Impact Investing 2.0: Not Just for Do-Gooders Anymore

- Diana Lieberman

- The Journal of Investing, Winter 2020

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

Can we do impact investing that is both good for us and tastes better? In the past, if an investment had positive non-financial outcomes (positive impact), a return trade-off was expected. Today, some investors find that incorporating aspects such as diversity, stakeholders, and environmental sustainability leads to stronger companies and investments. Clearly not all healthy meals are tasty. Similarly, incorporating these factors does not necessarily guarantee higher returns. The author addresses four key questions:

- What is Impact Investing?

- What are the return and impact spectrum?

- Where does Impact Investing stand today?

- What is Impact Investing 2.0?

What are the Academic Insights?

- If you ask five people what Impact Investing is, you will likely get five different answers. Anthony Bugg-Levine is often credited with creating the phrase “impact investing” in 2007 when he was at the Rockefeller Foundation. He used this term during a meeting regarding types of investments with more than a single aim that would leverage capital in a way beyond what traditional grants could (Greene 2014). Foundations pursue their missions with grants, Program Related Investments (PRIs) where an investment is expected to be paid back with no (or low) interest, and with Mission Related Investments (MRIs), which have a modest return expectation. Impact Investing started to evolve from these three vehicles. The investment-oriented evolution began with socially responsible investing (SRI). SRI Investing happens when: 1) Investors would exclude certain industries or companies that, from a social or environmental standpoint, were felt to be undesirable; 2) Very large shareholders or groups of shareholders can encourage corporate responsibility and discourage unsustainable or unethical practices (shareholders advocacy). Then came Environmental, Social, Governance(ESG). ESG investing expands opportunities beyond negative screening. Rather than including or excluding a company based on its industry or product line, an ESG analysis looks at a company through a broader lens by including the company’s ESG practices. ESG investing began its evolution toward impact investing when it adopted an economic and financial reason for incorporating the ESG factors into the investment decision. Analyzing these factors and incorporating the relevant ones enhance return potential rather than detract from it. For instance, companies actively working to reduce their carbon footprint most likely will have lower future energy costs compared to companies that do not prioritize energy efficiency. Studies (here and here )show that board diversity allows for divergent views, which create more well-rounded decisions and thus a more effective governance process.

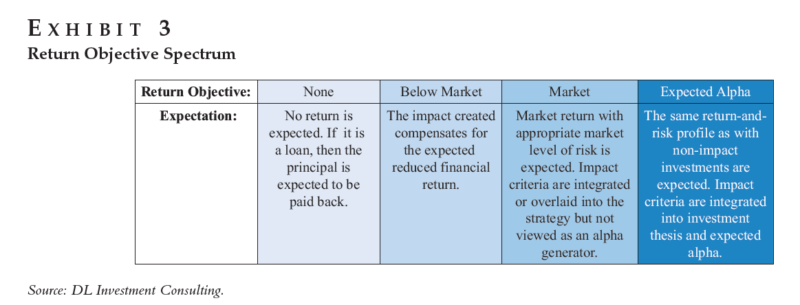

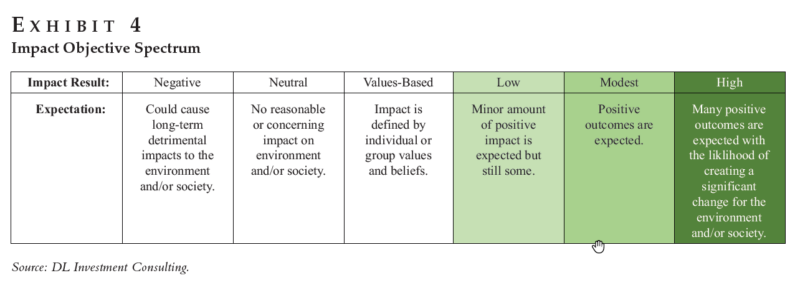

- There is a wide range of return and impact objectives in the field. As Exhibit 3 shows, on one end, no return is expected, as with grants or PRIs, and on the opposite end of the spectrum, the investor anticipates an above-market return. Obviously, the philanthropic capital is the only funding source with no return expectation and is fairly unlikely to seek above-market returns. Differently, the investment-oriented capital is more likely to meet the market return objective. Some impact investors accept below-market returns, expecting a social return that will compensate for the reduction. The acceptable amount of trade-off between investment return and social return varies depending on the investment and the investor (for example, microfinance). Recently, more and more impact investors are looking to achieve market and above-market returns. The investors who are looking to achieve a market return while incorporating impact or sustainability into their investment strategy—and who do not vie it as an alpha generator—fall within the purview of values-oriented investors (for example, MSCI ESG Focus Indexes). Finally, investment strategies looking to perform better than the market will incorporate ESG factors as a theme because investors see added value in them. Just as there is a return spectrum for impact investing, there also is an impact spectrum. Exhibit 4 shows that this spectrum ranges from having a negative impact to having a high positive impact, along with the possibility of having no meaningful or known impact. Impact investing is related to the last three colored columns in the table. A low impact investing example is a solar bond. A modest impact investing example is a real estate example of retrofitting an existing building to be energy efficient and provide a healthier and community-oriented workplace. Finally, a high impact investing example is a Kenyan solar energy private company selling home solar systems in Kenya, Tanzania, and Uganda. The solar power replaces dangerous kerosene lamps that are the only option for many households. Determining where an investment belongs on the return spectrum is fairly straightforward since the return expectation is an integral part of the due diligence process. Accessing the level of impact is not as clear cut, especially when trying to determine it ahead of time. Therefore, it is important to view these impact categories conceptually and to incorporate both qualitative and quantitative information when considering specific investments.

- According to the Global Sustainable Investment Alliance (2016) investment review, global assets under management incorporating sustainability factors total $23 trillion, up 25% from 2014, and estimates of responsible investing accounts are 26% of all professionally managed assets globally. Additionally, Morningstar reports that the number of sustainable funds offered to US investors at the end of 2018 showed a 49% increase (a total of 351 funds) over the last 12 months (Hale 2019). The main point dividing the enthusiasts from the skeptics is whether Impact Investing is additive to performance or not. The skeptics often cite a study that shows underperformance for strategies incorporating the use of impact investing (Caplan, Griswold, and Jarvis 2013). This study like others focuses on SRI strategies with exclusionary screens. Differently, research on strategies integrating ESG and sustainability factors based on their economic or investment merits shows a different picture: companies with high ratings for CSR and ESG have a lower cost of capital in terms of debt and equity; companies with high ESG ratings exhibit market-based outperformance as well as accounting-based outperformance.

- The author of this paper refers to “Impact Investing 2.0” as an above-market return expectation in which the positive impact component is a contributor to the alpha. In other words, the drivers of the impact are integrated into creating the above-market return. Additionally, Impact investing 2.0 is based on understanding the future implications of social and economic shifts that are creating investment opportunities often missed by other investors. For example, most people agree that climate change is occurring; nevertheless, many investors view it as a far-off problem and not a priority in their investment programs. More specifically, a consequence of climate change is the possibility of clean water scarcity. This is not a too far-off problem as Cape Town, South Africa, recently experienced a serious drought and came close to what observers were calling Day Zero. Companies that own water purification technologies are only one type of investment that could be in high demand as the world deals with these new conditions. Other examples of Impact Investing 2.0 are advancements in the financial ( impact implications within financial inclusion objectives), health care ( patients and doctors have easy access to multiple sources of information and improving ways to use this information to weed out the irrelevant from the pertinent is just one way that medical informatics enhances our overall well-being), and education sectors (ability to provide a good education worldwide is another benefit of the increased access to information). The author also clarifies what Impact Investing is NOT: it is not values-based investing with many advancements in incorporating one’s values into a portfolio without adding significant levels of risk. As discussed previously, since there is no economic or financial driver motivating this activity, it falls into more of an SRI approach.

Why does it matter?

Impact Investing is becoming increasingly popular. What was once thought of as a one-off investment strategy now has its own department at many of the most prestigious investment organizations. This article does a great job of defying what it is and what to look for in due diligence processes. As far as the due diligence process, a good first step to incorporating impact investing 2.0 into an investment program is to review the current holdings. For both asset owners and managers who do not have the capability to do such analysis themselves, using a third-party ESG and sustainability rating analysis represents a good start. But it is important to remember to look behind those ratings and understand the rationale of the holding. Just as with any accounting metric, it is beneficial to understand how the number is derived. Don’t just take a sustainability metric at face value. A successful analyst does not do that.

The Most Important Chart from the Paper

Abstract

Impact investing is a rapidly evolving field—depending on the type of investors asked, they will give a variety of definitions and expectations. Much of the field has derived from philanthropic roots; however, the latest developments are driven by an investment perspective. The historically assumed trade-off between financial return and social benefit is no longer a given. Astute investors realize that incorporating sustainability and environmental, social, and governance (ESG) factors into their analysis will often enhance long-term returns. Many of these impact-oriented trends are overlooked or undervalued by traditional investors, leaving an investment opportunity for those ahead of the curve. Before discussing the financial applications to impact investing, the article provides an overview of impact investing and its two disparate evolutionary paths, along with differing return and impact expectations. Impac investing 2.0 stems from the field’s investment side, and its primary characteristic is that the drivers of the impact are integrated into creating an above market return, attracting all types of investors.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.