One of the mistakes that prevent investors from achieving their goals is that when it comes to evaluating investments and investment strategies most think that three years is a long time, five years a very long time, and 10 years an eternity. This is true of both individuals and institutional investors alike as the typical review cycle for institutional money managers is three years. This traditional approach continues even though the research consistently shows that this approach leads to underperformance. Among the studies finding that the managers fired go on to outperform the ones that were hired to replace them are “The Trust Mandate” by Herman Brodie and Klaus Harnack, “Institutional Investor Expectations, Manager Performance, and Fund Flows,” by Howard Jones and Jose Vicente Martinez, and “The Selection and Termination of Investment Management Firms by Plan Sponsors,” by Amit Goyal and Sunil Wahal.

Despite the evidence demonstrating that manager performance chasing is a loser’s game, the tradition continues, making this behavior one of the great anomalies in behavioral finance—why do investors keep repeating the same behavior and expecting a different outcome? Einstein said that was the very definition of insanity.

We might consider that there is another anomaly here: If markets are efficient then future outperformance should be random. Yet, the studies all show this not to be the case. If future outperformance was random, past losers would not outperform past winners persistently. Which raises the question: Why does this occur? An explanation is provided by Rob Arnott, Vitali Kalesnik and Lillian Wu, authors of the study “The Folly of Hiring Winners and Firing Losers,” published in the Fall 2018 issue of the Journal of Portfolio Management.

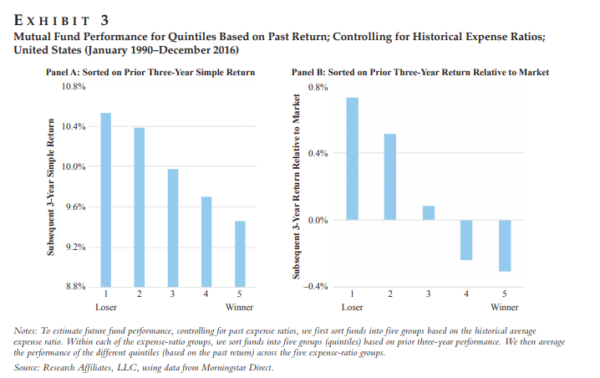

They used the Morningstar Direct Mutual Fund Database, covering the period of January 1990 to December 2016. Their sample included 3,331 U.S. mutual funds, both live and dead. By 2016, the sample included about 1,800 funds. The following is a summary of their findings:

- The holdings of underperforming managers tend to be dominated by recently underperforming (and often newly cheap) styles/factors. The holding of cheaper assets, with cheaper factor loadings, sets them up for good subsequent performance.

- The holdings of outperformers tend to be dominated by recently outperforming (and now often newly expensive) styles/factors. The holding of expensive assets, with more expensive factor loadings, sets them up for poor subsequent performance.

- The relationship between expenses and subsequent performance is reliably negative; high fees often imply lower returns.

- On a simple return basis, over three-year horizons, recent winners, on average, underperform recent losers by 1.1 percent per year.

- Past outperformance over three-year horizons relative to the market leads, on average, to future underperformance, whereas past underperformance is usually followed by future out- performance. Recent winners, on average, underperform the recent losers by 1.0 percent per year.

- Once returns are controlled for factor exposures the underperformance disappears—pointing to the source of underperformance (factor loadings).

- The results were similar for both one- and five-year horizons.

Summarizing, chasing performance results in a buy high (expensive) and sell low (cheap) strategy—not exactly a winning strategy. The problem is buying past losers not only seems counterintuitive, but buying past winners is more comfortable than buying past losers. The evidence led Arnott, Kalesnik, and Wu to conclude that in evaluating performance, ignorance of relative current valuation levels is naïve.

They added:

“Equity factors, just like individual stocks or different asset classes, can become cheap at certain times and expensive at other times.”

They also observed:

“Just like individual asset classes or individual stocks, factors tend to perform better from a starting point of trading cheaply and tend to perform worse after they become expensive.”

The bottom line is that valuations matter whether we are talking about market beta or any other factor or asset class. To test this point, they analyzed the performance of the various factors.

The value factor is long a value portfolio and short a growth portfolio. Size is long a small-cap portfolio and short a large-cap portfolio.

“The relative valuation is based on the valuation of the long portfolio relative to the short portfolio. This relative valuation is a blend of four relative-valuation ratios: price to book, price to five-year average sales, price to five-year average cash flows, and price to five-year average dividends, each computed for the long portfolio relative to the short portfolio. The average valuation indicates whether the factor is trading cheap or rich relative to historical norms.”

They also examined the factors of momentum, low beta, illiquidity, profitability, and investment. The period covered was from 1967 through 2016.

Arnott, Kalesnik, and Wu found a negative relationship between valuation and subsequent return, illustrating that as the factor becomes cheap, it tends to perform better; as it becomes expensive, it tends to perform worse [emphasis mine].

They concluded:

“Factor returns and the subsequent factor valuation are powerfully correlated. Lousy past performance leaves factors cheap, whereas brilliant past performance leaves them expensive. The strong and consistent positive correlations between past performance and the resulting relative valuations suggest that equity factors tend to become cheap as they underperform and tend to become expensive as they outperform.”

This helps explain why past winners tend to disappoint, whereas past losers tend to positively surprise.

Arnott, Kalesnik, and Wu found that most funds have persistent factor exposures, and those exposures explain the lion’s share of the fund’s return in excess of the market. Thus, “when a factor performs poorly, it drags down the fund’s return, which contributes to cheap valuations that lead to future superior performance. It also works the other way around: Stellar performance of a factor will boost the fund’s return, pushing its valuations higher until they are very expensive, and setting the fund up for future disappointing performance.” They found similar results in international markets—“the predictability of future return based on past return seems to be subsumed by factor-implied valuations and fees.”

Summary

While individual and institutional investors alike focus on short-term (whether 1-year, 3-year, or 5-year) performance, the evidence makes clear that doing so is a loser’s game. What’s surprising is that despite all the evidence being well known, having appeared in published journals, the behavior persists. It seems human behavior is very difficult to change, especially when the right actions seem counterintuitive. When this is the case, instead of changing behavior, we tend to experience cognitive dissonance. The result is we keep repeating the same bad behavior while expecting a different outcome. You don’t have to keep making that mistake.

Arnott, Kalesnik, and Wu offered this advice: “Given that what is comfortable is rarely profitable, having the discipline to follow a much less orthodox and quite uncomfortable approach to investment may translate into far better performance.” It’s uncomfortable because “when we sell high and the asset moves higher, we feel foolish. ‘Buying low’ is even harder. Anything that is newly cheap has inflicted pain and losses in its path to low prices. It is impossible to know where the bottom is, so buying low inevitably leaves us looking and feeling foolish until the turn. ‘Buy low, sell high’ is therefore a painful path to success.” That is why, as Warren Buffett noted, investing is simple, but not easy.

I hope you keep these lessons in mind the next time you are tempted to abandon a well-thought-out investment strategy (supported by evidence of a premium that has shown persistence, pervasiveness, robustness, and intuitiveness, as well as having logical risk-based or behavioral-based explanations for why you think it should persistent) that has experienced underperformance over three- , five-, or even 10-year periods. Remember, all risky assets must be expected to endure random long periods of underperformance. Otherwise, there would be no risk, and they would not carry risk premiums as compensation for that risk. And given that all risky assets should be expected to endure such long periods, the prudent strategy is to diversify across as many unique sources of risk and return that we can identify that meet our investment criteria of persistence, pervasiveness, robustness, intuitiveness, and implementability.

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.