U.S. Companies bought back $217 Billion of their $1.3bn in overseas cash in the first quarter helping fuel a record $189 billion in stock buybacks. More are expected throughout the year. Even Warren Buffett is getting deeper into the game. Has this demand pushed up stock prices, perhaps for the benefit of management over long-term shareholders who would have preferred reinvestment?

I will argue “no,” at least in theory. I will also show the evidence that I could be wrong. My larger point is that despite this tension, theory and contradictory evidence can co-exist and can still reveal truths. For stock buybacks, this truth includes their effect on common measurements of valuation, themselves simplified models of reality. Those investors who stay humble yet curious, skeptical and adaptable, can thus stay unperturbed by all the recent rhetoric around stock buybacks.

The Basics of Stock Buyback in Theory

I will start by illustrating that buybacks by themselves don’t theoretically change the value of firms. This insight on the irrelevance of the capital structure to a firm’s value was behind the Nobel Prize in Economics awards given to both Franco Modigliani and Merton Miller. It is known as the Modigliani-Miller theorem.

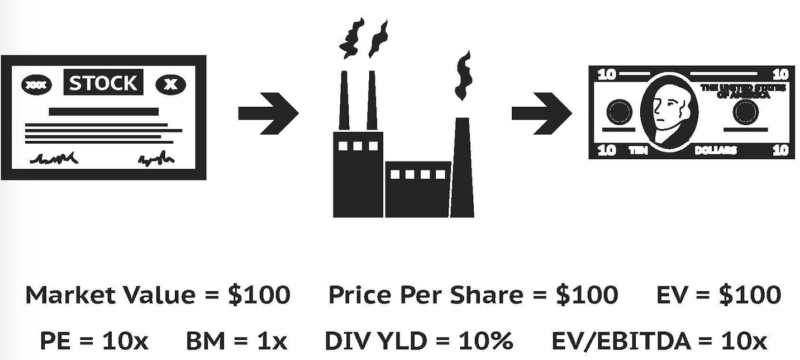

As is true when building any model, I need to start by simplifying my world and do so by making some very unrealistic assumptions: zero interest rates for both cash and borrowing rates, no taxes or transactions costs and perfect price inelasticity (i.e., prices and thus profits won’t change with supply). In my fantasy world, I have one company with one factory that issues one share of stock that the market values at $100. This fantasy firm generates an expected $10 in profits annually which it pays out as dividends and is expected to do so into perpetuity. If that’s not enough, its factory never depreciates.

The capital structure picture: one share of stock worth $100 which owns one company with one factory which entitles the shareholder to receive $10 into perpetuity.

Simple One Share Co

The resulting valuations measures:

- The Price-to-Earnings ratio (or price per share/earnings per share referred to as PE) = $100/$10 or 10X.

- The Book-to-Market Value (or book value/market value referred to as BM) = $100/$100 or 1X.

- The Dividend Yield (or dividend per share/price per share referred to as Div Yld) = $10/$100 or 10%. Because in our case all earnings are paid out as dividends and last into perpetuity, this is also our discount rate.

- The Total Enterprise Value (or Market Value plus Debt minus Cash referred to as EV) to Cash Flow (or Earnings before Interest, Taxes, Depreciation and Amortization referred to as EBITDA), the resulting ratio referred to as EV/EBITDA = $100/$10 since we assumed away the ITDA or 10X.

Now, let’s view the impact of playing with the capital structure of our fantasy firm. First, let’s issue another share and sit on the cash (i.e., do the opposite of a stock buyback).

Simple 2 Share Co with Cash

Note that the PE ratio goes from 10X to 20X and the dividend yield drops from 10% to 5%. Did the firm just get “richer” in value by the financial “manipulation”? Of course not. A single share is still worth $100, but it now reflects ownership in a less leveraged (i.e., less risky) combination of cash along with the factory. At this point, if the company bought back its share with the cash, you’d be back where you started. Stock buybacks, in other words, do not affect the price of a share, at least theoretically.

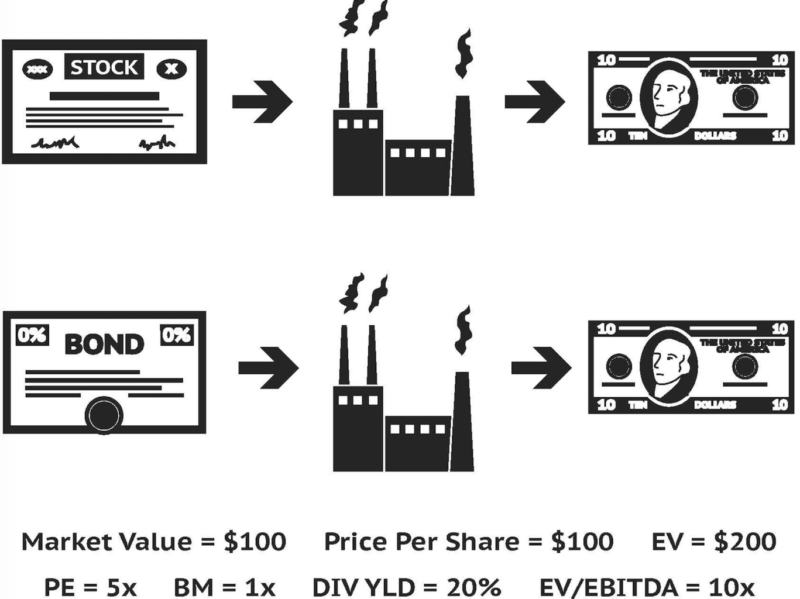

Stock buybacks, because they affect leverage, do affect most measurements of value. In this last example, we will now issue a bond to fund another factory. Note the changes in valuations now.

Simple Leveraged Co.

Increased leverage by issuing bonds, like stock buybacks that use cash, makes firms look cheaper using valuation measurements like a PE ratio or dividend yield. However, rather than expressing true cheapness, this lower valuation instead reflects the increased riskiness of each share due to the debt issuance. If each factory’s value collapsed by half and the firm was liquidated, the stockholder would be wiped out as the remaining $100 in value would be used to pay off the bond. Investors rightfully demand a higher risk premium, and thus apply a higher discount rate, when valuing the firm.

To conclude: in theory, buybacks have no effect on the valuation of a stock’s price, but will change its PE ratio and dividend yield to reflect the changes in leverage and risk. Book value and enterprise value, on the other hand, aren’t concerned with leverage so maintain their valuation measures.

The Reality of Stock Buybacks

The realities of stock buybacks are not so straightforward.

If our fantasy firm that just issued a share resulting in $100 in cash turned around and immediately paid back the cash as a dividend, the 2 shares would drop in value by the $50 each shareholder just received. Stocks drop like this when they go “ex-dividend” in real life, too. Opting for a share buyback doesn’t raise the price but it does avoid a drop in the stock price associated with a dividend payment. If managements’ compensation depended on poorly written contracts that paid off based on share price instead of returns, shareholders would be right to fear managers using buybacks to boost their compensation.

Evidence implies another hole in the theory: Most shares actually jump when a firm announces a buyback (1). Why? Without going into the full literature, the most common explanation is that managers use buybacks to signal to their shareholders they both view their stock is cheap and they won’t waste their cash on less profitable investments. They can’t find any more factories, in other words, and trust that their shareholders can find better investments for their cash. There is equally deep literature showing that the acquiring company’s stock typically falls and stay down after takeover announcements, so this positive reaction by investors seems valid.(2)

Share buybacks also provide for more flexibility than dividends. If the shareholder can’t find an alternative investment, she doesn’t need to sell. She may also want to avoid a capital gain. This option to avoid taxes doesn’t exist with dividends. Managers often prefer the greater flexibility of stock buybacks relative to dividends, too. Stocks that cut their dividends typically experience a significant price drop, so managers do everything they can to avoid a dividend cut. In fact, managers take pride in gradually increasing their dividends over time.

As we have seen, stock buybacks also increase earnings per share and thus, without a corresponding increase in price, will make companies look cheaper by measurements like PE ratios and dividend yields. Maybe managers are hoping their shareholders are too dim to realize the extra risk the new leverage from stock buybacks creates. This is more or less the theory behind the alarm that by “inflating the value of the stock” a stock buyback “benefits corporate executives”, to quote Senate Minority Leader Chuck Schumer.

And in fact, to the dismay of proponents of the efficient market theory, people like Chuck might be right. Benefits from stock buybacks appear to persist as first reported by Lakonishok and Vermaelen in 1990 and more impressively, out of sample 15 years later as studied by Standard and Poor’s.(3) Sadly, it hasn’t proven so useful recently as witnessed by the relative performance of the SPDR S&P 500 Buyback Index ETF (which makes suspect the argument that buybacks are fueling the latest leg of this rally).

Source: Bloomberg, LP

Stock Buyback Implications and Valuation Realities

Although it’s unclear whether shareholders are systematically fooled into accepting a PE ratio or dividend yield unadjusted for leverage, leverage still matters. But even when adjusted for leverage properly, because accounting is only a model of a firm’s profitability and value, it too is flawed. To mention just a few shortfalls associated with our valuation measurements:

- Dividend Yield: As we just discussed, many firms may prefer to reinvest their earnings or return them to shareholders via stock buybacks and thus purposely keep their dividend low. As Meb Faber of Cambria finds in his whitepaper, “Do You Pay Taxes? Then Avoid Dividends and Do this Instead”, there are also plenty of more tax efficient means to access inexpensively valued companies.

- Price-to-Earnings (PE) ratio: Likewise, many firms may at any time be experiencing a cyclical drop in earnings leading to a high PE ratio, but still be considered having a compelling value by other measurements. This leads to large shifts in sector weightings. Corey Hoffstein of NewFound Research highlights the sector bets inherent in most value strategies as does Nicolas Ravener of FactorResearch when he extends and expands the valuation measurement horse race Wes Gray and Jack Vogel first ran on these pages. Other research by Feng Gu and Baruch Lev argues that earnings are now so irrelevant that even knowing earnings in advance offers little benefit.

- Book-to-Market: Optimally a less distortive way of measuring value and a favorite of academics (even though their standard value factor measurement—HML—has some serious flaws as pointed out by our friends at AQR). Travis Fairchild of O’Shaughnessy Asset Management, for instance, shows that reported book values do a poor job of valuing intangible assets and correctly depreciating long-term assets. In other words, reported book value should equal the net assets (or residual claim of a firm left to the shareholders) and thus its market value, but in practice, it can miss by a mile.

- Enterprise Value over Cash Flow: Although a favorite among private equity participants and the winner of Wes’s and Jack’s previously mentioned measurement horserace, it doesn’t even try to measure the “residual claim” of a firm’s assets, the very definition of a share of stock. Instead, it measures a firm’s cash making potential in relationship to the overall cost of taking full control of the firm. A buyer like a private equity firm can optimize the capital structure in relationship to real-world items like interest rate costs, capital expenditures and taxes later, all components that we assumed to be zero. Still, Charlie Munger of Berkshire didn’t call reported cashflow “bullshit earnings” for nothing; as Jason Zweig of the Wall Street Journal recently reported, this number can also be easily manipulated.

The Larger Lesson on Why Investors Should Care

As tempting as it may be for an investor to throw up their hands in disgust, the larger lesson for both the conflict between theory and evidence in regard to stock buybacks and the shortcomings of various accounting valuation measurements is to gain perspective.

By definition, theories and models only look to simplify our world so we can better understand it. They aren’t designed to always work but rather better help us to discern all the data, correlations and gut feelings that we are otherwise bombarded with. This isn’t a new insight. As Aristotle said, “about some things, it is not possible to make a universal statement which shall be correct.” But even if our theory is that “all swans are white” proves wrong when a black swan arrives, we shouldn’t assume there is a pink swan on its way.

Similarly, just because we see patterns doesn’t imply they will persist. There once was strong evidence that when old NFL Super Bowl teams win, stock markets would go up, but that doesn’t make for a worthy model. Correlation doesn’t prove causation. But as Michael Nielsen of Y Combinator observed, “If it doesn’t imply causation, then what does?”

Correlations, in other words, should be explored. If shown to hold up out of sample and across environments, correlations can even be acted on. Cliff Asness of AQR, a firm built around the ability to earn excess risk-adjusted return by employing factors like momentum, was a teacher’s assistant to efficient markets guru Gene Fama. The evidence at the time of his dissertation was enough for him, and he went off to employ the strategy at Goldman Sachs. Fama, an unapologetic donner of the University of Chicago T-shirt “That’s all well and good in practice…but how does it work in theory”, waited. He didn’t want to open the barn gate to every anomaly into his model, especially one built on a behaviorist theory. Yet even he has “reluctantly” included Momentum as a sixth factor in his asset pricing model.

We stay curious and skeptical but eventually adaptable.

In the case of the theory of the capital structure of firms, stock buybacks by themselves shouldn’t affect the value of shares. The lack of consistent supporting evidence may simply imply the theory is incomplete instead of wrongheaded. As reported by Asness and his team at AQR, there is also little evidence we should be worried that shareholders are getting hoodwinked or firms are under-investing. In short, we stay unperturbed by all the rhetoric void of either sound theory or evidence, but we remain always curious and adaptable.

References[+]

| ↑1 | Bhattacharya , Utpal and Jacobsen, Stacey E., The Share Repurchase Announcement Puzzle: Theory and Evidence (April 20, 2015). Review of Finance, Forthcoming; Kelley School of Business Research Paper No. 2014-45. Available at SSRN: https://ssrn.com/abstract=250049 |

|---|---|

| ↑2 | Here is a link to a ton of academic research on corporate governance. |

| ↑3 | Ikenberry, D., J.

Lakonishok, and T. Vermaelen. 1995. Market under reaction to open market share repurchases. Journal of Financial Economics 39: 181–208. |

About the Author: Jonathan Seed

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.