Each year I teach my “seminar in investments” course at Drexel, which consists of the Masters in Finance students and a handful of geeky MBA students.

The first few weeks of the course involve an introduction to various investment frameworks and how to navigate the source academic literature.

The rest of the course is dedicated to research. Yeah, baby!

I divide the class into research groups of 5-6 people and they are required to conduct several research projects over the 10 week course.

This year there were a handful of great research projects conducted. A lot of the research projects are associated with factor investing and most of the groups highlighted things we already understood: momentum works, value works, trend-following works, etc.

However, one group went the extra mile and did an extensive investigation of the Fama and French 5-factor model using out of sample data from the Chinese A-share market. (To learn more about factor models, you can read our long-form piece on the subject).

The data in their study included all A-shares from 1995 to 2014 and excluded financial firms, negative book-to-market ratio firms, firms with less than 5 years of return data, and any firm missing the necessary information to calculate the required metrics to calculate the variables: size, book-to-market, beta, profitability, and asset growth. Some caveats are that the data time period is short and the Chinese A-shares market is extremely volatile — arguably hard to identify much signal from all the noise.

The 5-Factor Model in the Chinese Market

The students started with a highlight of what was discovered in Fama and French (2015):

- Profitability and investment help explain the cross-section of US stock returns.

- HML becomes redundant when profitability and investment factors are included in their 5-factor model.

Fama and French (2015) is a pretty extensive study with a handful of robustness tests. However, other authors have identified that the Fama and French 5-factor model may not be as robust as originally contemplated. For example, here is a discussion by Hou, Xue, and Zhang and Asness also has a discussion in his piece here.(1)

My students were able to take another angle on the debate by looking at out of sample data from Chinese A-shares.

Here is what my students found:

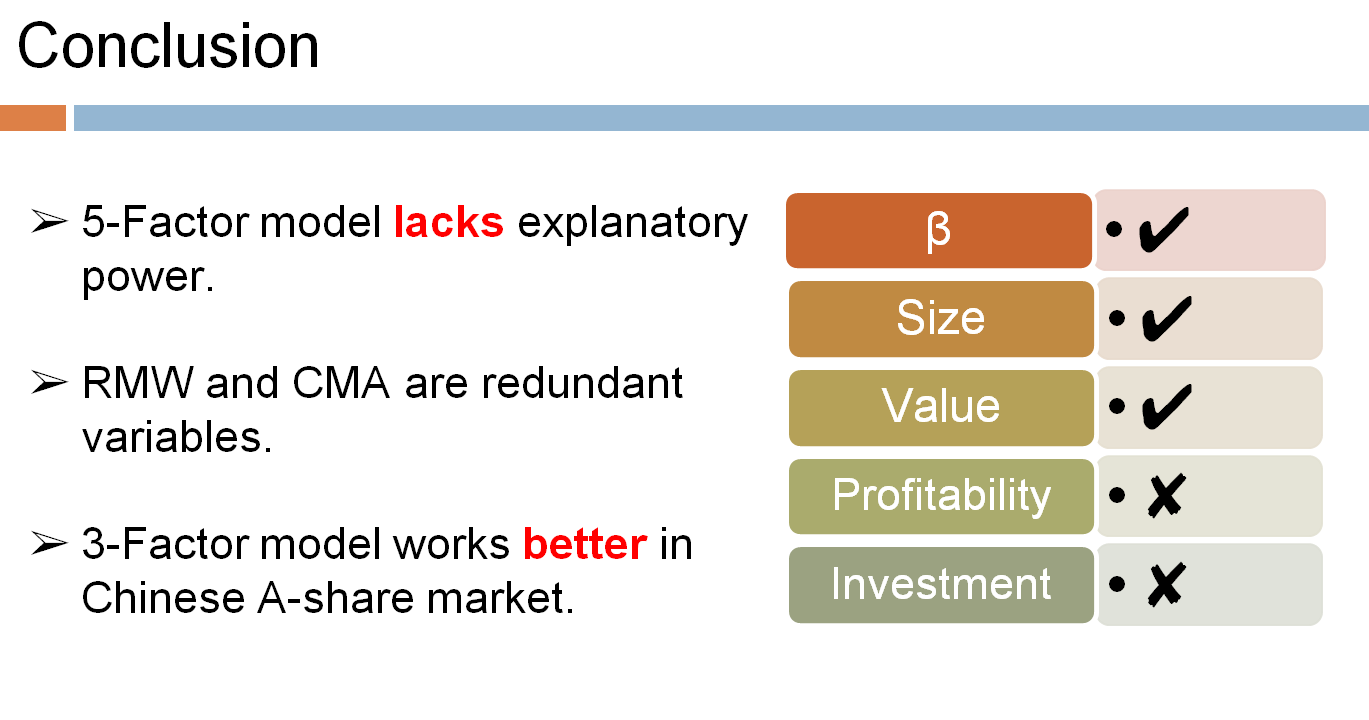

- The original 3-factor Fama French model works well in the Chinese A-share market.

- HML matters. A lot.

- Profitability and investment (RMW & CMA) becomes redundant when the value factor (HML) is included in the asset pricing model. (opposite of the results in the US market)

Long story short, based on the evidence from the Chinese A-share market, the Fama and French 3-factor model (beta, size, and value) still gets the job done and the 5-factor model lacks robustness.

Here is the final slide from my student’s presentation:

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.