A lot of people ask me how I invest my own money, and I am always happy to oblige. But I have never discussed the topic in public (unlike my friend Meb, who has a great post dedicated to the subject). However, this past week Justin and Jack asked if they could grill me on my portfolio for their excellent podcast, “Excess Returns.” You can listen to and/or watch the podcast via the video below.

The video sparked a lot of questions from listeners/watchers, which will be addressed in this post. Below I cover many of the topics discussed in the video interview and add some additional context.

I’d like to point out that nobody should care how I invest: my situation is likely different than it is for most investors:

- As of 2022, I am 42 with 3 young kids (7, 9, and 13) (i.e., I’m “in the growth phase” so I can pay huge bills in the future.).

- I have a high-risk tolerance and use a lot of leverage to enhance capital efficiency. (i.e., I’m more pain-tolerant than most, as evidenced by this and that)

- I have a Ph.D./MBA in finance, I’ve been investing for 20+ years, and I’ve published books/articles on technical financial topics. (i.e., I have an above-average knowledge base).

- I own/operate a vertically integrated asset management firm with large exposure to general market risk.

- My family and I live in Puerto Rico and have a very different tax situation than most. (i.e., I live in a tax haven).

HUGE DISCLAIMER: how I invest is not how you SHOULD invest.

Normal disclaimer: You should speak with a financial professional and your constituents to ensure that the plan you have in place is the plan that works for you. Also, below I provide some names of firms that provide products I find interesting. I do not necessarily use/promote their products in my own investing, and I am not affiliated with any of them in any way — I just find their products interesting.

What are my Investment Goals?

I like to start what the “big blue arrows” of our family’s investment goals.

Avoid having to stress about money and cover the essentials: food, transport, and housing.

I spent my entire childhood and most of my adult life worrying about money and how I would pay for food, transportation, and housing. Being broke sucks, and it’s the main reason why I have always wanted “to get rich.”(1)

Fund any chaos and ensure the long-term survival of our business

We have spent 12+ years building Alpha Architect — and the real fun is just beginning. The last thing I’d want is to get “margin-called” in our business via financial distress. I always want to be in a position to personally backstop our business’s balance sheet if things got crazy and we entered a nuclear winter in the asset management business.

Float education costs for the kids and fund a reasonable retirement lifestyle

Like everyone else, I have financial responsibilities to my family as the so-called “breadwinner.”

The three key goals above are nebulous, but when I zoom in and think more tactically, I know I have “made it” when the following are achievable:

- Don’t worry about affording nonstop/non-redeye flights.

- Don’t worry about affording healthy food and nutrition.

- Don’t worry about affording exercise/motivation for my family – lessons, gear, etc.

- Don’t worry about affording team/community bbq/MFTF events.

- Don’t worry about affording family adventures/experiences that expand our knowledge and appreciation for life.

What does my portfolio look like?

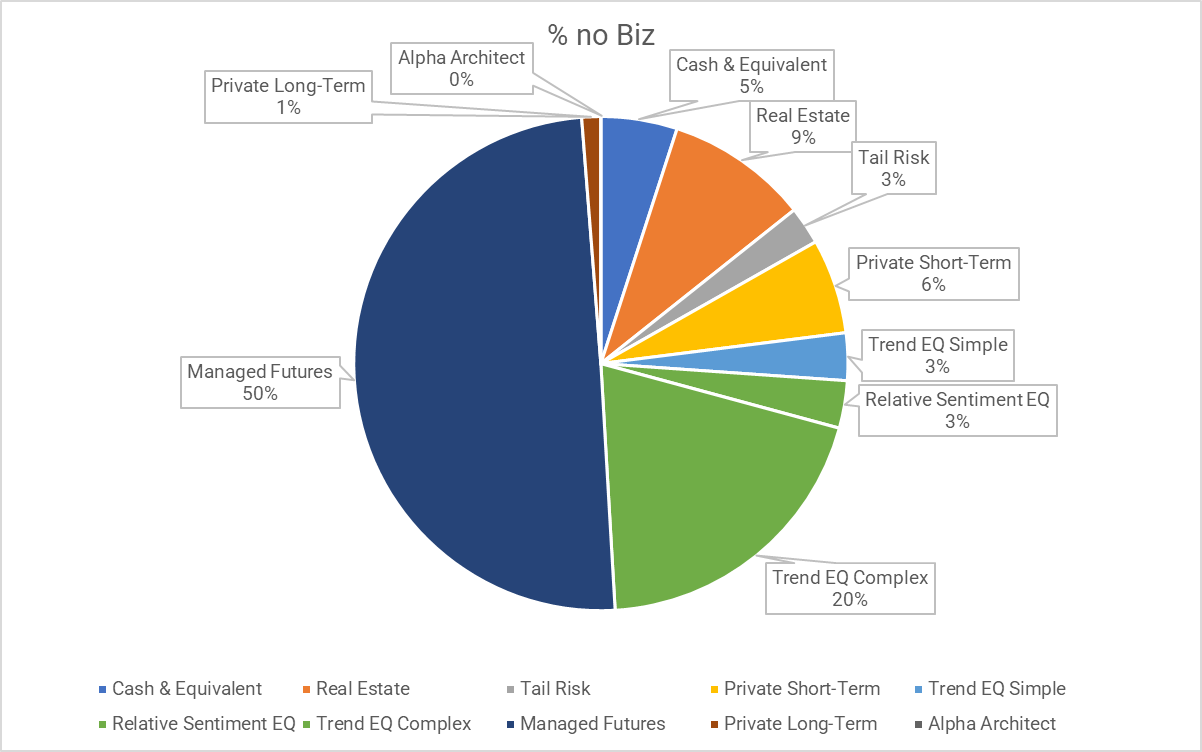

| Asset Class | % W/ Biz | % W/O Biz | Notes |

|---|---|---|---|

| Cash and Equivalents | 1.22% | 4.99% | Liquidity |

| Real Estate | 2.27% | 9.31% | Residence equity (mortgage is ~1/3 value) |

| Tail Risk | 0.61% | 2.48% | MF/ETFs that buy puts, but manage carry costs. Cambria and Simplify have some options in the ETF space. |

| Private credit (Short-Term) | 1.51% | 6.21% | Distress Loans in Puerto Rico (short-term opportunity) |

| Trend Equity (Simple, no leverage) | 0.76% | 3.10% | Global Value Momentum Trend. Pacer, Resolve, and Cambria have ETF options. |

| Relative Sentiment Equity (Simple) | 0.76% | 3.10% | Relative Sentiment Strategy |

| Trend Equity (Complex w/ leverage) | 4.84% | 19.87% | Alpha Architect Long/Short |

| Managed Futures | 12.10% | 49.68% | Bond/Commodity Long/Short (SMA we manage). iMGB, Kraneshares, Dunn Capital, Jerry Parker, and Simplify have options. |

| Private Long-Term | 0.30% | 1.24% | Investments in ETF white-label companies |

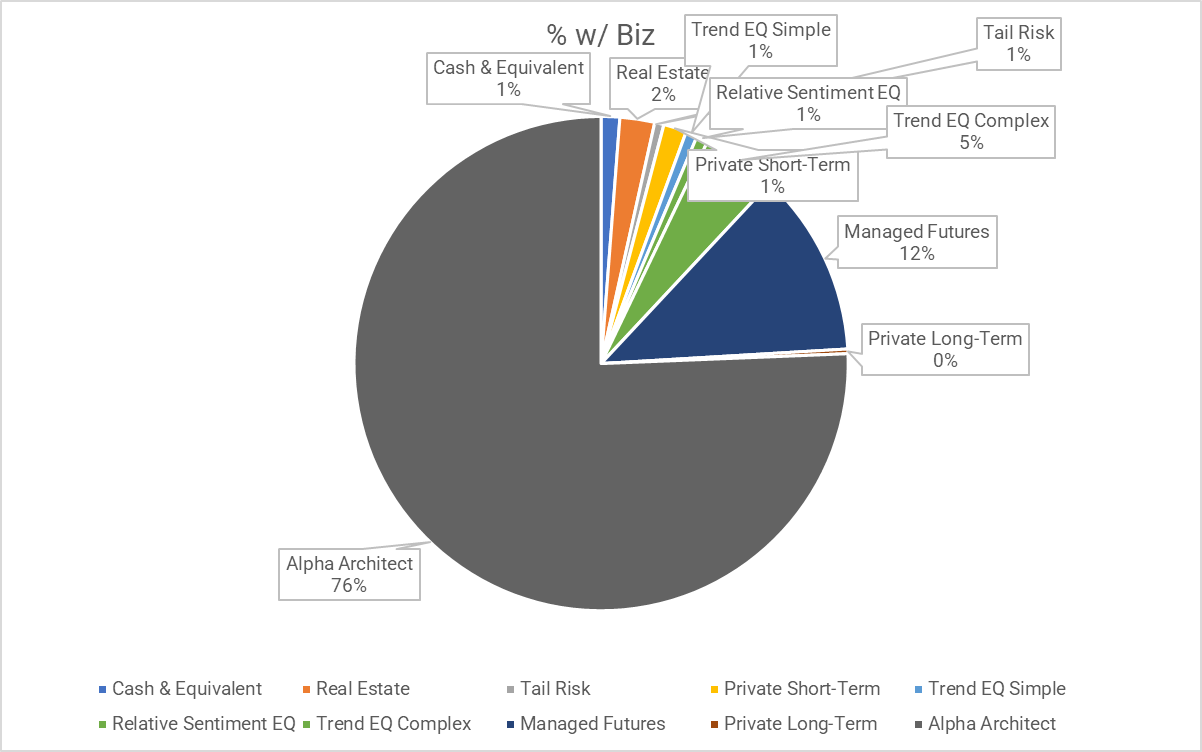

| Alpha Architect Business | 75.64% | 0.00% | Our business (60% owner) |

Visually, you can see my allocations below. Please note that these are based on notional values, not net asset values. For example, the managed futures exposure does not have ~50% dedicated capital allocated. Still, it is, instead, an overlay collateralized by my equity exposures (i.e., what Corey and Invest Resolve refer to as “return stacking”). Also, I have recently added an allocation to “relative sentiment”, which is based on technology developed by my friend, Ray Micaletti. Full disclosure, Ray launched his ETF on our platform, and I am personally invested in Ray’s operating company.(2)

Here is the version that includes my ownership in Alpha Architect:

My interest in our business is by far my largest asset. But in my mind, I mark it at $1 on my balance sheet because capital tied up in equity is not liquid.

The vast majority of my allocations are invested in our products (i.e., lots of “skin in the game”). I currently have a decent slug of capital in short-term private loans because of some unique (and fleeting) opportunities I stumbled upon in Puerto Rico. I foresee that allocation going to 0% in the future, and my goal is to have 95%+ invested in liquid and tradeable investments that are low-cost and tax-efficient. I’m happy to talk tickers/details if you reach out via email.

What Does Retirement look like? Golf all day? Work-till-ya-drop?

Based on my goals, which don’t include Lear jet or yacht ownership, I am already ready to achieve financial victory. But I like our business, I like our team, and I like our mission. Plus, I get to talk to investors and ETF entrepreneurs daily and help them solve problems…as Warren Buffett says, “I tap dance to work each day.” So I’d like to be engaged as long as I’m adding value (i.e., my partners don’t tell me I’m “dead weight”), not suffering massive cortisol spikes, and I’m able to be with my family and maintain a good work/life balance.

At a high level, how would you classify your approach to managing your portfolio?

- Evidence-based

- I try and make decisions and adapt to the world via the scientific method whenever possible.

- Long-term

- Short-term behavioral issues cause the vast majority of the issues for investors. I avoid these like the plague and try and focus on long-term base-rate evidence when making decisions.

- Robust to chaos

- I live in a highly volatile business and therefore need to build a portfolio that can deal with all forms of chaos robustly.

- Skin in the game

- We are in the business of investing other people’s hard-earned wealth. We need to lead from the front and ensure that our constituents know we are rowing an oar in the boat alongside them. Therefore, I invest almost all of my liquid wealth in our strategies. I believe in what we do and put my money where my mouth is.

Appendix: Random thoughts on market topics

Please note that the answers below are high-level summaries, not gospel, and I reserve the right to change my mind and reassess costs/benefits at any time. Plus, these commentaries are based on my own experience and situation, which may not apply to folks with a different experience/situation.

What are your thoughts on bonds and commodities?

In general, I’m not a fan of corporate bonds as a buy-and-hold asset class. Outside of treasury bonds, most bonds earn lower returns than equity, but they act a lot like equity when the world is on fire. And to make matters worse, most of the appreciation is tied to income, which has a terrible tax burden. Could I be convinced in certain situations to invest in non-treasury bond assets? Sure, but I’m not a fan overall.

But let’s talk Treasuries. US Treasury bonds are unique because they still sit in the coveted “flight to safety” asset class (at least, historically, when inflation expectations aren’t high). On their own, treasury bonds are terrible investments, but IF one is convinced they can provide insurance against chaos in your stock portfolio, they can be an incredible diversifier. Fortunately, we’ve looked into the “crisis alpha” aspect of bonds, and the story is mixed. Many insurance benefits tied to treasury bonds are related to high underlying coupons. But if the high coupon rates are gone, you aren’t left with much. Not to mention that the key reason Treasury bonds act like insurance assets is due to their unique position as safe-haven assets. If their status as the liquidity/safety king becomes questionable, their investment merit becomes extremely questionable.

Where does that leave us with bonds?

Well, when in doubt, trend-follow. I can’t predict what treasury bonds will do, but I am a fan of trend-following longer-duration Treasury bond exposures — if they are in a positive trend, own them; otherwise, own cash and cash equivalents. And that’s what I do in my portfolio. Part of our managed futures strategy is investing either long or short in the various government 10-year and 30-year duration bonds around the globe.(3) I have a 0% allocation to static buy-and-hold bonds. That’s crazy, IMHO.

How about commodities? Same as above. No buy and hold — trend-follow only.

Equities have low expected returns right now, given their high valuations. How do you manage this risk?

I trend follow all my equity exposures, and I have no buy-and-hold equity allocations. Is this the right solution for everyone? Probably not, but I have large risk exposure to generic market beta via our business, so I need to be especially aware of this risk. Also, I am wired to trust the process and know that trend following is the epitome of no pain, no gain.

What do you think about using factors in your portfolio?

Factors can be used to shape different risk and reward characteristics. For me, I look to the factors that give me the best shot of earning the highest returns over the long haul, which boils down to the two kings of factors: value and momentum. I’m not going to bore everyone to death on this subject because we have over 1,000 blog posts dedicated to thinking about and understanding factors. But I will say that I am only interested in concentrated factor exposures versus diluted exposures that seek to track closely to the broad benchmarks. I have no interest in tracking a benchmark; my interest is to beat the benchmark over a 20-year cycle and embrace the pain that comes with being different.

With concentrated value and momentum strategies in hand, how do I invest in these exposures? I prefer to spread my bets around the globe, so I end up with roughly 100 deep value/quality names and 100 high momentum names. That equates to roughly a 200-stock global equity portfolio that makes up my entire equity investment. The following blog post outlines how I generally invest in equities, which includes some leverage and tax optimization.

Do you invest in alternatives?

Yep, managed futures (trend following on bonds/commodities) and tail-risk funds.

On the private side, I try and avoid seduction. However, I am currently invested in some private credit deals in Puerto Rico and have invested in one of our ETF white-label operators (might expand this in the future).

Are you tactical at all with your portfolio? Will you overweight certain asset classes or factors when you think they are undervalued?

Only with my retirement account, which contains how much damage I can do to myself. My claim to fame was pulling off trend in March 2020 and going all-in on deep value. (Turns out that call was wrong…should have gone all-in on momentum!)

What do you think about the impact of inflation on your portfolio? Do you change anything for potential higher inflation?

Nope. Already built to manage all regimes and situations that the world could throw my way (I hope!).

Bitcoin?

No comment for fear of retaliation from my Puerto Rican neighbors. But when in doubt, trend-follow.

What do you think about risk when building your personal portfolio?

I am highly tied to beta in our business, so I try and build a portfolio that diversifies and protects against that risk.

As an owner of a company, I would assume you have a large percentage of your net worth in it? How does that impact the construction of the rest of your portfolio?

My ownership in AA is my largest asset, and it is highly tied to ‘beta’ risk, so I try and manage that to a certain degree.

What is something you do with your portfolio that you would not recommend to an average investor?

Private investing. I have special access to ETF white-label operators and also live in Puerto Rico, where there are capital constraints that cause fleeting opportunities. But I keep this type of investing as a small part of my portfolio and would place it in the “fun bucket.”

What do you do in your portfolio that most investors don’t but probably should?

More long-volatility investments like tail risk funds and trend-focused managed futures programs. These asset classes should make up 20-50% of most investors’ portfolios and replace buy-and-hold bonds.

I also decided to move to Puerto Rico under Act 60, which is a bold way to optimize on tax-efficiency and lower my cost of capital.

If you had to impart one lesson you have learned from building your portfolio to the average investor, what would it be?

Know what you own. Keep fees/taxes to a minimum.

Buy cheap; buy strong; follow trends.

What do you think of Rick Ferri?

He’s a former Marine, so I think he’s awesome.

Investment-wise, I am a huge fan of his first principles: keep taxes/fees low and keep complexity to a minimum. Therefore, owning generic Vanguard-centric portfolios is a great idea for many people and will prevent them from doing silly things.

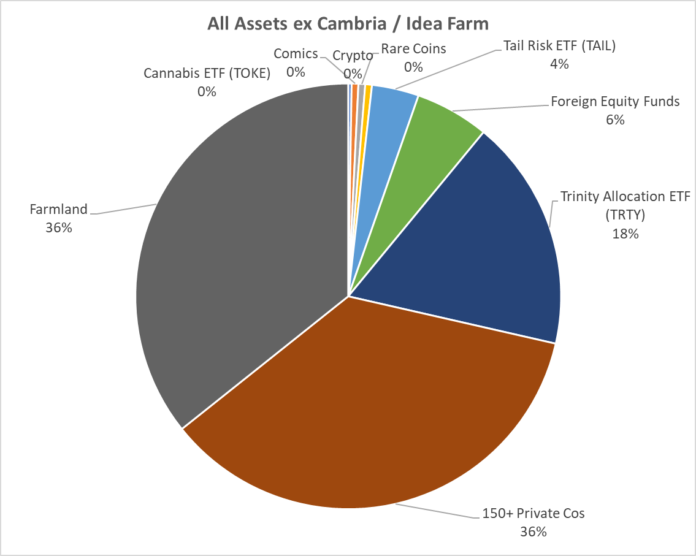

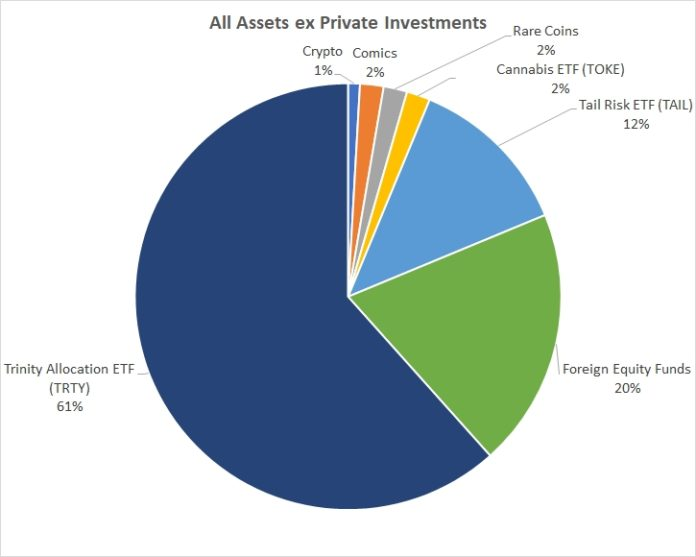

How Do you Compare with Meb Faber?

Here is Meb‘s allocation as of March 2020. He invests a much larger percentage of his wealth in private assets via farmland and underlying startups. But his trinity allocation is roughly similar to what I’m doing on my broader portfolio. Interestingly enough, we are very similar as far as life/investment situations, and yet, our investment portfolios look dramatically different. This is a great way to highlight that investment portfolios are highly customized to the individual investor, and no single portfolio will work for every investor.

References[+]

| ↑1 | I grew up on a ranch in Colorado, and we would flip haybales that came out of the baler. Sometimes they would flip on their side — which would screw up the hay bale stacker when it came by to pick them up. So my dad would send us out there to walk the entire 1,000 acres — back and forth on every single hay bale row — to flip hay bales. It was terrible. I did this from 1-3th grade, every hay season, at 5 cents a bale. I would relentlessly complain.

My dad suggested that the only solution to avoid being out in a hayfield all day was to get smart so people would pay you for your brain, not your brawn. That inspired me to start reading books and learning about ways to make money that didn’t involve manual labor. Lesson learned? If you aren’t born rich — you cannot compound your wealth because you don’t have any wealth. Therefore, you need to compound your knowledge, which is driven by an investment in the only asset we are all born with — our brain housing group.  |

|---|---|

| ↑2 | Ray convinced me that his algorithm was different than trend-following and would serve as a good complement to trend-following. I’m a small buyer but might increase this allocation in the future. |

| ↑3 | You could also keep it simple and trend-follow your favorite intermediate or long-term treasury bond ETF. |

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.