Explaining the Value Effect in Emerging Markets: Tangible vs Intangible Information

- Douglas W. Blackburn and Nusret Cakici

- A version of this paper can be found here.

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category.

What are the research questions

To most readers, it’s no surprise that our ears perk up a little bit anytime someone attempts to broaden the understanding of the value anomaly. The precise reason why high book to market equities have higher expected returns has been a long-standing debate among academics. There are two primary explanations: The first explanation postulates that the excess returns generated by the high book to market stocks are due to additional risk.(1) In contrast with that, an alternative view argues that the value anomaly is due to mispricing caused by a systematic overreaction to negative news (on average).

ref] http://lsvasset.com/pdf/research-papers/Contrarian-Investment-Extrapolation-and-Risk.pdf [/ref] What both of these theories have in common is that firms deteriorating accounting fundamentals drive the increased risk, or the overreaction to bad news. For a deeper dive into these arguments please take a look at an earlier post by Larry Swedroe titled: The Value Premium: Risk or Mispricing?

Daniel and Titman in their 2006 paper, “Market Reactions to Tangible and Intangible Information,” (2) argue that a firm’s future performance isn’t related to past accounting performance. Rather Daniel and Titman conclude that performance is related to past intangible information (information outside of accounting changes) – which is a result that is inconsistent with both the risk and overreaction hypotheses. The authors of this paper, Blackburn and Cakici, expand on Daniel and Titman’s research and explore the value anomaly in the realm of emerging markets, and ask the following:

- Do emerging markets have a consistent message that can narrow down what is driving the higher expected returns of high book to market stocks?

- Can they find the one “true” factor that explains the value anomaly across all markets?

- If the research finds that emerging markets have a relationship with tangible information, is the additional return due to risk or the overreaction hypothesis?

What are the Academic Insights?

The research team analyzed stock return and fundamental data from twenty-five emerging market countries from 1991 to 2016 (source is Datastream). The twenty-five countries were separated into 3 separate geographic regions (Asia, South America, and Europe/ Middle East/ Africa – abbreviated as AMEA). Once separated into their geographic regions, the value anomaly was analyzed by regressing book to market, tangible information, intangible information, and the net change in shares against returns.

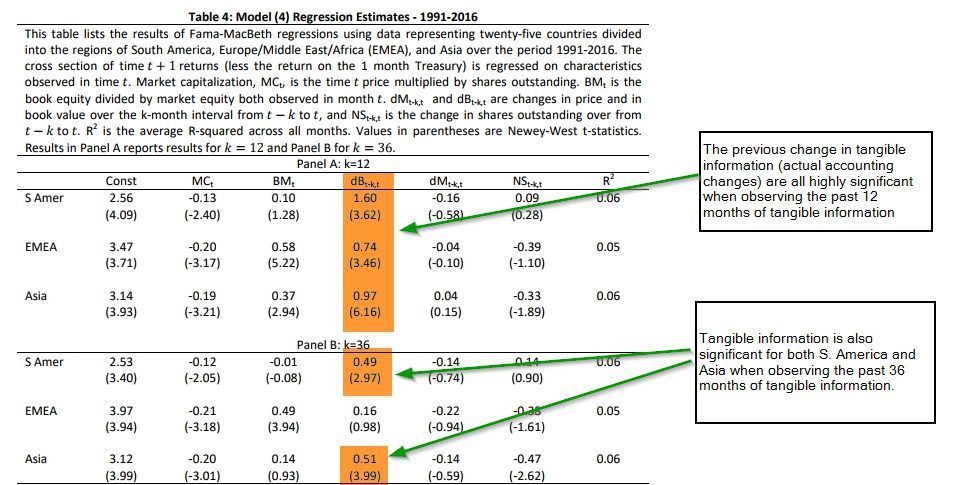

- YES – The authors found that in emerging markets tangible information (past accounting performance) is significantly related to expected returns. The findings were particularly strong for all regions when the observable period of tangible information was 12 months. When observing intangible information over the previous 36 months the results were still significant for two of the three regions but to a lesser degree. These results were fairly consistent across all regions, subgroups based on size, and sub-periods.

- NO – The results of this study showed completely different results than what has been observed in the US markets. Daniel and Titman found that intangible information (changes in market cap unrelated to accounting changes) was significant in explaining the higher expected return of high book to market firms. This is in stark contrast to the results that Blackburn and Cakici found in emerging markets. Therefore the research was unable to identify the one true characteristic that underlies the value anomaly.

- Risk – The researchers were unable to find evidence that supported the overreaction hypothesis in emerging markets. Due to the lack of evidence supporting the overreaction theory, they concluded that the higher expected return must be due to the additional risk assumed when purchasing high book to market equities in emerging markets.

Why does it matter?

High book to market stocks have been shown to exhibit higher expected returns across multiple markets, and value investors (myself included) have clung to the belief that “Mr. Market” is wildly over-reactive to bad news. The finding that expected returns in emerging markets are highly related to tangible information, but without exhibiting any overreaction, came as a surprise. The faith-based value investor in me wants to pound the table and say it can’t be so, but as Wes likes to point out, we ought to be investing based on evidence, not faith. The evidence put forth in this paper disputes the overreactions of Mr. Market in what you’d assume would be some of the least mature (and most likely to overreact) markets in the world.

In short, it seems to be a case of, “Who the hell knows.”

What is the most important chart from the paper?

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Abstract

High book-to-market stocks earn higher average returns than low book-to-market stocks. This result has been verified using stock returns from the U.S., developed, and emerging markets. Why B/M explains expected returns is still an open question. In this paper, we use stock returns representing twenty-five emerging markets to differentiate between competing theories. Our results differ from papers studying the U.S. stock market. For emerging markets, the component of book-to-market that is related to tangible information (past accounting performance) is significantly related to expected returns while the component related to intangible information is not. We then differentiate between the overreaction and risk explanations. We find little evidence of overreaction in the emerging markets suggesting that the B/M is likely a proxy for some risk factor. Our evidence is consistent across emerging market regions, across size groups, and across subperiods.

About the Author: Rich Shaner, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.