And the Winner Is…A Comparison of Valuation Measures for Equity Country Allocation

- Adam Zaremba and Jan Jakub Szczygielski

- Journal of Portfolio Management

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

The use of valuation multiples in selecting equity securities is well established in the literature, and we’ve covered the research on enterprise multiples here (here is a recent JPM on the topic). However, there are relevant questions as to the effectiveness of multiples when applied to national indexes in the service of country allocation. Contrary to popular opinion, studies show that not every ratio is the same as every other, although practitioners tend to focus on Book to Market as their go-to approach. To contribute to the existing literature, the authors examine 73 country equity indexes from 1995 to 2017 and calculate 14 value ratios. The ratios are calculated with Net Profit (NP), Book Value (B), Cash Flow (CF), EBITDA, Gross Profit (GP), Sales (S) and Dividends (D) in the numerator, each one across two denominators: Market Equity (ME) and Enterprise Value (EV). Application of a long-only and long/short configurations occur via ETFs across countries and time periods. Four-factor risk models are used to disaggregate returns and establish robustness.

Here is what they address:

- Which is the best valuation ratio for country selection in terms of historical performance?

- Are the results robust relative to risk?

- Are the results robust across markets?

- Are the results robust over time?

- Can the relationships observed be converted into profitable investment strategies after trading costs?

What are the Academic Insights?

- EV MULTIPLES, especially EBITDA/EV. A long/short using EBITDA/EV (hereafter EB/EV) equally weighted portfolio of country indexes returned 0.69% with a Sharpe Ratio of .81 (2x that found for BK/ME), Although most of the ratios were significant in predicting returns, the EV multiples exhibited higher t-stats when compared to ME multiples. Traditional BK/ME ratios were not significant. Ratios based on EBIT and SALES were superior to those based on NET PROFIT, BK, and DIVIDENDS.

- YES. When controlled for known predictors of country index returns, including momentum, size of market, long-run reversals, cross-sectional seasonality, and beta, ratios based only on EBITDA and SALES remained significant. This was true when both EV and ME were included in the denominators. Again, EBITDA/EV was the superior performer. When Carhart risk adjustments were made, only five ratios exhibited significance including EBITDA/ME, GP/ME, SALES/ME, SALES TO EV AND EBITDA/EV, with the latter the clear winner again.

- NO. Risk-adjusted excess returns were confined to emerging and frontier markets. When the analysis is conducted on the subset of the developed markets, only one ratio (GP/EV) remained significant and for emerging markets, several (EBIT/ME, GP/ME, S/ME, S/EV) remained significant. Frontier markets produced 9 significant ratios out of the 14 tested (CF/ME, NP/ME, EB/ME, D/ME, NP/EV, B/EV, EB/EV, S/EV, D/EV), large and significant alphas were also observed with EB/EV producing the best performance. In any case, it is apparent that the least liquid and smallest markets account for the majority of the profitability associated with using value ratios to construct profitable long/short country strategies. It is also apparent that the limitation to frontier markets is a major impediment to the application of a value-based ratio approach to country allocation.

- NO. With the exception of the D/EV ratio, all other multiples strategies failed to produce a significant alpha since mid-2006. EB/EV ratio included. Exhibit 7 in the paper illustrates a clear shift in the profitability of using either ME or EV based value ratios to predict country returns. In 2006, there is a marked flattening of the profitability relationship. Between 1995 and 2006 however, a steep and positive relationship between cumulative returns and either type of valuation ratio existed. Whether or not this is a temporary or permanent regime shift remains to be seen. It is, however, a much-debated topic at the stock level.

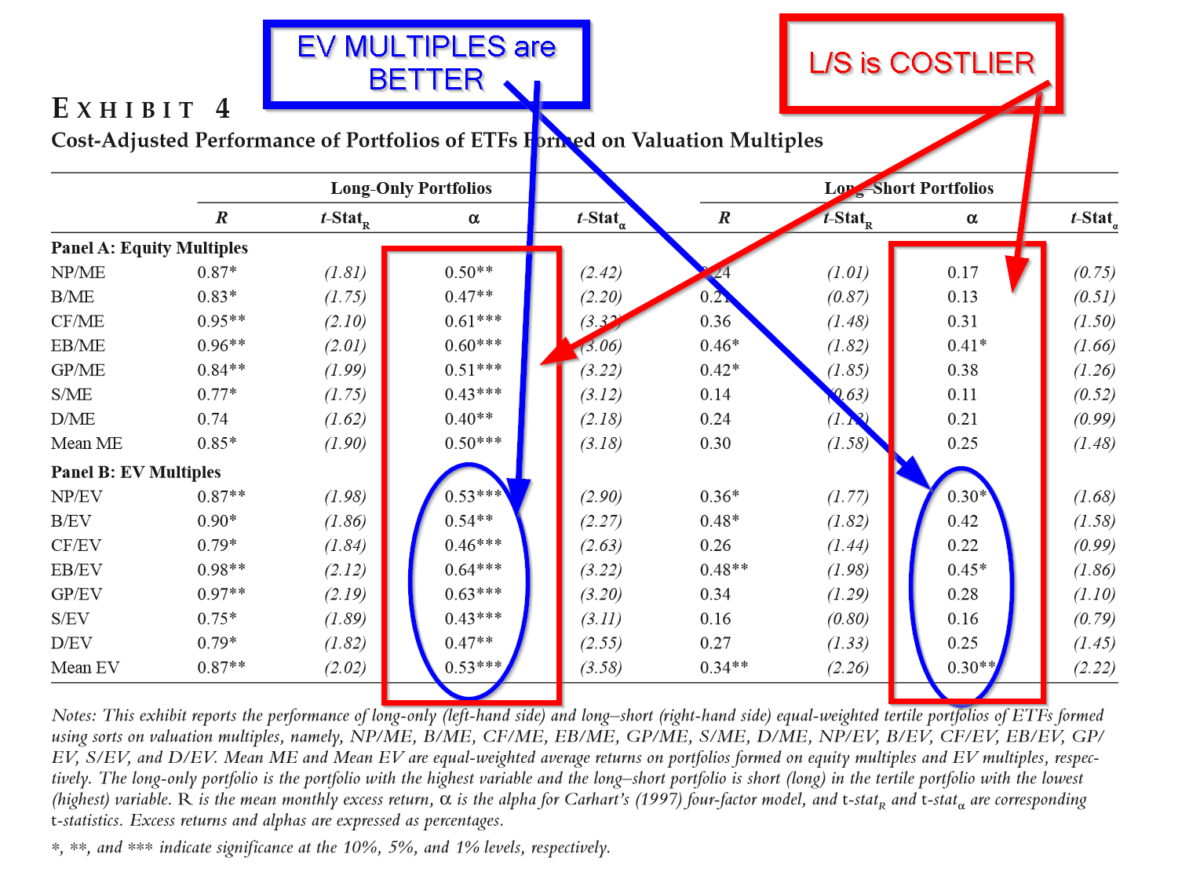

- YES. The results presented in Exhibit 4 below show the potential profitability of implementing the country strategy in the long-only and long/short configurations. All ratios and configurations produce significant risk-adjusted and profitable results for the long-only configuration. Once again, the EBITDA to EV ratio is superior and produces an average monthly excess return of 0.64% (t-stat 3.22). The more costly long/short portfolio constructed using EBITDA to EV is the only ratio with significant results, producing an average risk-adjusted excess return of 0.45% (t-stat 1.86).

Why does it matter?

The authors put together a smart application of the use of typical valuation ratios to country allocation. Although this idea seems obvious now that the study is published, it does contribute to the literature on value investing. Similar to stock selection, the traditional and commonly applied ratio (book to market) performs poorly when applied to country selection. This should not be a surprise, but it is a useful finding and is consistent with the academic literature. Quite a few of the 14 ratios examined here have never been tested at the country level in the literature. Questions of stability over time aside, the ratios identified as good or superior performers now extend the set that could be employed by retail investors, ETF providers, and asset allocators.

The most important chart from the paper

Abstract

The authors evaluate and compare the usefulness of various valuation ratios for equity country allocation. To this end, the performance of 73 national equity indexes is investigated for the period 1996 to 2017. The earnings before interest, tax, depreciation, and amortization (EBITDA)to-enterprise value (EV) multiple is the best predictor of performance and outperforms other metrics. An equal-weighted portfolio that is long (short) in the tertile of countries with the highest (lowest) EBITDA-to-EV ratio produces a mean monthly return of 0.69% and a Sharpe ratio of 0.81, which is more than double the Sharpe ratios obtained from using traditional metrics such as the book-to-market ratio or dividend yield. Two major drawbacks of intercountry value strategies are identified: (1) payoffs are derived predominantly from emerging and frontier markets and (2) profitability has significantly declined in the last decade.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.