U.S. stocks have delivered incredible stock market returns for a long time: the average compounded total return on the U.S. stock market has been nearly 10 percent per year from 1927 through 2016 (Using data from Ken French’s website on the market-capitalization weighted CRSP index).

Doesn’t sound impressive?

Consider the fact that a $100 invested for 90 years at 10 percent would compound to over $530,000. Perhaps this is why my two favorite investors of all time suggest that savers stash the bulk of their cash in the US stock market:

First, Warren Buffet’s advice:

Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard’s.)

Next, Jack Bogle’s advice:

I wouldn’t invest outside the U.S. If someone wants to invest 20 percent or less of their portfolio outside the U.S., that’s fine. I wouldn’t do it, but if you want to, that’s fine.

When great minds speak, we should listen, but we should also ask a critical question: Are Warren and Jack making this recommendation based on evidence? Or are they basing this recommendation on their experience as long-time US equity market investors?

In this short essay, I explore the idea that Buffett and Bogle’s advice should be digested with a healthy dose of skepticism. To make this point, I highlight several recent research articles that suggest US stock returns are exceptional relative to all other stock markets across time. The US stock market is an anomaly and perhaps the ubiquitous disclaimer, “Past performance may not indicate future performance,” is an important consideration with respect to the expected performance of the US stock market over the next century.

What is the Equity Premium Puzzle?

The exceptional performance of the US stock market has been deemed the, “The equity premium puzzle,” by academic researchers and was first discussed in an influential academic paper by Rajnish Mehra and Edward Prescott in 1985.

Here is a quote from the original paper:

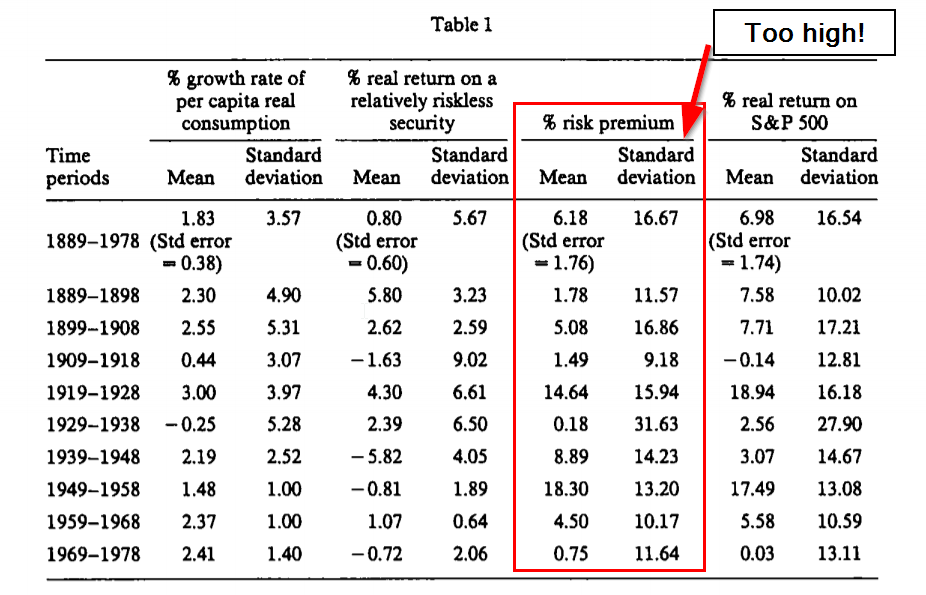

Restrictions that a class of general equilibrium models place upon the average returns of equity and Treasury bills are found to be strongly violated by the U.S. data in the 1889-1978 period…

The authors find that stocks beat bonds by an average of 6% a year, which is simply too high to be justified by any equilibrium model in existence at the time. Here is the key table that outlined the real risk premium for US stocks:

How Academics Tackled the Equity Premium Puzzle

Academics struggled to build theoretical models that would predict such a high return for the U.S. stock market. Despite significant efforts, the research community never seemed to form a general consensus that the equity premium puzzle would be solved.

Nonetheless, one of two solutions was explored in an effort to answer the puzzle:

- Approach #1: Build elaborate models that predict why the expected US equity premium is justifiably high.

- Approach #2: Refute the premise that the historical US equity premium is a valid estimate: perhaps high past US stock market returns simply reflected a lucky run?

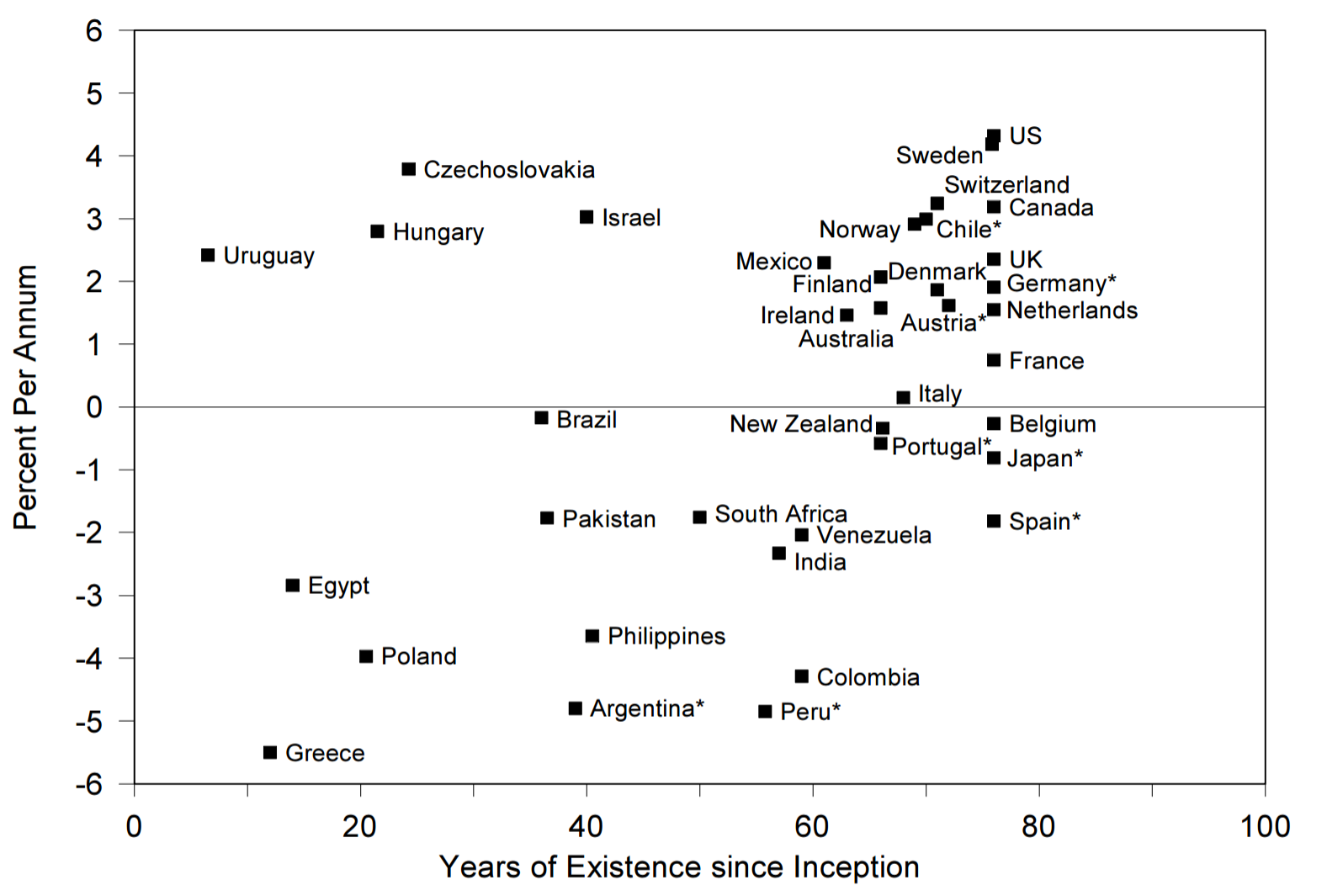

Researchers continue to explore solution #1, but there seems to be no clear answer in sight. Other academics have explored option #2, by collecting more data on various stock markets across different points in time. Philippe Jorion and William N. Goetzmann provide a good example of this research in their paper, “Global Stock Markets in the Twentieth Century.” The authors examine 39 global stock markets from 1921 through 1996 and, as before, saw evidence of the outperformance of the U.S. stock market, which provided a real return (i.e., adjusted for inflation) of 4.32% over the period, the highest of all countries (the median performance was 0.80% for the other countries). But the US stock market’s strong performance was old news and not the point of their story. Their key insight was identifying a clear survivor bias in the data: The longer a country’s stock market existed, the higher the annual return.

This relationship is best captured in Figure 1 from their original paper:

In short, the returns of the winners depend on their past survival. If investors can predict with perfect foresight which countries will survive and which countries will die, using the past results might be meaningful. However, is it realistic that investors have the ability to know future winners? Unlikely.

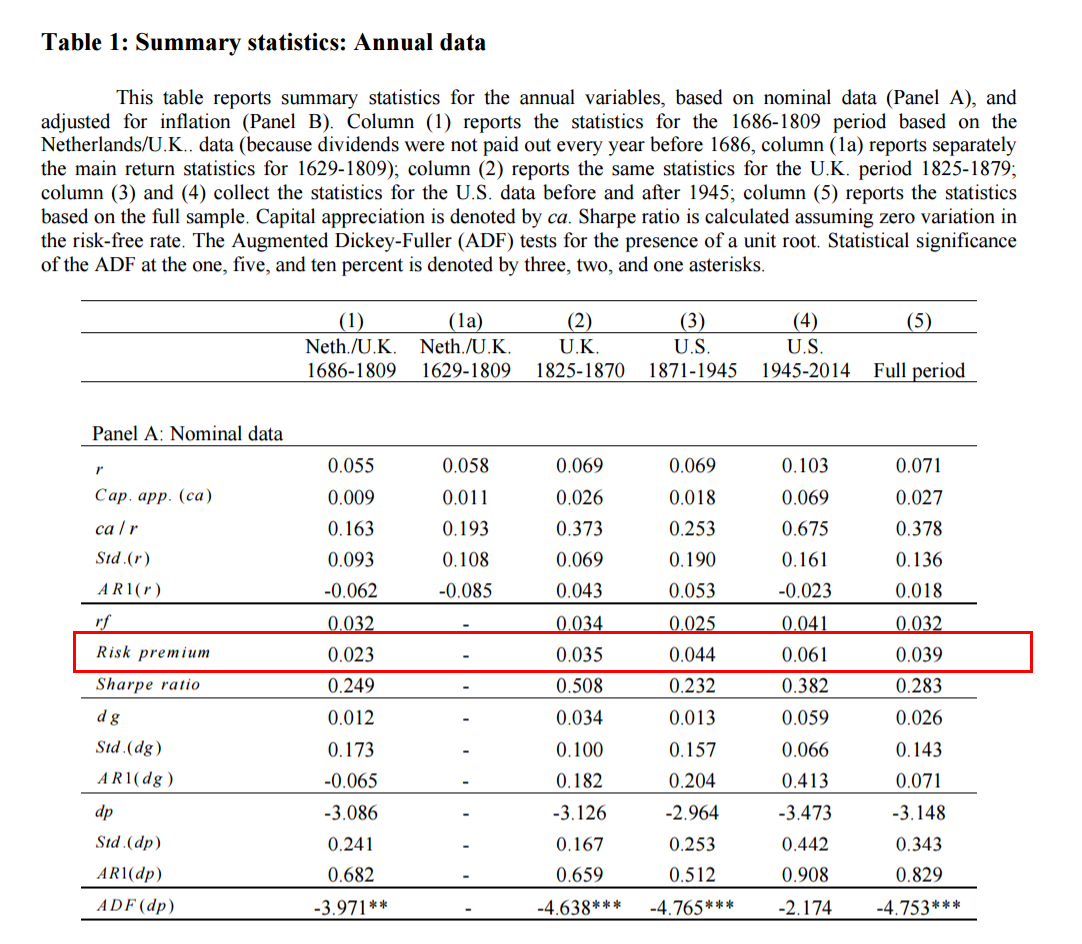

To make matters worse for those who have been conditioned to believe the US stock market experience is “normal,” a new paper by Notre Dame professor Benjamin Golez and Stanford professor Peter Koudijs, titled, “Four Centuries of Return Predictability,” performs a similar “out of sample” study as Jorion and Goetzmann. In their research the authors look at data from the Netherlands and the UK from 1629 to 1812, the UK market from 1813 to 1870, and US stock markets from 1871 to 2015. They estimate that the equity risk premium, or the spread in average returns between stocks and bonds, are around 2.3% to 3.5% for the Netherlands and the UK in the earlier time periods and around 6% for the US market.

So the US experienced an equity risk premium that was 2-3x that of other markets. Wow.

Will High US Equity Premium Continue into the Future?

On one hand, perhaps the US stock market will continue to defy market expectations and generate high realized returns in the future. However, on the other hand, investors may be wise to acknowledge the incredible amount of potential luck the US has experienced. Perhaps Jack Bogel, who ironically suggests a huge overweight position to US equities, makes the best case that we should think twice about this recommendation.

Consider a PBS interview with Jack Bogle where he states the following:

Good markets turn to bad markets, bad markets turn to good markets. So the system is almost rigged against human psychology that says if something has done well in the past, it will do well in the future. That is not true. And it’s categorically false. And the high likelihood is when you get to somebody at his peak, he’s about to go down to the valley. The last shall be first and the first shall be last.

As Bogle points out, it may be precisely the past winners who are about to fail.

Famed Wharton professor Jeremy Siegel has a related statement in his paper, “The Equity Premium: Stock and Bond Returns since 1802”:

Certainly investors in…1872…did not universally expect the United States to become the greatest economic power in the next century. This was not the case in many other countries. What if one had owned stock in Japanese or German firms before World War II? Or consider Argentina, which, at the turn of the century, was one of the great economic powers.

It’s probably likely that Argentinian investors predicted continued economic dominance at the turn of the century. They were wrong. Perhaps US investors are suffering from a similar level of hindsight bias? Can we determine with certainty that the U.S. will be a superpower 100 years from now? We should consider the fact that when we look at past U.S. returns, we are looking at a market that did not fail, but does it follow that it cannot fail in the future?

Conditioning on past returns can subject investors to form misguided expectations about the future (a reasonable premise since investors are often irrational). US investors should avoid their innate biases and take advantage of diversification — spread stock market bets around the globe — not just in US stocks. A concentrated bet on the US stock market is exactly that — a concentrated bet. And at current relative market valuations — the US stock market sells at a P/E of 21, developed markets sell at a P/E of 18, and emerging markets trade at a P/E of around 13 — hitting 10% annualized returns over the next 100 years via US stocks will be challenging and investors should plan accordingly.

(1)About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.