Beating a Dead Horse: Value investing and momentum investing work

At this stage in our lives we’ve essentially memorized the CRSP/Compustat database. Name an anomaly and we can probably tell you the stats on it fairly quickly.

Legitimate anomalies can usually be described via a behavioral finance lens:

- Can we identify poor psychology in the market? (Why do prices get dislocated along the way)

- Can we identify the limits to arbitrage? (Why don’t large pools of capital arbitrage the anomaly away)

There are 2 anomalies that stand out among all other anomalies: Value investing and momentum investing.

But don’t take our word for it, check out one of my favorite papers on the subject of “anomaly chasing:”

…and the Cross-Section of Expected Returns

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

You can find the entire laundry list of the papers examined here.

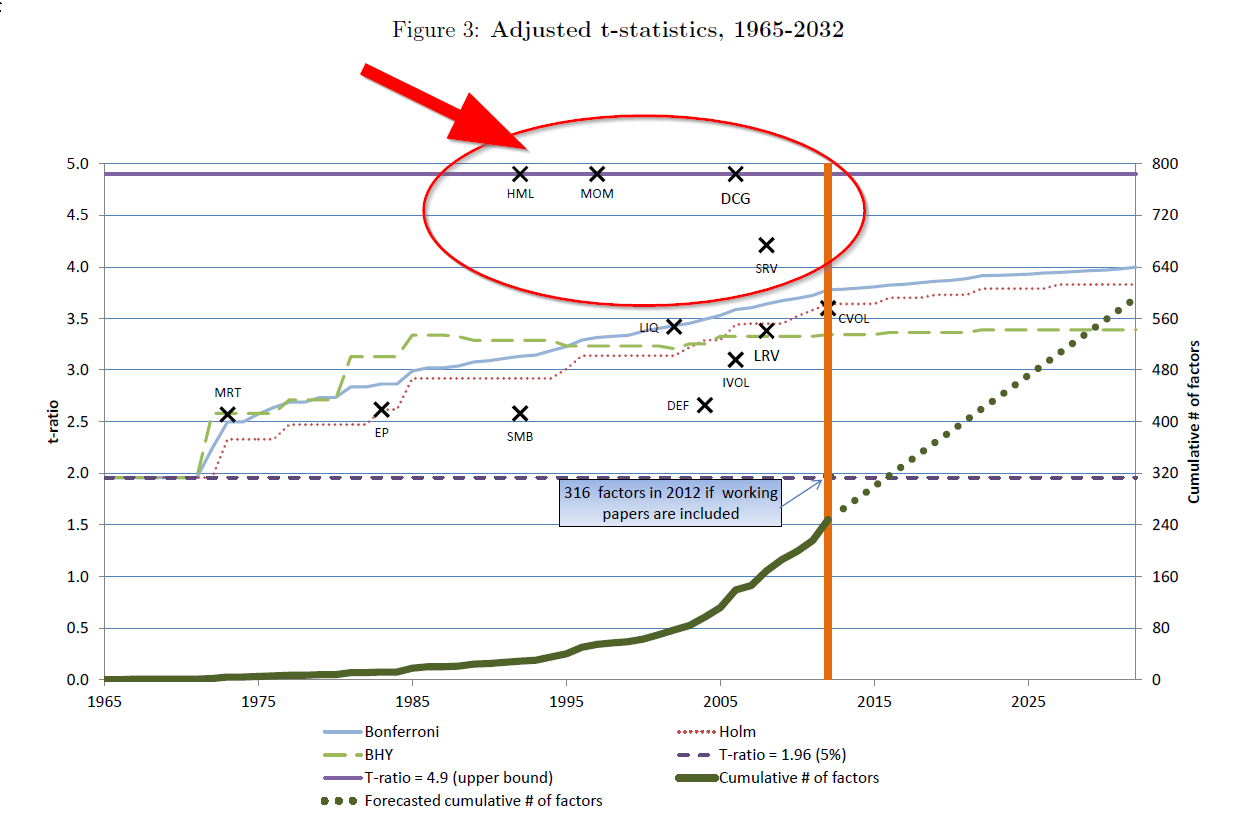

The authors argue that published papers suffer from serious data-mining efforts, and therefore, we need to adjust our statistical inference metrics to account for this fact.

We 100% agree with this insight.

And after considering this “high-bar,” there are only 3 anomalies that withstand the test of time: Value, Momentum, and Durable Consumption Goods (DCG). Value and momentum we know and love, whereas, DCG, while interesting, is a questionable strategy based on our internal research. (one can get the data here)

Perhaps more interesting is the fact that 300+ “anomalies” identified in the academic literature, once adjusted for data-mining, don’t pass the gauntlet. You’ll also notice that many of these strategies are wrapped in “smart beta” wrappers in the current marketplace.

Some examples:

- Dividend Yield

- Size

- Sentiment

- Liquidity

- Profitability

- Volatility

- Carry

- Beta

Are you buying a backtest? Or are you buying a sustainable alpha process?

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.