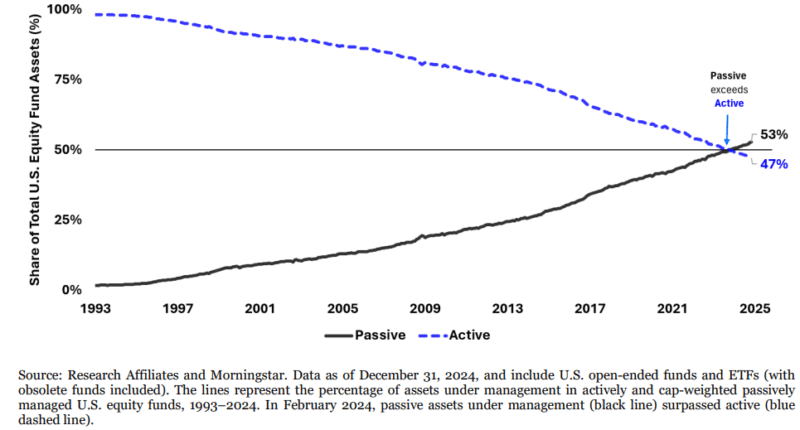

Fueled by the persistent failure of active management (as evidenced, for example, by the annual SPIVA scorecards), passive investing now commands the majority of assets under management.

This structural shift is not without consequence. Chris Brightman and Campbell Harvey’s May 2025 paper “Passive Aggressive: The Risks of Passive Investing Dominance,” along with recent academic and industry research, highlights several critical risks and unintended market distortions emerging from the dominance of passive strategies.

Key Findings on Passive Investing Risks

- Erosion of Diversification

As passive funds grow, stocks within major indices increasingly move together, undermining the diversification that index investing was designed to provide. This rising correlation means that sector and business-model differences matter less for portfolio risk, exposing investors to larger market swings. - Structural Divergence in Market Responsiveness

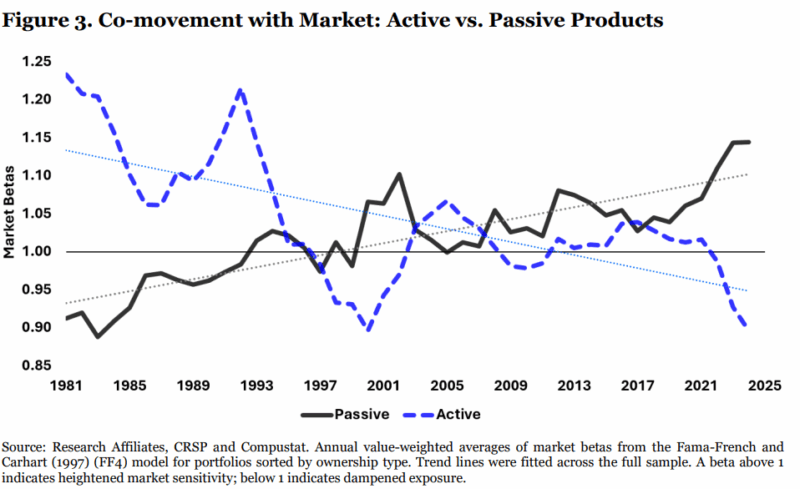

Stocks with high passive ownership are exhibiting higher betas—greater sensitivity to market movements—while those with more active ownership are showing declining betas. This divergence points to a market increasingly driven by coordinated flows rather than fundamental price discovery.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

- Price Pressure from Index Rebalancing

The mechanical process of index rebalancing creates predictable trading patterns. Large institutional index funds must buy or sell specific stocks at set times, leading to temporary price distortions. Opportunistic traders can front-run these trades, profiting at the expense of index investors and increasing implementation costs that are not reflected in headline expense ratios. - Amplification of Liquidity and Volatility Risks

Stocks with higher passive ETF ownership are more exposed to aggregate liquidity shocks. During market downturns, these stocks become particularly vulnerable, as passive funds may be forced to sell in unison, exacerbating price swings and reducing market liquidity. Adding to the problem is that large institutions and firms themselves systematically avoid buying when index funds are selling. - Reduced Market Efficiency and Price Discovery

The rise of passive investing has made stock demand more inelastic—price changes have less impact on trading volume—disrupting traditional price-setting mechanisms and making markets less efficient. This can lead to less informative prices and greater susceptibility to sharp, momentum-driven price swings.

Their findings led Brightman and Harvey to conclude:

“Collective trading behavior may undermine diversification, exacerbate liquidity risk, and cause more frequent and extreme volatility spikes. Escalating passive dominance reinforces a feedback loop in which passive inflows perpetuate price trends, active managers underperform, and capital shifts further into passive strategies.”

Investor Takeaways

While media and advisors often focus on passive funds’ low expense ratios, they frequently overlook the hidden costs associated with index rebalancing and structural inefficiencies. For example, research suggests that more efficient rebalancing strategies could reduce implementation costs by about 40 basis points per year—far exceeding the typical fund expense ratio. High-frequency traders and other active participants exploit these predictable trading patterns, further eroding returns for index investors.

Weaknesses of Index Replication Strategies

- Style Drift and Reconstitution Lag

Annual reconstitution of indices leads to unintentional style drift, as stocks migrate across asset classes throughout the year. For example, according to a 2024 study by Dimensional Fund Advisors, on average from 2010 through June 2023, roughly 25% of the Russell 2000 Index, positioned as a small cap index, was composed of the largest 1,000 stocks in the Russell 3000 Index. Similarly, the overlap between the Russell 1000 Value and Growth indices averaged about 300 companies over that period.

- Front-Running and Trading Exploitation

The predictability of index trades allows active managers to front-run passive flows, extracting value from index investors. - Inclusion of Low-Quality Stocks

Indexes often include penny stocks, bankrupt companies, or recent IPOs with poor risk-adjusted returns, which could be filtered out in systematic strategies. - Tax Inefficiency

Passive index funds have limited ability to optimize for taxes, such as harvesting losses or avoiding short-term gains. - Momentum-Driven Misvaluation

Capitalization-weighted indices mechanically add stocks after periods of strong performance and remove them after underperformance, often at unfavorable prices. Index rebalancing research shows that discretionary deletions from indices can outperform additions by a significant margin in the year following reconstitution. - Post-IPO Underperformance

The research shows that index funds that buy stocks immediately after IPO inclusion often experience subsequent underperformance.

Advantages of Systematic, Non-Index Strategies

Systematic funds that are not strictly index-tracking can mitigate many of these issues by:

- Reconstituting portfolios more frequently (e.g., monthly) to maintain consistent exposure to desired asset classes or factors.

- Avoiding predictable, mechanical trading patterns that attract front-running.

- Excluding low-quality stocks through targeted screening.

- Employing tax-efficient trading strategies.

- Taking on tracking error risk to gain greater exposure to proven return factors such as size, value, profitability, and momentum.

- Avoiding the mechanical buying of stocks immediately post-IPO by index funds that leads to underperformance.

- Trade patiently in order to be a provider of liquidity to the market instead of a taker.

Another advantage of systematic funds, in return for accepting tracking error risk, is that they can gain greater exposure to the factors for which there is persistent and pervasive evidence of a return premium (such as size, value, momentum, profitability/quality, momentum, carry, and term). For example, a small-value fund could be structured to own smaller and more “valuey” (cheaper) stocks than a small-cap value index fund. It can also be structured to have more exposure to highly profitable companies, and it can screen for the momentum effect (avoiding buying stocks that are exhibiting negative momentum and delaying selling stocks with positive momentum).

Conclusion

The dominance of passive investing has delivered enormous benefits—low costs, transparency, and broad diversification—but it is also introducing new systemic risks. These include diminished diversification, heightened volatility, greater vulnerability to liquidity shocks, and less efficient price discovery. Investors should be aware of these evolving risks and consider systematic, factor-based strategies as a way to capture the benefits of passive investing while mitigating its growing structural weaknesses.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest Enrich Your Future. He is also a consultant to RIAs as an educator on investment strategies.

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.