Security Analysts and Capital Market Anomalies

- Li Guo, Frank Weikai Li, K.C. John Wei

- Journal of Financial Economics

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

Do analysts actively exploit anomalies when they recommend stocks? Do analysts’ research efforts contribute to efficiency in the equity markets? Good questions. This research clarifies the relationship between established stock return anomalies and analyst recommendations. Given that anomalies are so well-documented and so well-known, and if analysts are “sophisticated informed and unbiased”, it makes sense that they should be willing and able to take advantage of them. However, if analysts are “biased and uninformed” they may make recommendations inconsistent with these anomalies. As a result of ignoring anomalies they may represent a significant friction in the market and significantly contribute to mispricing. The research completed in this paper examines long-short portfolios of 11 anomalies including net stock issuance (NSI), composite equity issuance (CEI), total accruals (Accrual), net operating assets (NOA), asset growth (AG), investment to assets (IA), gross profitability (GP), return on assets (ROA), momentum (MOM), financial distress (Distress), and Ohlson O-score (O-score). The 11 anomalies were combined into two composites—PERF (Distress, O-score, MOM, GP, and ROA) and MGMT (NSI, CEI, Accrual, NOA, AG, and IA). The sample covered the period 1993-2014.

- Do analyst recommendations and changes in recommendations contain information consistent with anomaly signals?

- Are analyst recommendations biased with respect to anomaly signals?

- Is the market reaction stronger for sophisticated/unbiased analysts?

- Were the results robust to risk adjustments and alternative explanations?

What are the Academic Insights?

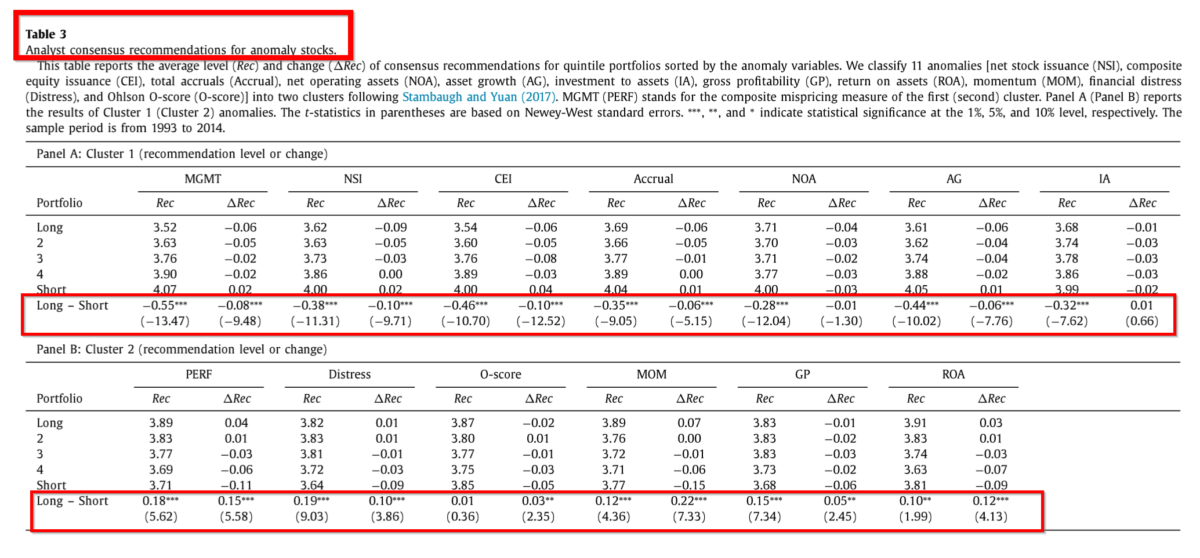

- NO. Analysts more often than not issue recommendations inconsistent and contradictory to the predictions of anomalies, especially for those related to equity issuance and investment. The long/short spread for the MGMT composite was -0.55, significant at 1%. More specifically and as shown in Panel A of Table 3 below: stocks on the short side had more favorable recommendations than those on the long side. For MGMT, the value of the recommendation for the shorts was 4.07 and 3.52 for the longs. Similar results were found for all but 2 of the anomalies included in the MGMT composite. The data tells a difference story for the PERF composite. Analyst recommendations were consistent with anomaly predictions for the PERF anomalies, with the value for the short side at 3.71 and 3.89 for the long. Although this represents a significant result, it is small when compared to the MGMT anomalies. Results did not change when the authors examined changes in recommendations. For MGMT anomalies, upgrades were more likely for stocks on the short side and downgrades were more likely for stocks on the long side. For the MGMT composite, the value for upgrades was 0.02 and 0.06 for downgrades, with the difference significant at the 1% level, although economically small. Apparently, analysts are quite active in revising their recommendations on anomaly stocks, however, the change in opinion is opposite of that predicted by the anomalies. WEIRD huh?

- YES. The alphas from L/S portfolios are larger for portfolios for which analyst recommendations are contradictory to the anomaly predictions, especially for anomalies in the PERF composite. The L/S PERF composite returned a risk-adjusted alpha of 1.57% for the contradictory case. The L/S PERF composite returned an alpha of 0.90% for portfolios formed for recommendations that were consistent with anomaly predictions. The difference of 0.67% between the two types of recommendations (inconsistent vs. consistent) was significant at the 1% level. Individual anomalies performed similarly to the composite, in the range of 0.43% to 0.65%, all significant. The picture for anomalies in the MGMT composite is very different. The alphas between consistent and inconsistent portfolios are small, positive, and are not significant. There were 2 exceptions: Accruals returned a difference of 0.54% and 0.52% for IA, both significant. For both PERF and MGMT anomalies returns from the short side of the inconsistent portfolios were amplified.

- YES. The authors develop and test a method for identifying “sophisticated and unbiased”, i.e. skilled analysts. Please refer to the paper for a description as it is beyond the scope of this summary. In any case, the research shows that skilled analysts who exploit anomaly predictions in the recommendations is a very small set of all analysts. They tend to be sell-side analysts who use quantitative research and elicit stronger returns around announcement of recommendations. As a result, those stocks followed by skilled analysts of this sort have muted anomaly returns, but are not sufficiently followed such that the return predictability is eliminated entirely.

- YES. The authors find that results hold for 6 other prominent anomalies including idiosyncratic volatility, maximum daily returns, part 12-month turnover, cash flow duration, losers minus winners, and market beta and were robust to firm size, institutional ownership, investor sentiment and 3-factor risk adjustments.

Why does it matter?

This research clarifies the relationship between analysts and predictable returns of anomaly stocks and buttress the argument that analysts are likely important contributors to mispricing in the equity markets and help explain the persistence of the returns from anomalies in the equity market. Apparently analysts do not make full use of information provided by anomaly signals and frequently contradict them. In other words, if you want to be the genius analyst on wall street, screen for anomalies first then write your research. Of course, the time period is a bit dated at this point. Because of the massive shift from active to passive and from discretionary to systematic, it would be interesting to see how things have changed since 2014.

The most important chart from the paper

Abstract

We examine the value and efficiency of analyst recommendations through the lens of capital market anomalies. We find that analysts do not fully use the information in anomaly signals when making recommendations. Analysts tend to give more favorable consensus recommendations to stocks classified as overvalued and, more important, these stocks subsequently tend to have particularly negative abnormal returns. Analysts whose recommendations are better aligned with anomaly signals are more skilled and elicit stronger recommendation announcement returns. Our findings suggest that analysts’ biased recommendations could be a source of market friction that impedes the efficient correction of mispricing.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.