Can it be Good to be Bad?

- Anders Karlen Sebastian Poulsen

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our free Academic Alpha Database!

Abstract:

Investment decisions grounded in personal values and societal norms has seen a growth in the last decades, to a point where large institutional investors are abstaining from certain industries that share a specific characteristic altogether. The affiliation with sinful industries that promote human vice is not viewed as socially responsible in the eyes of the public, a reason why socially responsible investment funds that screen out these companies has experienced an increase in popularity. This study sets out to investigate the performance of American sin stocks in an attempt to increase the awareness of how these shunned industries has performed. While the existing literature provides evidence which proves sin stocks outperforms the market, we will provide further evidence concentrating on a mix of industries previously not focused on. Additionally we will extend the observation period beyond what has been done in the past. In this study, the definition of sin incorporates the industries of alcohol, defense, gambling and tobacco, and investigates the performance of a survivorship-free sample of 159 companies between July 1973 and June 2012. As performance measure, the four factor model is employed to capture any abnormal performance in relation to the market with three additional risk factors. In addition, we set out to investigate the performance of the different industries individually, to find if there is any that acts as a driver of the performance. Further, we look into the persistence of the performance over time. We find that the sample outperforms the market with 5.8% annually, and where the tobacco industry stands out with the highest abnormal return, the other industries grouped together still produce significant outperformance. The sinful index examined in this degree project has shown persistent performance, with no obvious trends of growth or decline. Unlike what has been found in previous research, the sample has shown a substantial difference in performance depending on the weighting scheme applied, not only individually for the industries, but also collectively.

Data Sources:

Data stream, 1973-2012

Alpha Highlight:

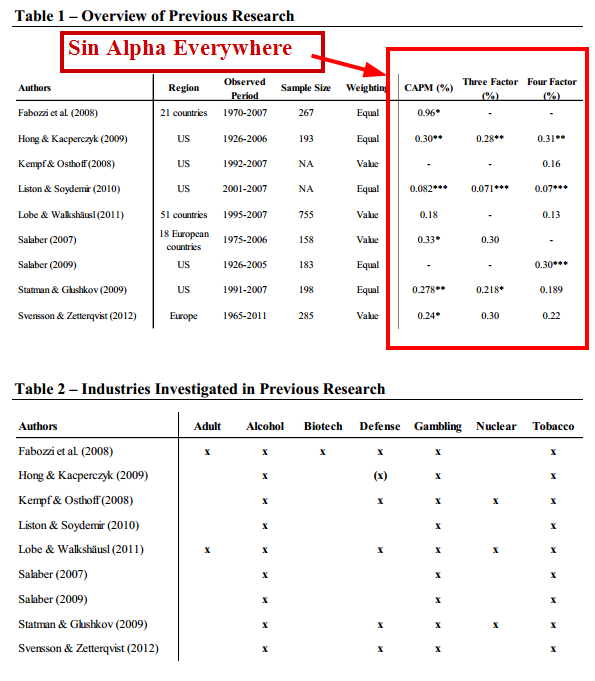

Sin alpha has been found in numerous studies:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

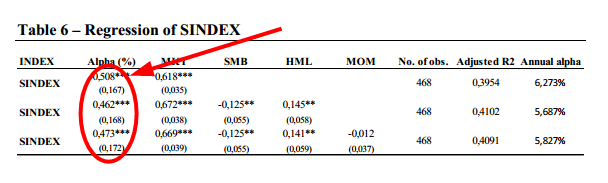

And more evidence of sin alpha from this paper. The SININDEX consists of alcohol, defense, gambling, and tobacco industry stocks, value-weighted:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

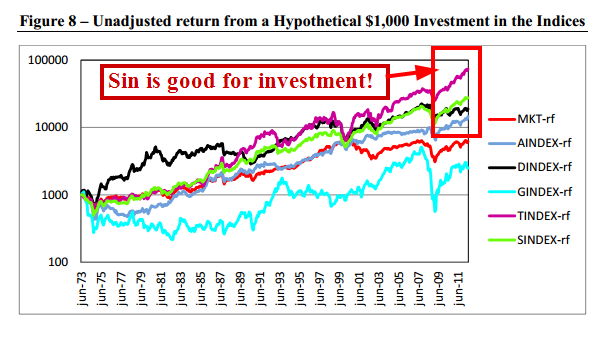

And the horse race chart:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Strategy Summary:

- Buy and hold sin stocks

Commentary:

- Socially responsible investors often represent endowments and charities. The goal of any good charity should be to maximize the benefits they can create for their stated cause. For example, if my charity is set up to cure cancer, I want to invest as much as possible in cancer-curing efforts–more investments require more money.

- By investing in a ‘socially responsible way’, charities are often hurting their charity efforts because they are generating less return that can go towards their stated cause. Why do charities and their investment advisers shoot themselves in the foot? I understand that perception matters, but what about mission accomplishment? Shouldn’t that matter the most? I’d rather cure cancer than come up short due to lack of funding because I was trying “look pretty” along the way.

- Apparently, charities and their advisers don’t understand how markets work. By withholding capital from publicly traded sin stocks, charities are not affecting anything with respect to the operations of the sin companies–they are simply providing a wealth transfer from their pocketbooks to the cold-blooded capitalist on the other side of the trade.

- The mission of any charity should be to maximize the benefits they can provide for their beneficiaries. One fairly reliable way to maximize benefits is to maximize endowment size. Call me old fashioned, but money still talks.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.