- Title: DOES PAST PERFORMANCE MATTER IN INVESTMENT MANAGER SELECTION?

- Authors: BRADFORD CORNELL, JASON HSU, and DAVID NANIGIAN

- Publication: JOURNAL OF PORTFOLIO MANAGEMENT, SUMMER 2017 (paper )

What are the research questions?

The authors study the universe of the Morningstar Direct, survivor-bias-free, US mutual funds database from 1994 to 2015. They eliminate funds that don’t have at least 1 billion of assets and that are in the top decile of fees because they are less likely to be in institutional investor portfolios.

By simulating investor portfolio with capital allocated equally to funds in the universe, they research the following:

- Does the common manager selection research methodology based on hiring managers with recent (36 months) excess returns over the chosen benchmark and firing those who underperform, lead to future outperformance against the same benchmark?

- If we had a crystal ball and knew future performance, do the truly “skilled” manager exhibit mean reversion in their benchmark-adjusted returns?

What are the Academic Insights?

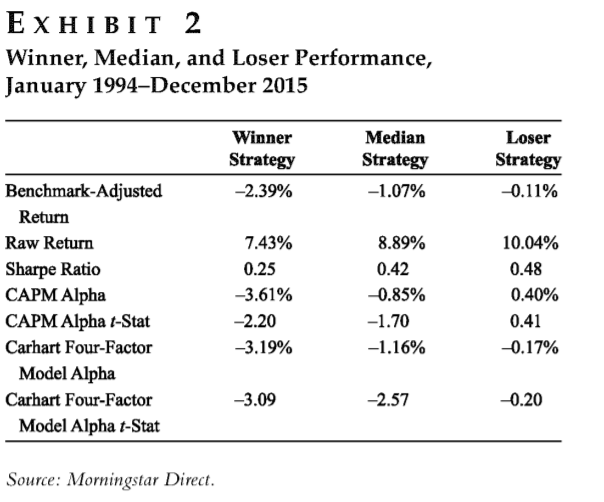

The authors look at three strategies:

- The winner strategy, which represents funds selected by the consultants ( equal positions in products that rank in the top decile of benchmark-adjusted returns);

- The median strategy ( equal positions in products that rank between the 45th and 55th percentile);

- The loser strategy, which represents funds put on a watch list by consultants and replaced in portfolios (equal positions in products that rank in the bottom decile of benchmark-adjusted returns).

The authors find the following with respect to the research questions above:

1. NO – it does not! The simulated investment results of the loser strategy consistently exceeded that of the median and winner strategy in all of the performance metrics analyzed.

Additionally, the authors compared the performance of funds that underperformed their benchmark by 1% and 3% / the “fired” funds) to those which did not underperform (the “kept” funds). The results show that the fired funds outperform the kept funds.

Furthur, the authors repeat the tests 1) using a two-year horizon for the evaluation and holding period, 2) using funds of any size; 3) using only institutional share class. Results and conclusions do not change.

2. YES – while the top 25% of outperforming funds does beat the median universe; it appears that the top decile of outperforming funds exhibit a decline in future performance. Also, by selecting the recent losers within the top 25% of outperforming funds, their future performance increases. Even the superior manager exhibits mean reversion.

Why does it matter?

Based on Morningstar Direct data (2015), investors allocate twice as many assets to active funds compared to passive solutions. Additionally, the majority of investors select managers by looking at recent (typically 3 years) performance (Goyal and Wahal, 2008).

However, because of mean reversion in manager performance, a strategy of hiring manager with mediocre track records seems to outperform a strategy that focuses on past winners.

While the authors don’t suggest to implement a strategy that substitutes past winners with past losers, they urge asset owners to focus on factors other than past performance to select managers.

The Most Important Chart from the Paper:

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.