The Returns to Private Debt: Primary Issuances vs. Secondary Acquisitions

- Douglas Cumming, Grant Fleming, and Zhangxin (Frank) Liu

- Financial Analysts Journal

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

The subject of private debt and its associated performance characteristics has not been covered sufficiently in the academic literature. Relatively few research articles have attempted to characterize the returns and risk on the types of private debt strategies available to investors. This is true, in spite of the position private debt holds as the dominant source of capital for private firms in the US and across the world.

In this research, the authors constructed “by hand” data on 443 private direct loans made by specialist credit investment funds in 13 Asia-Pacific markets that occurred between 2001 and 2015. Special attention was paid to the representativeness of the sample. Countries included China, India, Australia, and Indonesia which helped to ensure diversity in legal systems, economic systems, size, and age of the associated credit market. There is, however, an important caveat with respect to the data. The authors note that the total track record is collected for each manager, however, some are unable or do not actually raise funds. Therefore, the data likely imparts a positive bias to the distribution of fund managers. In any case, the research is notable in that it does contain insights into the private debt market despite the potential bias.

- Should bond investors consider expanding their opportunity set to include the acquisition of private debt on the secondary market?

- Is the performance of private debt, whether buy-and-hold in the primary issuance market or acquired in the secondary market superior to public credit?

What are the Academic Insights?

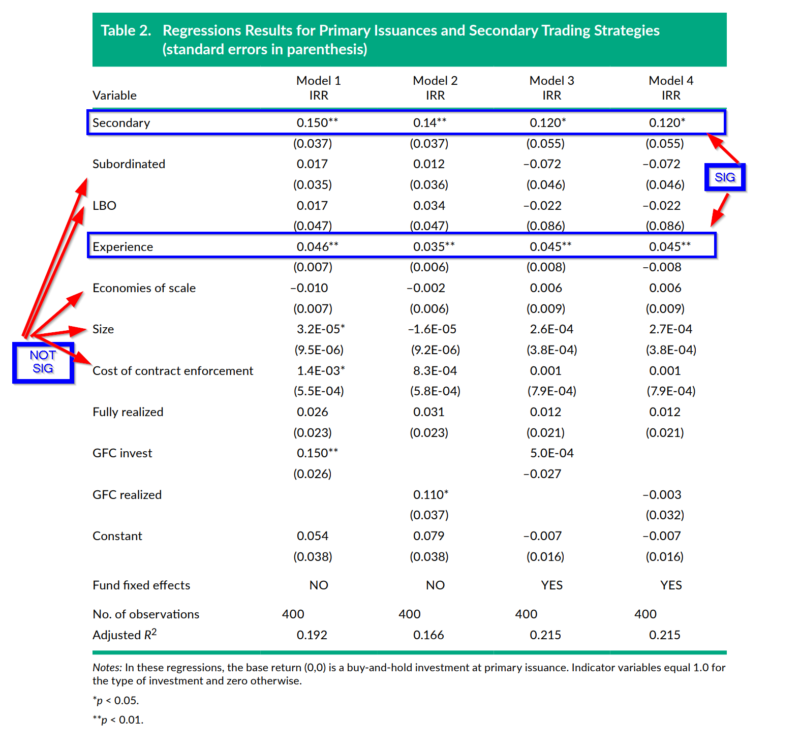

- YES. Returns are higher in the secondary debt market. In a primary issuance, the manager participates in setting the price, covenants, collateral, information and control rights as well as other nonprice terms of the debt. In a secondary acquisition, credit fund managers purchase a private loan in a deal typically brokered by an investment bank. A stark contrast, with no opportunity to manage the credit risk of the loan. This hypothesis was confirmed in the empirical tests of the differences between the two strategies. Secondary trading generated returns in excess of those to the primary issuance alternative. The results were statistically significant after controlling for the effects of the global financial crisis, quality and cost of the legal system, manager experience, economies of scale for the fund family, size of the fund itself, and subordinated or LBO status. Note the following empirical findings reported in the Chart below: The coefficient on “secondary” is positive and significant for all models tested. This indicates secondary strategies earn higher returns than primary issuances; The coefficient on LBO (where LBO represents private equity ownership) was not significant, indicating no difference between returns for LBO and non-LBO structures; Manager experience was significant and positively related to returns; There was no relationship between returns and fund manager economies of scale, size, and cost of contract enforcement.

- YES and NO. The authors construct a private credit return index from the data (including both primary and secondary issuances) and calculate an excess return index using traditional public credit (JPMorgan Asia Credit Index) and equity indexes (MSCI-EM, R3000, SP500). Although the results suggest that the private credit return index outperforms both public credit and equity indexes, these results are subject to a considerable bias associated with the use of IRRs in this context. I would consider them to be unreliable when compared to market-based returns.

Why does it matter?

The takeaway from this research comes from the demonstrated potential to add value in terms of risk and return that is available in the Asia-Pacific private credit markets. The freedom to take advantage of this potential is subject to the due diligence constraints present when investors seek out other sources of credit outside of the US. To my knowledge, this is the first article to supply an empirical rationale for lowering the bar for specific credit fund managers. If an experienced fund manager invests in primary issuance strategies only, should they be allowed to acquire debt in the secondary market in these countries? The answer is a qualified yes.

The most important chart from the paper

Abstract

Private debt fund managers invest in debt positions of private companies through (1) new issuances or (2) secondary acquisition of loans. In the study reported here, we used data from more than 400 investments in private companies in 13 Asia-Pacific markets between 2001 and 2015 to examine which strategy performs best. Conditional on market and industry factors, trading private debt delivers higher returns than buying and holding a primary issuance. So, institutional investors should permit fund managers the flexibility to trade. Furthermore, a portfolio of private debt investments delivers excess returns to public markets over time, with excess returns affected by volatility, funding liquidity, and the global financial crisis. An investment in Asia-Pacific private debt should improve risk-adjusted returns for a global or emerging market fixed income portfolio.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.