 2014, now that we have a long enough data trail, we can show that Markowitz’s model doesn’t outperform a simple equal-weight allocation. The reason for this underperformance is a not critique on the model, which is clearly an incredible intellectual achievement, but has everything to do with the practical realities of accurately estimating a covariance matrix. So Markowitz’s 1/N approach was right, but for the wrong reasons. He was right that a simple 1/n allocation strategy was appropriate, but his reason – that he wanted to minimize his future regret – was the wrong one. The right answer is that good models don’t necessary translate into good practical ideas.

Holy cow. Someone should write a financial economic soap opera on this story…

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.