We’ve been focused on understanding how to communicate the concept of active fee to the broader investment community.

Active fee is an important concept because it helps investors make more informed and educated decisions — a great thing!

The concept has been around in the institutional space for a long time, but has not taken root in the retail/advisory space.

We’d like to change this reality.

Quick review: Active fee, while not perfect, is a tool to help investors understand what they are buying and how much they are paying for it. In short, active fee breaks a fund’s exposures into passive and active components — and helps an investor identify how much they are paying for the active portion of their investment.

Quick example: With active fee, an investor can conduct an apples-to-apples fee comparison between 1) a 250 stock low p/e fund and 2) a 50 stock low p/e fund. Intuitively, the fee for a 250 stock p/e fund has a larger passive component than the 50 stock p/e fund, and because investors should not pay a lot for passive exposure, the overall fee for the 50 stock low p/e fund should be higher than the 250 stock low p/e fund. Active fee helps tell us the fee levels that “equalize” the costs between the 50 stock fund and the 250 stock fund.

Consider the following assumptions:

- 50 stock low p/e fund has expense ratio = 80bps, active_share = 90%, and the Index fund = 10bps

- 250 stock low p/e fund has expense ratio = 35bps, active_share = 32%, and the Index fund = 10bps

The active fee for both of these low p/e funds is = 88bps. The implication is an investor should be indifferent between paying 80bps for a 50 stock low p/e fund or 35bps for a 250 stock low p/e fund.

Here is some more information on the concept:

Anyway, active fee is a compelling concept and helps investors make sophisticated cost/benefit trade-offs with a simple tool.

Why Aren’t All Investors Leveraging Active Fee Type Concepts?

Turns out that some investors have been leveraging this concept for a while (e.g., institutions), while other have not been (e.g., retail).

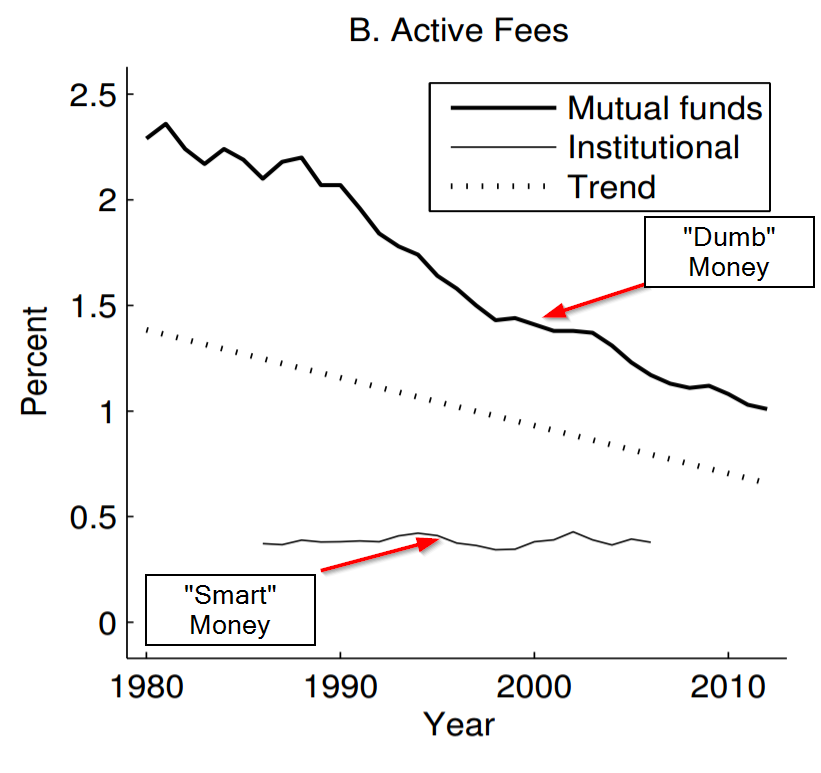

A fascinating article by Rob Stambaugh (@ Wharton) makes this point clear. Rob shows active fee across time for different segments of investors. Mutual funds, which are sold to more retail-focused investors, have been paying huge active fees for a long time — but they are coming down — fast!

In contrast, institutional investors (e.g., pensions), with more market bargaining power and arguably more sophistication, on average, have priced active management at roughly the same level throughout the sample period.

Source: author paper

Looks like institutional investors pay 40-50bps for the active component of their investments.

The natural question this raises is whether or not retail/advisory investors active fee costs will converge towards the institutional equilibrium over time. Our guess is the active fee rate will converge, but the equilibrium fee will be higher due to the economics of servicing retail/advisory investors versus institutional investors.

I’m guessing retail-focused active-fee will hit institutional pricing + 25-35bps, or a range from 65-85bps. 65-85bps is a long way to go from the ~%1.3 estimated active fee presented in Stambaugh’s paper!

Here is the source article and the abstract. Check it out…

Investment Noise and Trends

During the past few decades, the fraction of the equity market owned directly by individuals declined significantly. The same period witnessed investment trends that include the growth of indexing as well as shifts by active managers toward lower fees and more index-like investing. I develop an equilibrium model linking these investment trends to the decline in individual ownership, interpreting the latter as a reduction in noise trading. Active management corrects most noise-trader induced mispricing, and the fraction left uncorrected shrinks as noise traders’ stake in the market declines. Less mispricing then dictates a smaller footprint for active management.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.