The Worst, the Best, Ignoring All the Rest: The Rank Effect and Trading Behavior

- Hartzmark

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Abstract:

In this paper, I document a new stylized fact about how investors trade assets in a portfolio setting. Specifically, investors are much more likely to sell the extreme winning and extreme losing position in a portfolio, even after controlling for a number of possibly confounding factors associated with extreme rank. The tendency to sell extreme positions is exhibited by both retail traders and mutual fund managers, and is large enough to induce significant price reversals in stocks of 40-160 basis points per month. I present evidence that this effect is related to extreme portfolio positions being more salient to investors.

Alpha Highlight:

This paper examines the trading of retail investors (1991-1996) as well as mutual fund managers (1990-2011).

The paper asks a simple question:

Given that an investor (or mutual fund manager) has a portfolio of stocks, are there certain stocks that are sold more often?

The answer is YES!

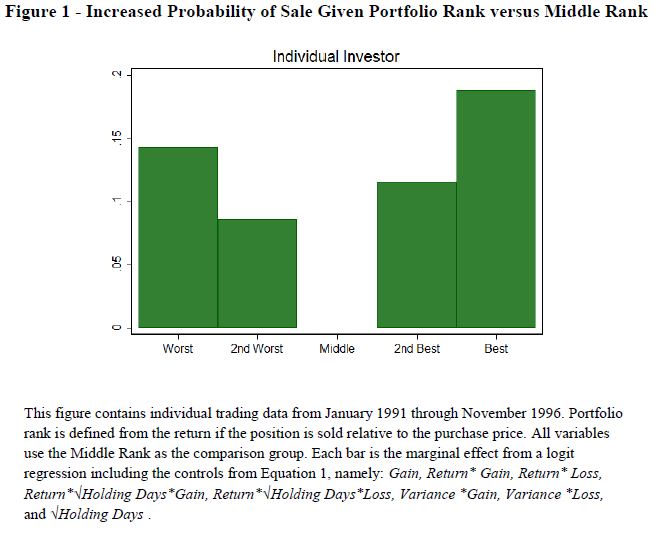

Those stocks which have done the best and the worst are more likely to be sold (As shown in the graph below).

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

It appears that saliency affects an investor’s or mutual fund manager’s decision to sell stocks, as those stocks with more extreme performance (relative to the other stocks in the portfolio), are more likely to be sold! This is found in both retail investors as well as mutual fund managers. Amazingly a simple rank variable appears to predict trading!

This results holds when controlling for the stock’s return from purchase, as this has been shown to affect trading via the disposition effect. Results also hold when accounting for tax considerations.

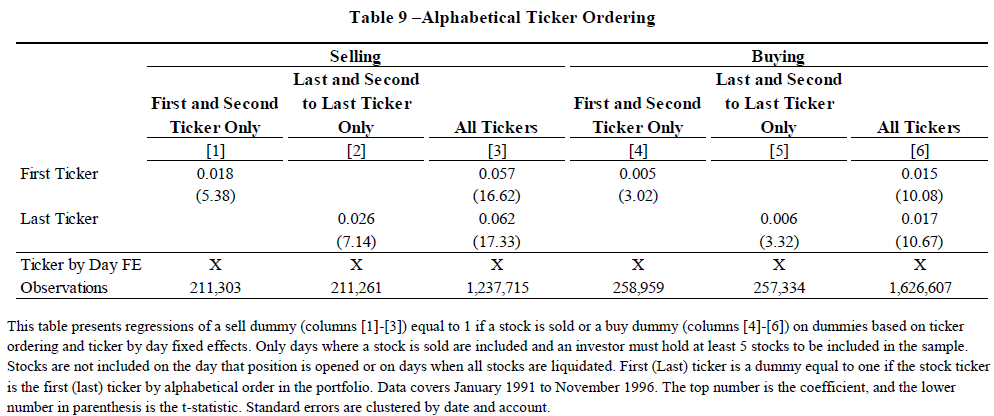

So does investor salience really drive trading activity? The paper has a neat study to investigate the “salience” idea: examine a brokerage statement. The idea is that stocks which are listed first and last will be more “salient” than stocks in the middle of a list. Here are the results:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

When the entire sample is considered (columns 3 and 6), the first ticker is 5.7% more likely to be sold and 1.5% more likely to be bought, whereas the last ticker is 6.2% more likely to be sold and 1.7% more likely to be bought!

The paper additionally finds that “The tendency to sell extreme positions is exhibited by both retail traders and mutual fund managers, and is large enough to induce significant price reversals in stocks of 40-160 basis points per month.”

The author does a great job explaining where these results fit into the broader literature:

“The broad explanation based on salience and consideration sets is not incorporated into standard explanations of rational investors or behavioral theories of trade constructed to examine the disposition effect. Explanations of the effect focus on decisions made versus homogenous reference points for each trader such as a zero return, the risk free rate, or stock specific expectations of performance. The rank of a stock in a portfolio is idiosyncratic to each trader and their portfolio. The theories of individual trade based on the disposition effect do not include this idiosyncratic component of decision making induced by the portfolio.

The rank effect provides evidence for a fundamental aspect of investor behavior – namely, that the evaluation given to any particular stock depends on what else the investor is holding. This fact may provide a micro-foundation for models that rely on disagreement across investors, such as those explaining the level of trading volume in the stock market (Stokey and Milgrom (1982)). In particular, investors may be acting differently towards the same piece of information about the same stock due to effect that other stocks in their portfolio (which are likely to differ, even for similar investors) have on the way they perceive the given information.”

Overall, an interesting paper pointing out another behavioral bias, the salience effect! So news about firm A affects me differently than another investor, if we currently have different portfolios of stocks!

About the Author: Jack Vogel, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.