The Persistence of Fee Dispersion among Mutual Funds

- Cooper, Halling and Yang

- Review of Finance, 2021

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

Elton, Gruber, and Busse (2004) as well as Hortacsu and Syverson (2004) suggest that mutual fund markets are not perfectly competitive and that fees do matter to investors. In contrast, the neoclassical view of mutual funds (see for example Berk and Green, 2004; Pastor, Stambaugh and Taylor, 2019 and others) implies that fees do not matter because with competitive markets and rational investors, in equilibrium, as fund size adjusts due to investor flows, gross-of-fee alphas will be on average equal to fees, and average net alphas will be zero.

This paper focuses on the investors’ perspective and asks the following research questions:

- What does the data show? Fees do or don’t matter to investors?

- If fees do matter,

- What is the Fee dispersion across funds?

- What is the competitiveness of mutual funds?

- Is too much capital allocated to funds?

What are the Academic Insights?

By studying a rich empirical sample of U.S. and International Mutual Funds from 1980 to 2017, the authors find:

1. YES- While the average alphas are indistinguishable from zero, they hide important fee-related cross-sectional variation among funds. In fact, the analysis shows a systematic cross-sectional relation between fees and net alphas and suggests that, from an investor standpoint, fees do matter, and have important investor wealth implications.

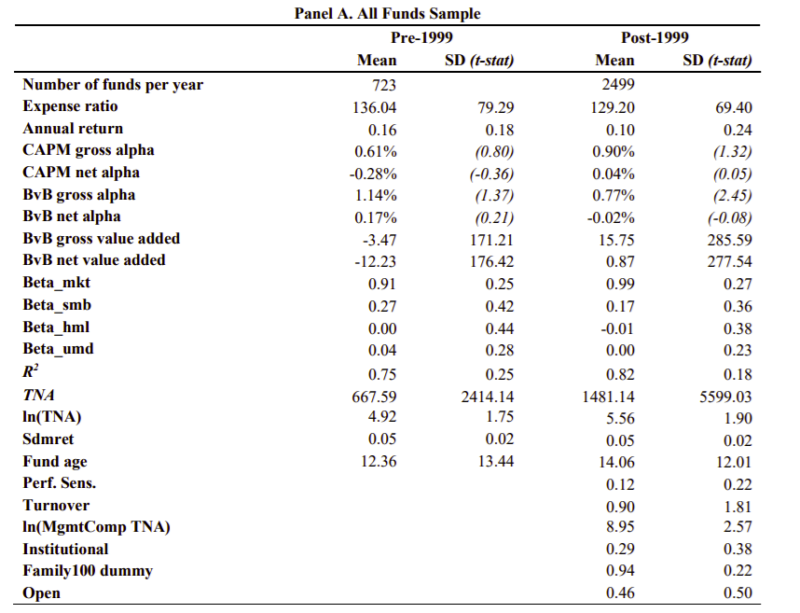

2.1. There is a large level of fee dispersion across similar S&P 500 index funds ( the average interquartile spread in

reported annual expenses is 23 bps while the 10th–90th percentile spread is 47 bps and numbers are higher for the most recent 15 yrs- 30 and 61 bps respectively)! Additionally, when looking at mutual funds the dispersion is higher ( 48 and 97 bps respectively). The phenomenon of fee dispersion is very persistent across time

2.2. Low-fee funds tend to have positive net value-added while high-fee funds have negative net value-added, suggesting, again, a systematic relation between net value added and percentage fees. HOWEVER, in aggregate, the total net value added for the “All funds (Index + Mutual)” sample amounts to a negative $125 billion USD. This number can be interpreted as a measure of the total economic value added or lost by the mutual fund industry for its investors. OUCH!

2.3. Following Zhu (2018)‘s methods to determine the optimal size of each fund based on its alpha, the first dollar invested, and diseconomies of scale, the authors found that 70% ( an estimated $1.4 trillion USD) of the sample are overinvested ( based on the notion of misallocated capital by Zhu, 2018). However, on average high-fee funds are much smaller than low-fee funds indicating that investors do understand that high fee funds oftentimes do not earn their fees.

Why does it matter?

This paper is an important addition to the academic debate on whether fees do or don’t matter for investors. In the words of the authors:

We do not believe that our results conflict with the neoclassical paradigm. Indeed, we view them as complementing the existing empirical evidence. In fact, the average values of neoclassical framework fund manager performance measures like gross and net value added hide ample cross-sectional variation.

For more on the debate of active/passive and who adds value and/or detracts value from the asset management industry we recommend checking out “Is Active investing Doomed as a Negative Sum Game?”

The Most Important Chart from the Paper:

Abstract

Previous work shows large differences in fees for S&P 500 index funds and other funds, and suggests that investors suffer wealth losses investing in high-fee funds when similar low-fee funds are available. In contrast, the neoclassical model of mutual funds (Berk and van Binsbergen, 2015) argues that percentage fees are irrelevant, as fund size will adjust in equilibrium such that net alphas are equal to zero. We show that fees matter from an investor perspective. We document (a) a strong negative association between net-of-fee fund performance and fees in a sample of all US and international equity funds, (b) economically large, robust, persistent, and pervasive fee dispersion in the mutual fund industry, and (c) important economic effects for investors. During the sample period, the mutual fund industry has generated a total value lost (i.e., a negative net value added) of 125 billion USD, coming predominantly from high-fee funds.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.