Insider Trading Patterns

- Cicero and Wintoki

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Abstract:

We find that corporate insiders trade over longer periods of time when they may have a longer-lived informational advantage. Controlling for the duration of insiders’ trading strategies, we find that isolated stock sales and purchases, and extended sale and purchase sequences (those spread over multiple consecutive months), predict sizable abnormal returns on average. We discuss how failure to account for these trading patterns has previously masked the returns to insider trading. Finally, we provide evidence that insiders attempt to preserve their informational advantage to maximize trading profits by disclosing their trades after the market has closed. When insiders report their trades after business hours they are more likely to engage in sequences rather than isolated trades, they trade more shares over more days, and the abnormal returns are larger on average.

Alpha Highlight:

“Insiders” are broadly defined under SEC regulations to be those who have “access to non-public, material, insider information.” We perceive “Insiders” as more like officers who hold C-level positions in a company and usually can get access to information earlier than anyone else.

Not all insider trades are illegal. Insiders can legally trade stock in their companies, so long as they adhere to the rules and report their trades to the SEC. Insider trades are broadly publicized, with insider trading data disclosed to the market in a timely manner. If you google around you can find numerous web sites, such as InsiderTrading.org, which offer information on insider trades.

So, what do insider trading signals indicate? When insiders are trading, does that mean we should trade too? Can we use insider trading information to make effective trading decisions? First, let’s investigate their trading patterns.

Short-lived vs. Long-lived Information

This paper sorts insider information into two types:

- Short-lived information is information that will be revealed to the market soon. For example, an insider of company A knows that the firm is likely to miss earnings in the near-term.

- Long-lived information is information that will be revealed to the market over a longer time frame (e.g., six months or more). For example, an executive of company B has been working on a negotiation with a key supplier that isn’t going well. But while this won’t affect performance in the near term, the information won’t be fully revealed until 6 months later.

Isolated Trading vs. Sequenced Trading

Insiders trade via two types:

- Isolated Trading: In order to act on short-lived information that will soon be incorporated into the stock price, insiders have to act very quickly before it becomes public. So they tend to engage in isolated trading, or even a single trade to benefit from the inside information. The paper defines isolated trading as trading that occurs when the insider did not trade the stock in the month before or the month after the isolated trading.

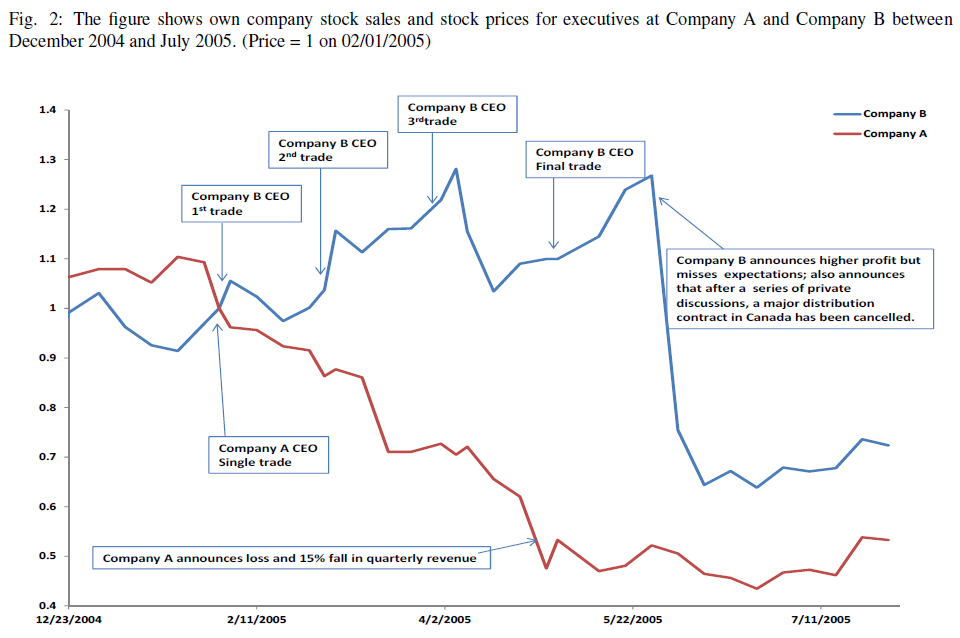

*For example, suppose Company A (the red line in Fig 2) was going to announce a loss around February 2005, so the CEO of company A engages in isolated trading (a single trade) immediately before earnings are disclosed.

- Sequenced Trading: When information is long-lived, however, the informational advantage will persist, so insiders tend to spread their trades over a longer period of time. The paper classifies trade months as “sequenced” if they occur in consecutive months.

*For example, company B (the blue line in Fig 2) won’t announce the failure of negotiations with a major distributor until May 2005. So Company B CEO can stretch his trades in a sequence of 4 separate trades across a longer horizon.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

What Do Return Patterns look like?

The paper finds that insider trading generates abnormal returns. Specifically, isolated trading usually comes with immediate abnormal return, since short-lived bad/good information is quickly incorporated into prices. On the other hand, no abnormal returns are found on sequenced trading until the sequences end. It is difficult for individual investors to profit from isolated trading since returns follow so quickly from the trading activity. However, we can take advantage of sequenced trading.

Trading Strategy

- Identify the end of a sequence of trade months by the second month after the final trade.

- Buy stocks after confirming the end of a sequence of insider purchases, and short stocks after confirming the end of a sequence of insider sales.

- One month later, re-balance the portfolio based on newly completed sequenced trades.

The paper highlights that such a strategy earns sizable abnormal returns, particularly when the focus is on the transactions of top executives.

A long-short portfolio that buys stocks after confirming the end of a sequence of insider (top executive) purchases, and shorts stocks after confirming the end of a sequence of insider (top executive) sales earns month alphas of 1.71% (2.37%), or 22.6% (32.5%) annualized.

Wow, that is some serious “alpha.”

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.