Employees Financial Literacy and Retirement Plan Behavior: A Case Study

- Robert Clark, Annamaria Lusardi, Olivia Mitchell

- Economic Inquiry, forthcoming

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category.

What are the research questions?

- Are survey respondents more likely to contribute to the plan?

- Are the more financially literate respondents more likely to contribute to the plan?

- Do the respondents contribute a higher rate to the plan?

- Do the financially literate contribute a higher rate to the plan?

- Do survey respondents invest differently?

- Do the financially literate invest differently?

What are the Academic Insights?

The following insights are measured pre-survey:

- YES- On average, survey respondents are 6.3% more likely to contribute to the DC plan.

- YES- Of those who responded, the workers scoring 4-5 correct answers are 13.4% more likely to be contributing to the plan compared to the least financially savvy ones. Differently, those scoring 2-3 answers correctly are 6.8% more likely to contribute compared to the least financially savvy.

- YES Across the full sample, the average contribution rate to the plan is 8.7%. The authors find that those who responded to the survey contribute 1% more of their salaries compared to the non-respondents.

- YES- those who are more financially literate contribute an additional 2.6% of their earnings to the plan compared to those who are less financially literate.

- YES- those who responded held 3.7% more of their assets in equities.

- YES- the financially literate held 14.6% more of their assets in equities.

The authors continued the study by measuring any material changes in the retirement plan behavior, one year after the survey was taken.

Here are the key takeaways:

- After completing the survey, 5% of workers who did not contribute to the plan in 2013, started contributing the following year

- Workers who completed the survey were also less likely to have stopped contributing one year later

Why does it matter?

While this study is specific to employees of the Federal Reserve, a few lessons can be drawn from the analysis:

- Financial literacy (together with marital status, salary, and tenure) is a predictor of participation and contribution levels to a retirement plan.

- More financially knowledgeable employees are more likely to participate, contribute more of their salaries and hold more equities in their accounts.

- Areas of improvements: fewer than half the respondents to the survey were knowledgeable about the tax-deferred properties of the DC plan contributions.Hence, targeted information and education on this important aspect of retirement could be beneficial to improve savings decisions.

- Overall, education programs intended to boost retirement savings can add a lot of value!

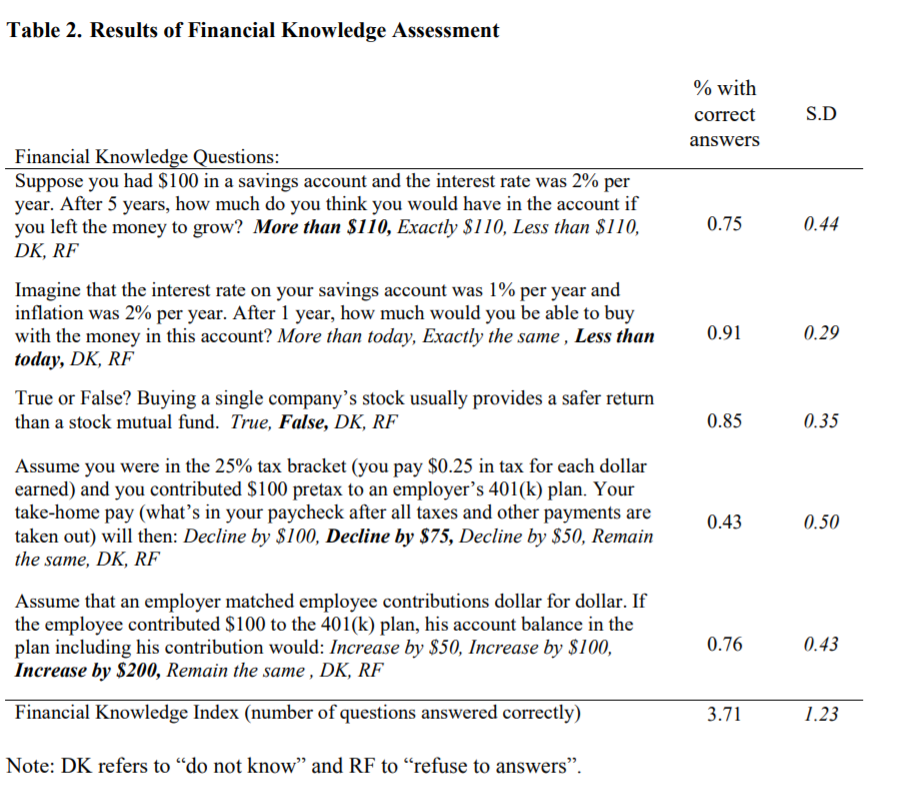

The Most Important Chart from the Paper:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

This paper uses administrative data on all active employees of the Federal Reserve System to examine participation in and contributions to the Thrift Saving Plan, the system’s defined contribution (DC) plan. We have appended to the administrative records a unique employee survey of economic/demographic factors including a set of financial literacy questions. Not surprisingly, Federal Reserve employees are more financially literate than the general population; furthermore, the most financially savvy are also most likely to participate in and contribute the most to their plan. Sophisticated workers contribute three percentage points more of their earnings to the DC plan than do the less knowledgeable, and they hold more equity in their pension accounts. Finally, we examine changes in employee plan behavior a year after the financial literacy survey and compare it to the baseline. We find that employees who completed an educational module were more likely to start contributing and less likely to have stopped contributing to the DC plan post-survey.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.