Day of the Week and the Cross-Section of Returns

- Justin Birru

- Journal of Financial Economics, forthcoming

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

According to psychology literature, mood increases from Thursday to Friday and decreases on Monday. In general, people tend to evaluate future prospects more optimistically when they are in a good mood than when they are in a bad mood. In equity markets, the presence of optimism or pessimism that is unrelated to fundamentals, usually called sentiment, delivers clear, testable cross-sectional return predictions. Specifically, a change in sentiment will have a contemporaneous effect on returns, with the strongest effect occurring for the prices of stocks that are hard or highly subjective to value and hard-to-arbitrage (Baker and Wurgler, 2006). This hypothesis therefore predicts that relative to non-speculative stocks, speculative stocks(1) will experience low returns on Mondays and high returns on Fridays.

The author investigates the following research question:

- Do certain anomalies exhibit return variation across days of the week?

- If so, is there evidence that such results are driven by firm specific or macroeconomic news?

- Is this day-of-the-week variation related to similar patterns in moods?

What are the Academic Insights?

The author finds the following:

- YES- For all anomalies with one speculative and one non-speculative leg ( 19 total are studied in this paper), the long minus short strategy returns exhibit opposite signs on Monday and Friday. Consistent with a mispricing explanation, all of the variation is driven by the speculative leg, not the non-speculative leg. The results remain robustly present for all such anomalies in every subsample period examined. Additionally, the author considers 44 anomalies that do not have a clear speculative and non-speculative leg (i.e. momentum). In this case, there is no evidence of similar day of the week patterns.

- NO- The observed cross-sectional return patterns are robust to the exclusion of firm-specific and macroeconomic news announcements.

- YES- Long minus short portfolio returns monotonically increase (decrease) from Monday through Friday for strategies for which the speculative leg is the short (long) leg. These results are related to the small, but growing literature that identifies exogenous changes in mood and shows a causal effect of these changes in mood on stock returns. Mood is a powerful determinant of individual actions, and changes in mood have been found to induce less than fully rational financial market behavior not just from individual investors, but also from institutional investors.

Why does it matter?

This study documents strong, predictable variation in the cross-section of returns across day of the week for a certain type of anomalies and it also shed some more light on how behavioral finance has an important role in understanding financial markets.

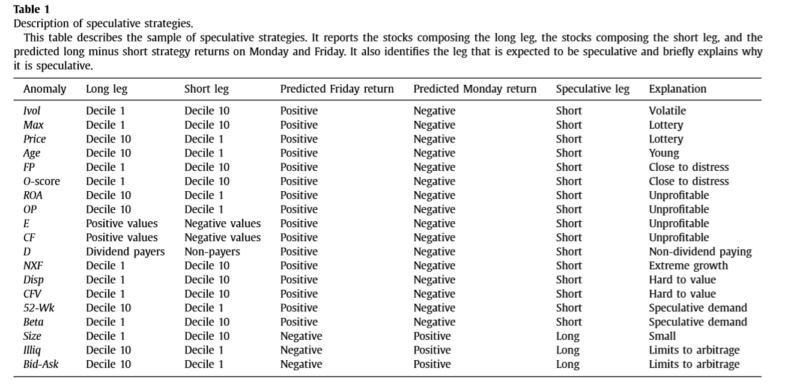

The Most Important Chart from the Paper:

Table 1 shows the list of 19 anomalies studied in this research:

Abstract

Long-short anomaly returns are strongly related to the day of the week. Anomalies for which the speculative leg is the short (long) leg experience the highest (lowest) returns on Monday. The opposite pattern is observed on Fridays. The effects are large; Monday (Friday) alone accounts for over 100% of returns for all anomalies examined for which the short (long) leg is the speculative leg. Consistent with a mispricing explanation, the pattern is driven by the speculative leg. The observed patterns are consistent with the abundance of evidence in the psychology literature that mood increases on Friday and decreases on Monday.

References[+]

| ↑1 | The term speculative refers to stocks that are hard or highly subjective to value properly and/or stocks that have the greatest impediments to arbitrage. Stocks that are difficult to arbitrage or difficult or subjective to value tend to be stocks that are small, young, volatile, unprofitable, non-dividend paying, lottery-like, prone to speculative demand, potentially close to distress, or extreme growth. |

|---|

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.