Competition for Attention in the ETF Space

- Itzhak Ben-David, Francesco Franzoni, Byungwook Kim, and Rabih Moussawi

- SSRN Working paper

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

This article supplies a testable framework for making sense of the rapid expansion of the ETF market over the last 30 years. The authors argue that the ETF market is differentiated into two types of markets or products: broad-based ETFs and specialized ETFs. Based on the theory advanced by Bordalo, Gennaioli, and Schleifer (2016), innovators develop products based on either a price or quality dimension. In the Bordalo model, ETFs are commoditized and competition is based on the ETF offering the lowest fee (index ETFs, smart beta); or quality, where the ETF is distinguished by high fees and distinct ETF features (theme-based ETFs). Essentially, the explosive growth in ETFs is a function of ETF providers competing for market share by advertising a low price OR some unique feature of the ETF other than the price. Fee-conscious investors are attracted to broad-based ETFs because they provide cheap exposure to an asset class. Investors indifferent to fees, but desire exposure to an investment theme promising very high returns are attracted to specialized ETFs. The authors liken the situation to “Walmart” vs. “Starbucks”. So, does the theory fit the actual ETF market? Yes and No. The empirical results indicate that this characterization of the ETF market is spot on for broad-based ETFs, but less so for the specialized group. A review of the empirical results tells the story.

Note: If you attended this year’s Democratize Quant, you heard a great back and forth discussion between the authors and Jay Jacobs.

What are the Academic Insights?

- There was quite a bit of empirical evidence of segmentation in the ETF market along the lines of price which was consistent with the notion of “competition for attention” explanation. This framework is also consistent with traditional views of financial innovation wherein innovative products are responsive to the rational investor and improve investor welfare. Broad-based ETFs increase the ability to access portfolios that reduce the risk of exposure to an asset class at a low fee. Cheap diversification plus cheap hedging equates to improved welfare. Unfortunately, the results suggest that the same story does not fit specialized ETFs. They are certainly not diversified and only attract investors because they offer exposure to a specific theme, usually at a high price. Over the period studied (2000-2019), 2 clusters of ETFs were observed. Broad-based ETFs, with very similar characteristics and low fees, emerged early in the industry. Late in the period, specialized ETFs proliferated with differentiated characteristics and much higher fees which allowed for multiple types of funds to exist even with smaller AUM. Revenues for broad-based vs. specialized funds were generally equally distributed with the exception of the very far right tail of the distribution, where large players generated significant revenue due to their sheer size. State Street and SPYs come to mind.

- Unfortunately, the results suggest that the same story on pricing or fees does not fit specialized ETFs. Remember that they are undiversified and only attract investors because they offer exposure to a specific theme. The decline in fees in broad-based ETFs was not matched in the specialized segment. As the themes were highly differentiated, there appeared to be little competition among new and old specialized ETFs with little pressure on fees as a result. Indeed, results of regression analysis indicated little to no sensitivity to fees with respect to fund flows into specialized ETFs. However, the sensitivity of flows to past return performance was significantly higher for specialized vs broad-based ETFs. Indicating that performance chasing is happening in the specialized segment of the ETF market.

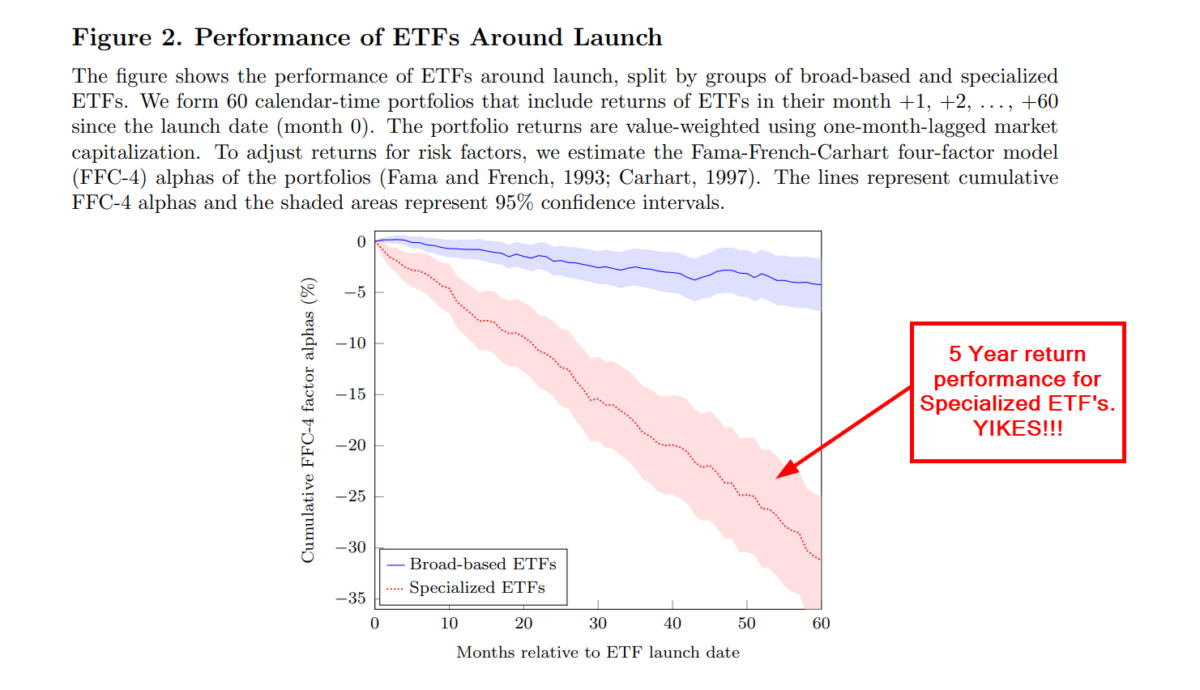

- However, the story with respect to quality (special features) and specialized ETFs is quite different. To their credit, the authors spend quite a bit of time exploring alternative explanations for the role of specialized ETFs. However, the case for quality (high fee, distinct feature) dimension for specialized ETFs is pretty bleak. Performance is poor. On a risk-adjusted basis, the authors report an alpha of approximately -3.1% per year, regardless of the risk model employed. Given the average fee is .55%, the negative performance remains unexplained by those costs. In contrast, the negative alpha exhibited by broad-based ETFs (-.05%) is roughly equivalent to the fees charged. Further, the authors are unable to muster any evidence that specialized funds act as insurance or hedging products as alternative explanations for their existence. To add insult to injury it also appears that investor enthusiasm, as measured by fund flows into the product, begins to ebb significantly during the post-launch period when persistent negative performance occurs. So why do specialized ETFs exist and produce such disappointing performance? The authors conclude that they bear more than a passing resemblance to the Glamour stocks of Lakonishok, Schleifer, and Vishny (1994). The “Overextrapolation” hypothesis developed and analyzed in the LSV article is rooted in sources of behavioral biases exhibited by the average investor and appears to be a better explanatory theory for specialized funds. That explanation does make some sense and if you haven’t read the LSV piece yet, it’s highly recommended.

Why does it matter?

The article is interesting in that it provides analysis suggesting that the rise of broad-based ETFs makes theoretical sense in the context of the demand for low-cost, diversified portfolios that provide exposure to various asset classes. However, the argument falls apart when it attempts to explain the surge of specialized ETFs later in the financial innovation cycle. It’s not quality, it’s not performance, it’s not diversification, and it’s not insurance. But it might be another example of a behavioral bias exhibited by ordinary investors. Perhaps providers are simply capitalizing on those unfortunate tendencies? Of course, a counter to this argument is that a relatively diversified professionally managed thematic ETF is a lot better for an investor relative to “stock-picking” in their Robinhood account.

The most important chart from the paper

Abstract

Exchange-traded funds (ETFs) are the most prominent financial innovation of the last three decades. Early ETFs offered broad-based portfolios at low cost. As competition became more intense, issuers started offering specialized ETFs that track niche portfolios and charge high fees. Specialized ETFs hold stocks with salient characteristics—high past performance, media exposure, and sentiment—that are appealing to retail and sentiment-driven investors. After their launch, these products perform poorly as the hype around them vanishes, delivering negative risk-adjusted returns. Overall, financial innovation in the ETF space follows two paths: broad-based products that cater to cost-conscious investors and expensive specialized ETFs that compete for the attention of unsophisticated investors.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.