Digesting Anomalies: An Investment Approach

- Hou, Xue, and Zhang

- A version of the paper can be found here

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category!

Abstract:

An empirical q-factor model consisting of the market factor, a size factor, an investment factor, and a profitability factor largely summarizes the cross section of average stock returns. A comprehensive examination of nearly 80 anomalies reveals that about one-half of the anomalies are insignificant in the broad cross section. More importantly, with a few exceptions, the q-factor model’s performance is at least comparable to, and in many cases better than that of the Fama-French (1993) 3-factor model and the Carhart (1997) 4-factor model in capturing the remaining significant anomalies

Alpha Highlight:

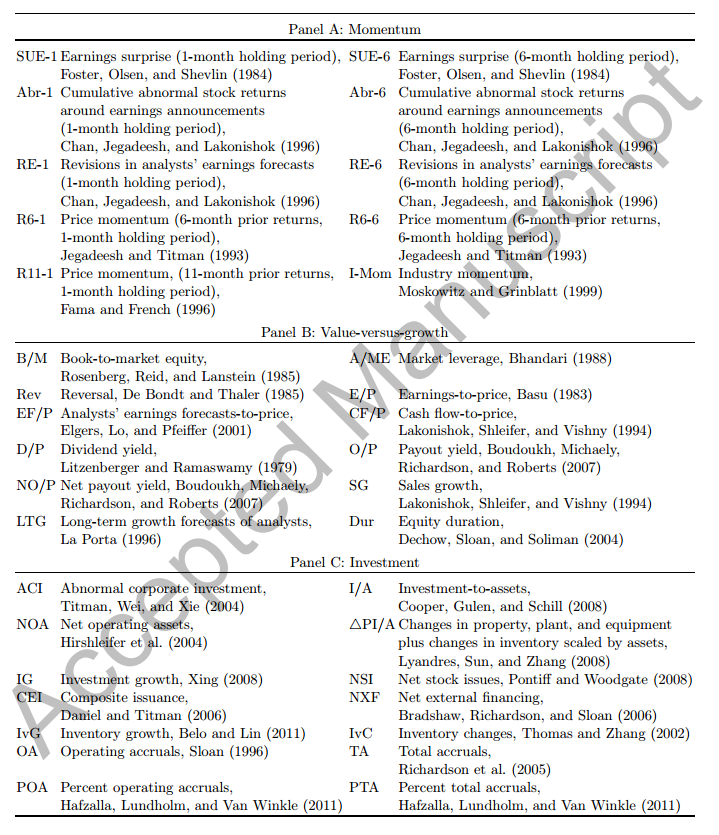

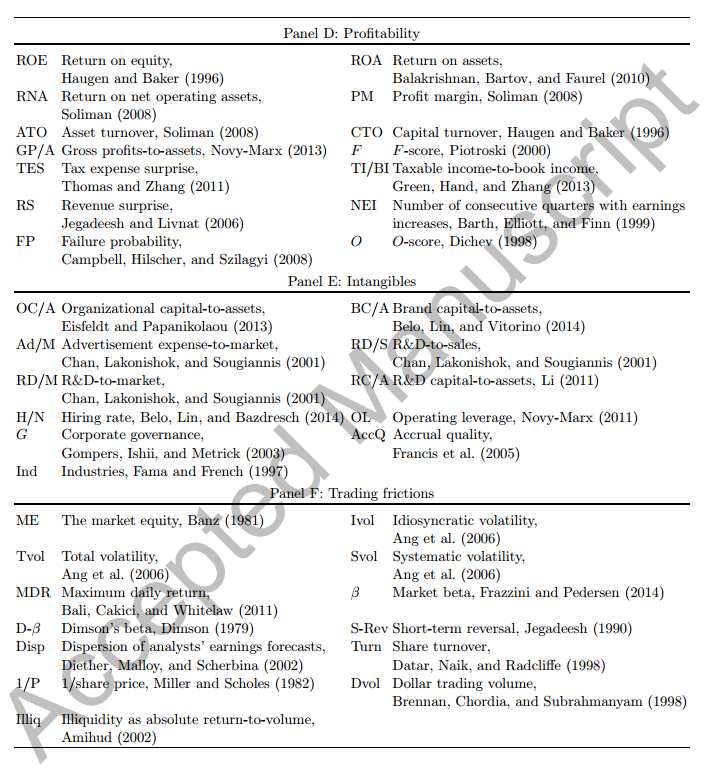

The laundry list of items tested…

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.