Sex Matters: Gender Bias in the Mutual Fund Industry

- Alexandra Niessen-Ruenzi, Stefan Ruenzi

- Management Science, forthcoming

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category.

What are the Research Questions?

- Do investor care about the fund manager gender?

Specifically:

- (Rational explanation) Do they manifest statistical discrimination (based on performance evidence)?

- (Irrational explanation) Do they manifest prejudice against female fund managers due to gender bias?

What are the Academic Insights?

By conducting a combination of empirical and laboratory tests (including an Implicit Association Test-IATs*), the authors find the following:

- NO- There is no evidence for gender differences among fund managers that would support the view that shying away from female managers could be rational: their investment styles are more persistent over time than those of male fund managers, while average performance is virtually identical and male fund managers exhibit less performance persistence

- YES- Linking the results from the IAT back to subjects’ investment behavior, the authors find that subjects with high IAT prejudice scores do indeed invest significantly less in female-managed funds in the experimental investment task, while subjects for which the IAT does not indicate any gender bias do not invest less in these funds.

* IATs are an established experimental method regularly employed by social psychologists to uncover prejudice based on associations. IATs consist of computerized sorting tasks and allow researchers to measure implicit associations between concepts

Why does it matter?

This study shows that gender bias of investors can have a strong impact on financial markets. This helps to clarify why female-managed funds receive much lower inflows than male-managed funds. The authors speculate that, as managers generating low inflows are not attractive for fund companies to hire, customer-based discrimination is a possible new explanation for the low fraction of female managers in the mutual fund industry.

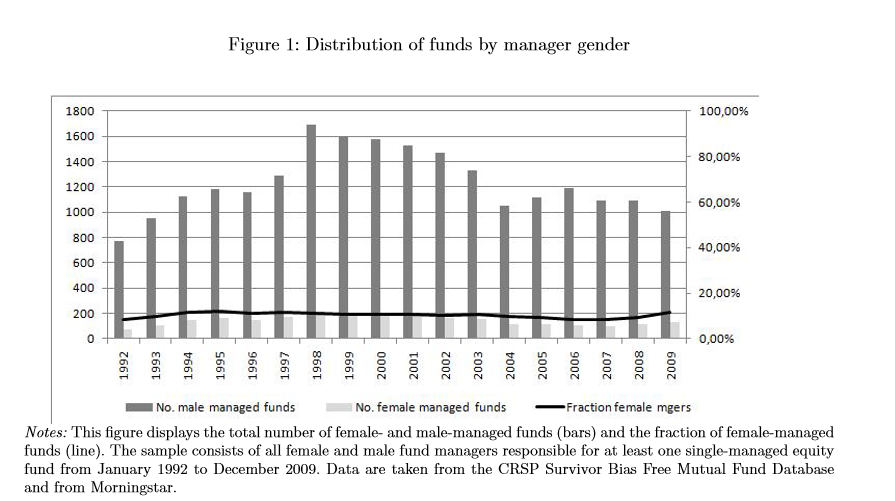

The Most Important Chart from the Paper:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

We document significantly lower inflows in female-managed funds than in male-managed funds. This result is obtained with field data and with data from a laboratory experiment. We find no gender differences in performance. Thus, rational statistical discrimination is unlikely to explain the fund flow effect. We conduct an implicit association test and find that subjects with stronger gender bias according to this test invest significantly less in female-managed funds. Our results suggest that gender bias affects investment decisions and thus offer a new potential explanation for the low fraction of women in the mutual fund industry.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.