We created this post as a resource for families and their advisors facing tough decisions regarding their ownership in their family business. Many folks approaching retirement are looking for options on how to achieve liquidity and diversification, along with tax-efficient ways to defer capital gains.

Note: A more extended post on 1042 qualified replacement property for ESOP rollovers is available here.

As we’ve learned, employee stock ownership plans (ESOP) are a good estate planning tool, and offer some intriguing ways to manage taxes.

We learned about ESOP strategies a few years ago, when we entered into a dialog with a family who, along with an ESOP, owned an interest in a large privately-owned company in the Philly area. The family was interested in reducing their concentrated ownership in the company and meeting their estate planning goals through a sale of stock to a company ESOP. But the family faced a problem: if they sold into the ESOP, a large tax bill loomed on the horizon.

Selling company stock to an ESOP creates a 1-time tax-deferral opportunity, as long as the cash generated from the sale is used to buy 1042 qualified replacement property. However, once the 1042 property is purchased, there is no looking back — if the investor sells any of the 1042 property they realize the deferred capital gain. For example, if an investor buys stock ABC, and 2 months later ABC receives a cash tender offer, the investor will realize a capital gain on the sell of ABC (the basis is equal to the basis on the stock sold to the ESOP). Or consider a frequently rebalanced portfolio, every time a transaction occurs, the 1042 tax-deferral opportunity is lost forever. For a tax-sensitive investor, the investment plan associated with the 1042 property is a critical decision point. Ideally, the investment option is 1) diversified, 2) low-cost, and 3) able to maximize the tax-deferral.

One problem: Investment solutions that solve #1, #2, and #3 are impossible to identify in the marketplace (as far as we could tell).

The current investment offerings for investors looking to roll ESOP funds into 1042 QRP are bleak and the primary service providers are banks and trust companies. We helped the family devise a better approach, which we outline in this piece so other independent advisors don’t need to reinvent the wheel.

So to summarize the key elements of the story:

- ESOPs are a great tool for businesses to provide liquidity for legacy owners and align firm incentives.

- ESOP rollover options into 1042 QRP stink and can be improved!

A potential solution: The Employee Stock Ownership Plan (ESOP)

We often run into individual investors who have a significant portion of their wealth tied up in a private business that they own or operate. While private companies are a great vehicle for creating wealth, things can get complicated when wealth becomes highly concentrated in the business, or in the context of succession planning. What these investors are looking for is a way to achieve some liquidity and diversification, without bringing in a new, unknown partner or facing risks related to other worrisome control issues. In an ideal world, a good solution would also help the business. Finally, if possible, owners would like to avoid painful tax consequences. An Employee Stock Ownership Plan (ESOP) is the answer.

ESOPs exploded in popularity a few decades ago, and today there are thousands of ESOPs in the US covering millions of employees. The success of the ESOP model may be due in large part because it is a win-win for employees and for business owners. If you’re a business owner, talk to your local lawyer for advice on creating an ESOP.

A Win for Employees

A fundamental aspect of the win-win situation is that ESOPs encourage employees to think like owners. As employees work for the business and help it grow, they acquire ownership, which creates incentives that drive a range of positive externalities.

Participation in an ESOP increases employees’ motivation and commitment to the business. It builds unity, loyalty and a cooperative culture, and reduces turnover and the “free rider” effect. Employees also get to vote their stock through the ESOP and thus have a say in the management of the business. If they do a good job and the business thrives, they will have a comfortable retirement, which directly affects their livelihoods and gives them a way to provide for their families. The varied benefits provided by employee ownership can have a huge long-run impact on company performance.

A Win for Business Owners

While employee ownership benefits the business and the employees themselves, another benefit of ESOPs is they can provide a source of liquidity and diversification for owners of the business, since owners can “cash out” by selling company stock to longtime, trusted employees via the ESOP.

This can be a big deal in a private company context, and the vast majority of ESOPs are associated with private businesses. Achieving liquidity in a private company can be a complex, difficult, risky and lengthy process. The process for selling to an ESOP, however, is much simpler: A third-party valuation firm prepares an appraisal for the ESOP shares, the ESOP announces a tender offer price, which cannot be more than the appraised value, and owners can elect to sell to the ESOP at that price.

ESOPs also have a compelling tax feature that enhances their attractiveness for sellers.

Exiting via the ESOP: The Section 1042 “Rollover” Election

Ordinarily, when an owner sells shares in a private business, there will be a taxable gain to the extent the sales price exceeds the tax basis in the shares sold. But with a sale to an ESOP there can be an alternative. For owners of C Corporations that have an ESOP, there is a remarkable tax deferral provision in Section 1042 of the Internal Revenue Code.

Section 1042 provides a way for sellers to sell stock to an ESOP and defer capital gains. There are a few basic conditions that must be satisfied to achieve this.

To qualify for 1042 treatment, the seller must have held the stock for at least 3 years, and the ESOP must hold > 30% of the outstanding stock of a private C corporation. Subsequent to the sale, the seller must file a Section 1042 election form with the IRS. Next, within 12 months of the sale, the seller must invest the sale proceeds in so-called Qualified Replacement Property (QRP).

Qualified Replacement Property

QRP is essentially defined as stocks, bonds or other debt instruments issued by U.S. domestic operating companies. There are also some passive investment income thresholds that disqualify some securities.

It is notable what does not qualify as QRP: mutual funds or exchange traded funds, foreign securities, certificates of deposit, REITs, MLPs, partnership interests, and local, state and federal government taxable or tax-free bonds.

Upon purchase of the QRP, these securities inherit the cost basis of the shares that were sold to the ESOP; the tax basis “rolls over” into the QRP. The gain that was deferred on the sale of stock to ESOP will be taxed when the QRP is sold. Finally, dividends from the QRP are taxed at dividend tax rates.

While there are obviously more details, these are the key features for 1042 and QRP. Now that we have some parameters laid out for the mechanics of 1042, what is a strategy we can use to invest in QRP?

Portfolio Selection

Wealth is built through concentrated holdings, but it is protected by diversification.

The purpose of our QRP portfolio is twofold: 1) assure current financial security, and 2) fund future opportunities. Our risk/return objective in this instance will be to match the performance of the S&P 500.

Our tax objective will be to optimize the 1042 deferral opportunity. Finally, our liquidity objective is to provide easy access to the capital in the portfolio, without adding unnecessary complexity or disrupting the strategy.

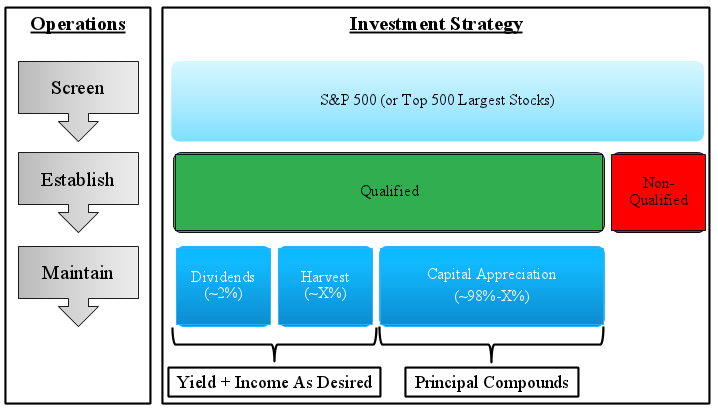

We think market-cap weighted indexing strategies are a solid option for a 1042 election and QRP re-investment.

We cannot invest in the entire S&P 500 due to passive income and certain other restrictions. Yet when we screen the stock universe for non-QRP features, we find that only about 20% of S&P 500 constituent securities do not qualify for 1042 treatment.

So while we cannot perfectly reproduce the S&P 500, we can get close. Also, similar to the construction of the S&P 500 index we can “market-cap weight” our portfolio so that it matches the composition of the index.

The S&P 500 index has modest turnover, so we can minimize the tax effects associated with trying to match a more active, high-turnover index.

Still, there may be certain corporate actions that may result in taxable events that can affect our QRP portfolio. These might include mergers and acquisitions, spinoffs, and so forth.

Additionally, our market weight construction is “self-rebalancing.” When the market value of a stock increases, its weighting in the S&P 500 increases; if the market value of stock falls, its weighting in the S&P 500 also falls. Thus, due to low turnover of the index and value weighting of the portfolio, our QRP returns over time should track the performance of the S&P 500 index quite closely. Plus, there is limited “tax drag” because the strategy is essentially “buy and hold forever” to maximize the value of the tax-deferral.

The Dividends and Yield Harvesting Option

Today, the current yield on the S&P 500 stands at approximately 2.0%. In addition to this yield, 1042 Rollover investors can elect to enhance it via a dividend “harvest” at any time.

It works like this. Let’s say a 1042 Rollover investor needs to access some additional capital beyond the 2% yield offered by QRP. Let’s say they want to purchase a new car, but only a 3% yield would satisfy this incremental liquidity need.

The advisor can sell 1% of the portfolio, but this is spread out across the portfolio on a pro-rata basis. So the investor will be selling only a few shares of the smallest QRP positions, but many shares of the largest QRP positions. This way, the market-cap-weight allocations within our S&P index have not changed in relation to each other — instead the overall portfolio is merely 1% smaller. In addition, since these sales are taxed at long-term gains rates, they are similar (at the highest marginal brackets) to dividend tax rates. Put another way, we have created a “synthetic” additional 1% yield through “smart” harvesting. Once again, this is facilitated by algorithmic trading. When these transactions are done in trust structures, one needs to be careful to stay in line with the rules related to the “power to adjust.”

An example of developing a low-cost uber-tax-efficient 1042 QRP qualified investment option is below:

Conclusion

1042 rollover investment strategies don’t have to suck. And as far as we can tell, nobody offers a 1042-qualified, low-cost, and tax-efficient solution for investors looking to maximize the benefit of their deferral opportunity. We’ve done these transactions for several family office clients with great success. The biggest hurdle is realizing that the solutions offered by banks and trust companies are not ideal for families looking to access a low-cost, tax-efficient, and totally transparent ESOP 1042 qualified-replacement-property investment strategy. We think independent advisors should consider tracking down clients that have an ability to sell into an ESOP and encourage them to take advantage of a 1042 rollover and use the proceeds to buy a 1042-compliant “passive” solution. You can use our proposed solution or contact us if you want to collaborate on building a win-win solution. We have the technology to facilitate custom solutions that can be tailored to suit individual circumstances.

About the Author: David Foulke

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.