Trend Following and Momentum Strategies for Global REITs

- Moss, Clare, Thomas and Seaton

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Abstract:

This study investigates whether the risk adjusted returns of a global REIT portfolio would be enhanced by adopting a trend following strategy (which is an absolute concept), a momentum based strategy (which is a relative concept and requires individual country allocations), or indeed a combination of the two. We examine the results in terms of both a dedicated Global REIT exposure, and the impact on a multi-asset portfolio. We find that the main improvements arise when the broad index is replaced with one of the four trend following (TF) strategies. The portfolios deliver similar returns but volatility is reduced by up to a quarter to the 8-9% range, the Sharpe ratios increase by 0.1 to 0.5 with the main benefit being the reduction in the maximum drawdown to under 30% compared to 43% when the broad index was used. We thus find that a combined momentum and trend following Global REIT strategy can be beneficial for both a dedicated REIT portfolio and adding REITs to a multi-asset portfolio.

Alpha Highlight:

The decade has seen an increase in interest in Global REITs (Real Estate Investment Trust). Allocating to domestic and international REITs within a portfolio helps diversify risk and generate better risk-adjusted returns, in expectation.

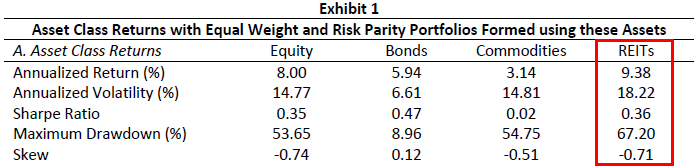

The table below shows basic statistics for 4 asset classes from 1991 to 2014. REITs are measured by the EPRA Developed Markets Index, which includes 37 developed markets. This global REITs portfolio has the highest annualized return as well as the highest volatility and maximum drawdown. If investors want to avoid unpleasant surprises down the road, risk-management within this volatile asset class is essential.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

But what can be done to reduce these hair-raising drawdowns?

Well, this probably isn’t a surprise to our readers, but a basic trend following strategy applied on REITS has been effective at reducing large drawdowns, historically.

REIT investing across countries

In Exhibit 1, REITs are considered as a single asset class, and represented as a global index consisting of a wide range of markets. In the first step, the paper disaggregates the REIT global index into 15 individual country indices (which is fewer than in EPRA). The below table shows the results based on country-level data.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

We now have equal weight and risky parity benchmarks, and we are set up for the momentum and trend following experiments, which draws from the 15-countries. In many respects, this is an application of the “dual momentum” concept developed by Gary Antonacci.

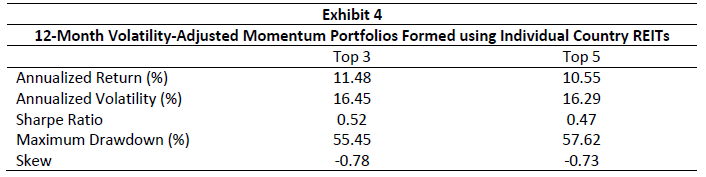

Add momentum (cross-sectional momentum)

The authors use a volatility-adjusted momentum strategy and construct portfolios formed based on top 3 and top 5 in the rankings.

How does this vol-weighting approach work?

- Volatility‐adjusted momentum rankings is calculated by, “Dividing the prior twelve month total return by the realized volatility over the same period and then ranking in the traditional fashion with rebalancing taking place monthly.”

- We can observe a substantial increase in returns and Sharpe ratios versus our benchmark from Exhibit 3.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

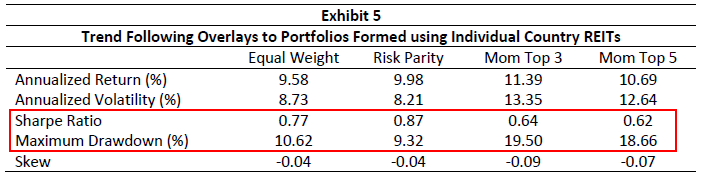

Add Trend Following (Time-series momentum)

In the next step, the paper explores adding a trend-following rule. Specifically, if the asset is classed as a “momentum winner” and the trend is “positive“, then long the position; If the “momentum winner” shows “negative” trend, then defer to treasury bills. Such “momentum” and “trend following” combinations can deliver higher risk-adjusted returns. The table below shows the performance of applying trend following rule to the four strategies (Equal Weight, Risk Parity, Momentum Top 3, and Momentum Top 5).

- Maximum drawdowns are greatly reduced and Sharpe Ratios increase dramatically.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Takeaways:

- Cross-sectional momentum has historically worked in country-level REITs.

- Adding a trend following rule can substantially decrease drawdowns and improve risk-adjusted performance in REIT investing.

Note: the authors did not study this, but we highlight in our own research that momentum can be used to select REITS at the stock by stock level. See DIY Financial Advisor for more details.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.