I’m a huge fan of hard-core academics that produce incredible research, and yet, very few are familiar with their research. I call these folks, “undiscovered gems.”

One might ask why undiscovered gems exist. On one hand, if a researcher produces incredible research, they should be widely recognized. However, this logical construct relies on an assumption: good researchers are good at sharing their work beyond their niche peer group in the ivory tower.

Bad assumption.

At Alpha Architect we try and fix this situation. We consistently read research and share it with our large community, which extends well beyond the readership of esoteric top-tier academic finance journals.

In this post we highlight research from one of my favorite researchers, Victor DeMiguel.

Source: http://faculty.london.edu/avmiguel/

Professor DeMiguel, is relatively unknown among the practitioner community, and even among finance departments.(1) In fact, I had never heard his name until I stumbled across his website 5 or 6 years ago. Turns out Victor isn’t a finance professor — he’s a management science and operations professor!

Of course, asset allocation is really less of a finance problem and more of an optimization problem. So it makes sense that someone outside of pure finance would write some really interesting papers.

Anyway, I am indebted to Prof. DeMiguel and I have learned an incredible amount on tactical asset allocation from reading his work. We have discussed his incredible paper (alongside his co-authors Lorenzo Garlappi and Raman Uppal who are great researchers as well!) that highlights the incredible robustness associated with dead simple equal-weight, “1/N,” portfolios.

Perhaps his greatest learning device isn’t a paper, but a presentation he has on the history of asset allocation research and the avenues for the research vein in the future.

Here is the link to the presentation, which starts with a great introduction slide (pictured below)

Source: ppt deck

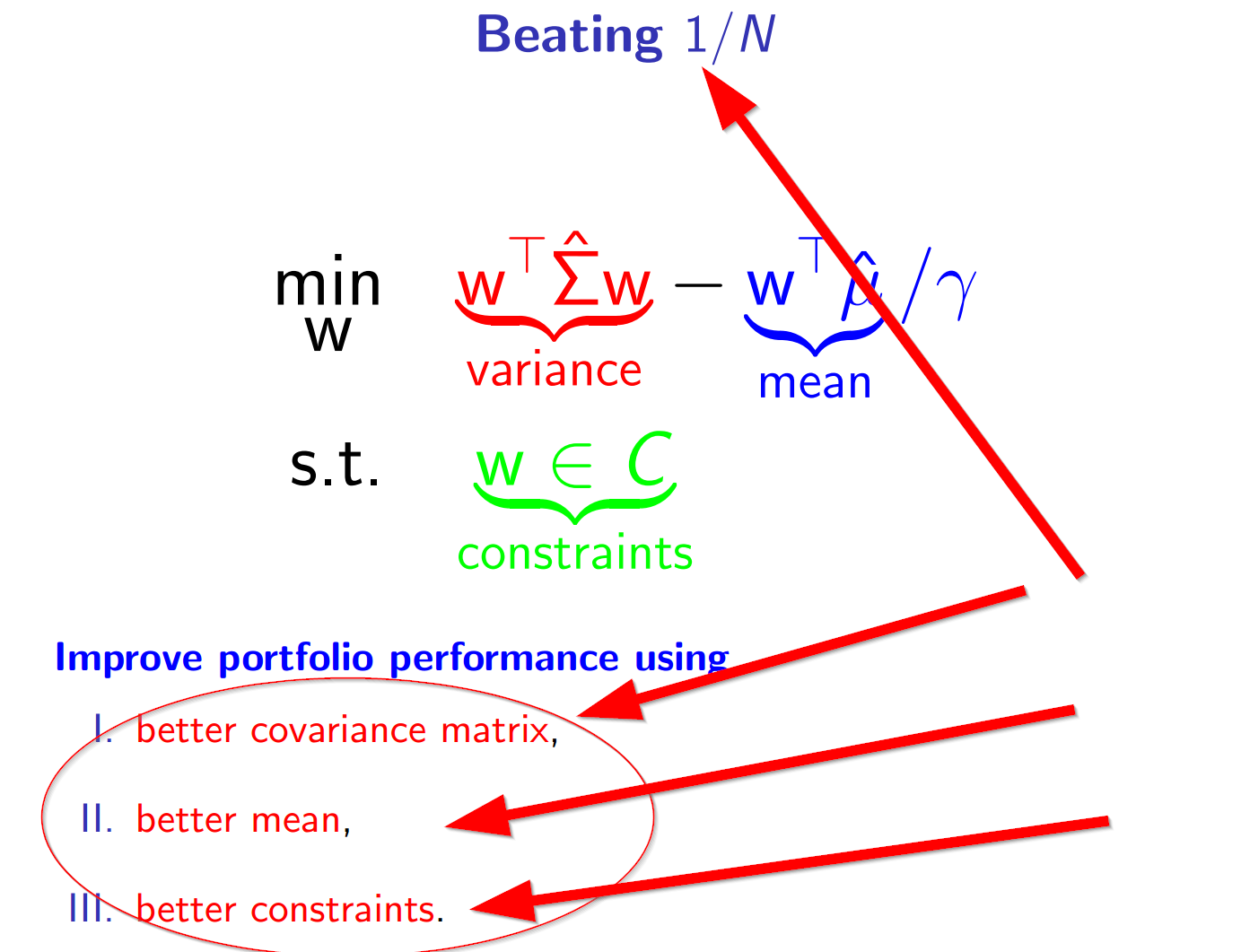

I highly recommend all readers spend some time on the presentation. Particularly towards the end. There is a discussion of various issues in portfolio optimization and the quest to beat the infamous “1/N” portfolio:

- Estimate a better covariance matrix

- Estimate a better expected returns

- Identify better constraints

So far all the whiz bang research doesn’t seem to provide crystal clear evidence that 1/N can be beat. In fact, we still recommend that investors beware of geeks bearing formulas and focus on simple trend-following rules if they choose to extend beyond 1/N. One idea that might be promising is robust estimation — see here.

Go forth and learn new things!

Note, Victor’s coauthors are also awesome. For example, here is a similar presentation from Raman Uppal on asset allocation.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.