A year ago, I traveled to Dallas and warned a group of advisors that the U.S. stock market looked like it was running out of steam. Valuations were stretched, the top ten companies made up over a third of the market and small caps had been lagging for years. It felt like the market’s strength was concentrated in fewer and fewer names. Things looked pretty frothy out there!

Of course, that didn’t happen.

Instead of cooling off, large caps surged. Investor enthusiasm only grew stronger and valuations kept climbing. The market’s biggest names, already dominant, became even more dominant. Index concentration rose to levels not seen in more than a century.

So what happened? Was I wrong in my thinking, or are we simply witnessing a delayed reckoning?

In this blog post, I wanted to examine the market’s current concentration and valuation to better understand return expectations going forward. But reader beware; this isn’t some bold macro prediction to scare you away from sensible investing. It’s a reminder that markets move in cycles, valuations eventually matter, and history has a way of humbling even the most confident forecasts.

Before starting, two things:

First, if you’d rather watch the video version of this blog, make sure to check our latest mini-doc on our YouTube channel. While you’re there, make sure to subscribe for more content like this!

Second, many of these ideas came from my interview with Meb Faber, founder and CIO at Cambria. I wanted to thank Meb for sharing his thoughts with us, and to give credit where credit is due.

Let’s begin.

The Valuation Reality Check

We’ll start with a simple question as we seek to uncover what the future might hold: Can valuations tell us something anything about future returns?

Historically, valuations have been a useful (though not perfect) indicator of real returns over the following decade. Below, you’ll see historical CAPE1 readings (in black) for the U.S. market alongside their corresponding forward ten-year real returns (in green). The conclusion is straightforward: when valuations are low, future returns tend to be above average; when valuations are high, forward returns tend to be much more muted.

Right now, the U.S. market sits at a CAPE ratio of around 40. That number doesn’t just sound high, but nearly double the long-term average of roughly 20, and the second most expensive in history!

Here’s the problem: historically, when valuations have climbed to this level, the following decade hasn’t been kind to investors. Not once has a country that ended a year with a CAPE above 40 produced positive real returns over the next ten years.

That’s not a personal opinion but what the data shows.

This raises the natural question: What does that imply for the road ahead?

To get a sense of what current valuations might mean going forward, I ran a linear regression using historical CAPE data and forward ten-year real returns. The relationship is remarkably consistent: as valuations rise, future returns fall. At today’s valuation levels, the regression suggests an expected real return of -2.46% for the next decade. From a historical perspective, the last time we were at the CAPE reading we find ourselves in today, the market went on to lose -2.11% per year for the next ten years. Of course, I must reiterate that these are models, and likely won’t 100% accurate; but these outputs should at least make us pause and think…

Could it turn out better?

Of course. Markets can stay expensive longer than anyone expects (just look at the past year!) But when you’re paying record multiples for future earnings, you’re leaving yourself very little margin for error.

A Market of Stocks or a Few Stocks for the Market?

Valuation isn’t the only red flag flashing.

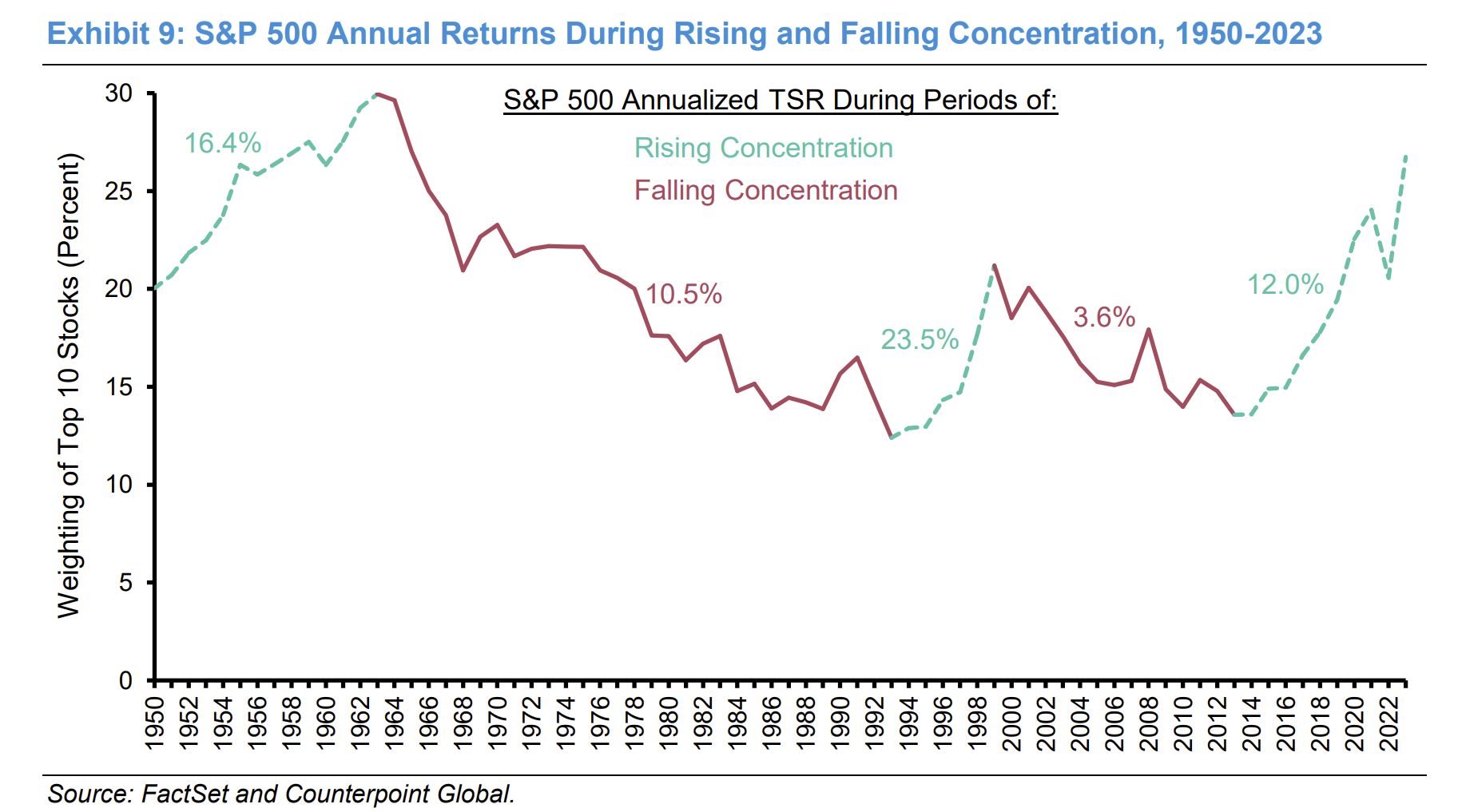

Today, about 40% of the market is concentrated in its 10 largest companies. This is the most concentrated the market has ever been.2

But what does this mean for the market going forward?

In their paper, Stock Market Concentration: How Much is Too Much? Michael Mauboussin3 and Dan Callahan point out that concentration itself isn’t a bearish sign. What really matters is how concentration changes going forward. Rising concentration tends to coincide with strong market performance as leading firms continue to gain share and deliver growth. On the other hand, when concentration starts to fall, this means your largest players are underperfoming the rest of your portfolio, and that’s when returns have historically suffered.

If the biggest names continue to pull away from the pack, the market could remain strong for a while. But if that leadership falters, history suggests the unwind can be painful.

What Can Investors Do About It?

Of course, this all may seem like doom and gloom, and you might be thinking that it’s time to sell your stocks and hide somewhere else.

This would be the wrong take-away.

Timing the market using valuation is a finicky proposition at best. But if you can’t predict when valuations will normalize or when concentration will unwind, what can you actually do?

First, remember that extremes eventually correct, but they don’t do it on a schedule. The goal isn’t to time the peak, but to tilt the odds back in your favor.

A few evidence-based approaches can help:

- Diversify across geographies. Many foreign and emerging markets trade at far lower valuations than the U.S. Historically, starting cheap has mattered.

- Tilt toward value and smaller companies. After years of underperformance, small-cap and value stocks now sit at some of the largest valuation spreads in decades relative to large growth stocks.

- Consider rules-based risk management. Systematic approaches, such as trend following, can help manage downside risk when markets begin to reprice.

A Season for Everything

As Meb said during our interview: “there’s a season for every market.” Today’s season is one of high expectations and high prices, but there will likely come a time where fundamentals matter again. Hopefully soon enough!

Investors can’t control valuations or sentiment, but they can control process, discipline, and diversification. Those tools don’t guarantee outcomes, but they do seek to improve the odds when the next season finally comes.

- The cyclically adjusted price-to-earnings or CAPE is a valuation metric that can be used on the market as a whole. The main differentiator from an ordinary PE ratio is that it smooths earnings to account for the booms and busts in the economy. ↩︎

- Just from last year, we surpassed the previous all time highs in concentration: 38%, set back in the 1900’s. ↩︎

- Mauboussin, Michael J., Callahan, Dan, Stock Market Concentration How Much Is Too Much? (June 4 2024). Morgan Stanley Investment Management, Counterpoint Global Insights. ↩︎

About the Author: Jose Ordonez

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.