Masculinity, Testosterone, and Financial Misreporting

- Jia, Van Lent and Zeng

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Abstract:

We examine the relation between a measure of male CEOs’ facial masculinity and financial misreporting. Facial masculinity is associated with a complex of masculine behaviors (including aggression, egocentrism, risk-seeking, and maintenance of social status) in males. One possible mechanism for this relation is that the hormone testosterone influences both behavior and the development of the face shape. We document a positive association between CEO facial masculinity and various misreporting proxies in a broad sample of S&P 1500 firms during 1996-2010. We complement this evidence by documenting that a CEO’s facial masculinity predicts his firm’s likelihood of being subject to an SEC enforcement action. We also show that an executive’s facial masculinity is associated with the likelihood of the SEC naming him as a perpetrator. We find that facial masculinity is not a measure of overconfidence. Finally, we demonstrate that facial masculinity also predicts the incidence of insider trading and option backdating.

Alpha Highlight:

This may sounds nuts, but the authors in this paper examine the relationship between a CEOs’ facial features and their propensity to misreport financials. The hypothesis for why this relationship is causal is that a person’s physical characteristics (ex, fitness, height, or facial shape) predicts his/her personality characteristics (ex, aggressiveness, risk-taking, egocentrism).

This paper hypothesizes that a male CEO’s testosterone levels are linked to his masculine behavior, which are linked to financial misreporting. While it is impossible to get data on a CEO’s testosterone level, Stirrat and Perrett (2012) shows that male facial width-to-height ratio is a valid measure of his testosterone exposure during puberty, and this ratio has correlation with antisocial tendencies. The paper uses the Stirrat and Perrett metric as a proxy for testosterone.

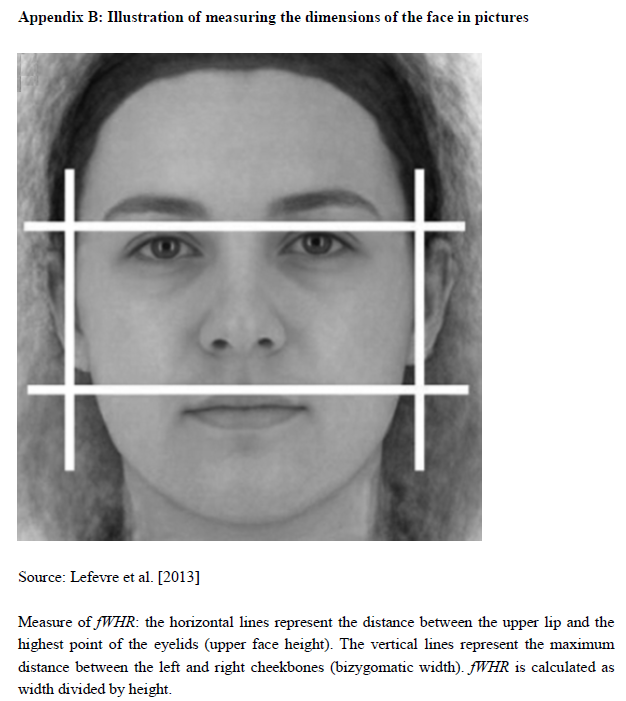

- Facial width-to-height ratio (fWHR): the distance between the cheekbones is the width and the distance between the upper lip and the highest point of the eyelids is the upper face height. fWHR is calculated as width divided by height.

The paper studies a sample of 1,136 CEOs from S&P 1500 companies in 2009. The authors manually collect each CEO’s measurable, high-quality, facing forward pictures from Google Images and calculate fWHR based on photos collected. Based on Stirrat and Perrett (2012), the above median fWHR represents more masculine facts.

To test the relation between financial misreporting and fWHR, the authors run a regression model as follows. D(fWHR>median) is a dummy variable that takes the value of “1” if a CEO’s fWHR is above the median and “0” otherwise.

Click to enlarge.

Key Findings:

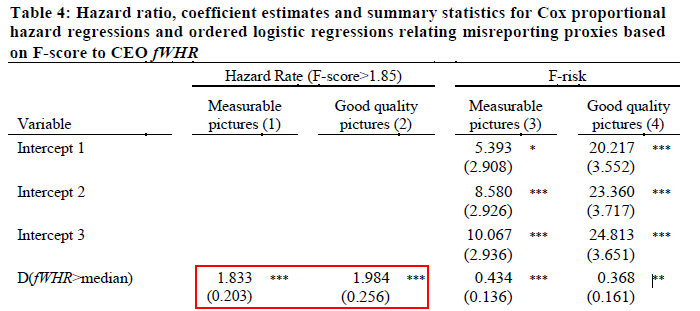

Facial masculinity matters! For CEOs with above-media fWHR, their risk associated with misreporting is up to 98% higher for CEOs with below-median fWHR.

Below is a part of Table 4 which shows the results of the regression. The coefficient on D(fWHR>median) in the proportional hazard model in column 1 (column 2) is 1.833 (1.984). Put it simply, CEOs with above-median fWHR face an 83% (98%) higher hazard of experiencing a substantial risk of misreporting than below-median-fWHR CEOs. (Column 1 and 2 differentiates on the quality of the pictures)

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Conclusions

This paper is hard to take seriously, but the authors do try their best to conduct a credible empirical analysis. You have to give the authors credit for thinking outside the box. I’m skeptical you can draw a causal conclusion from this research, but it is a thought-provoking finding nonetheless.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.