Our friends Corey Hoffstein and Rodrigo Gordillo over at Return Stacked have done some interesting research on the potential for gold to improve your run-of-the-mill 60/40. You’ll need to hit them directly on their site to get their full report. However, I read their very detailed white paper, and I thought the concept was intriguing and worth a look for Alpha Architect readers seeking tactical ideas and diversification opportunities (can the S&P 500 continue to go up forever? Maybe!).

Bottom Line Up Front (BLUF)

If you like your 60/40 but hate the drawdowns, consider adding a modest gold futures overlay on top. According to Corey/Rod’s research, a hypothetical portfolio can improve excess returns and lower drawdowns. Why? Well, gold’s long-run correlations to U.S. stocks and 10-year Treasuries are basically zero (0.01 and 0.07), and layering this asset into your 60/40 mix has made a lot of sense. Of course, if using leverage isn’t your thing, you could always pull some exposure out of your stocks and bonds and allocate it to gold (Google or ChatGPT, “permanent portfolio,” for some ideas in this direction.). You might hurt your expected returns, but you may improve your risk-adjusted portfolio along the way.

Why gold and why now?

For centuries, gold was money with roughly 0% real over ultra-long horizons. Post-August 1971, gold floats and investors demand a risk premium for inflation/currency/policy risk. Early futures had nasty contango, but post-2004 storage transparency and arbitrage tightened the basis—so modern gold futures track spot economics much better.(1)

What do the long-run data say on Gold?

- Performance: Modernized gold total return ~7.35% annualized since 1971—below U.S. stocks, above 10-year Treasuries, well ahead of cash.(2)

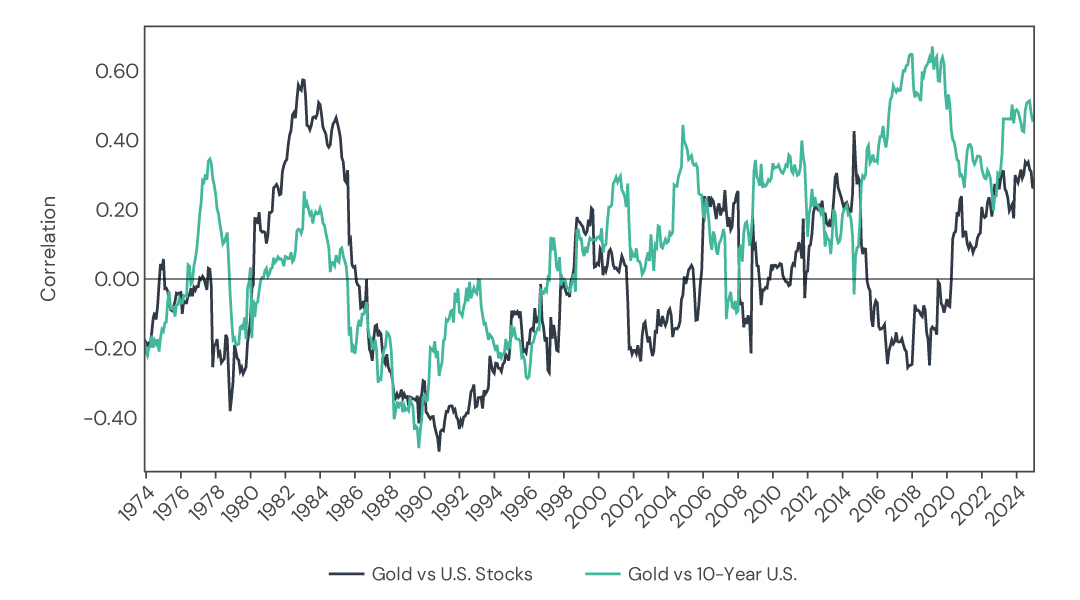

- Diversification: Near-zero long-run correlation to stocks/bonds; tends to help when equities are stressed (“crisis alpha”). For perspective on gold’s mixed but valuable role, see Gold as a Safe-Haven Asset and Does Gold Do What It Is Supposed To Do?

- Macro hedges: Historically likes falling real rates, dollar weakness, and inflation spikes. For inflation context across assets, see Bond Investing in Inflationary Times.

36-Month Rolling Pearson Correlations of Gold with Other Assets (August 1971 – December 2024)

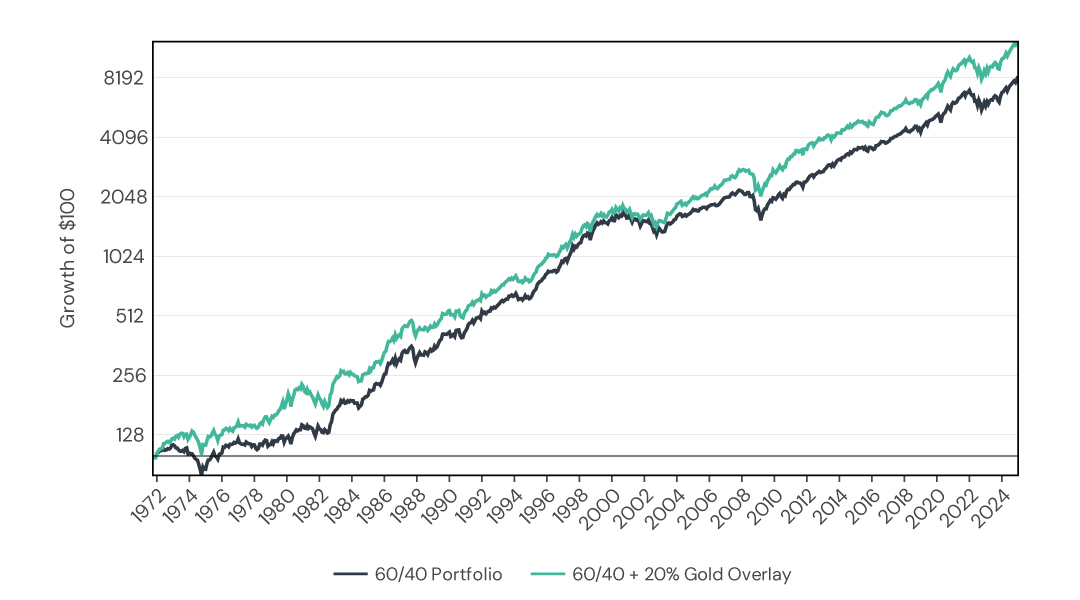

The simple use case: stack 20% gold on a 60/40

From 1971–2024, a 60/40 did ~8.54% annualized. Add a 20% fully collateralized gold futures overlay and you’re at ~9.43%, with similar headline volatility (~10% vs ~10.8%) and an improved max drawdown (~-30% → ~-26.5%). The lift accrues over multiple cycles because gold’s return stream is different—and often shines in left-tail equity events.(3)

Figure 15. Growth of $100 – Traditional vs. Stacked Portfolios (August 1971 – December 2024)

“But what about Bitcoin?”

Are we really talking about gold in 2025? How about Bitcoin, the high-octane, digital cousin—potentially a complement or a replacement for gold? If you believe Bitcoin is another gold-like asset, with highly diversifying properties, then certainly, consider BTC as well. The name of the game in portfolio risk management is diversification.

Conclusion

A traditional 60/40 portfolio of stocks and bonds has been great and can be accessed very cheaply thanks to the ETF market. But one must always ask if the 60/40 is diversified enough. I, personally, don’t think it is, and I’m in favor of adding diversifying exposures to a portfolio—IF—you can get them at affordable prices, with low frictional costs, and full transparency. With a capital-efficient gold futures overlay, you can keep your full stock/bond allocation and still add a return stream that has historically improved compounding, reduced drawdowns, and helped in inflation/recession/crisis regimes. I prefer to trend follow the gold exposure since permanent gold holdings wig me out a bit, but that’s just my opinion. Will Gold continue to work in the future? Only the market gods will ever know.

References[+]

| ↑1 | For broader context on commodities/futures as diversifiers, see our primer: Commodity Futures Investing: Complex and Unique.) |

|---|---|

| ↑2 | From Corey/Rod research. |

| ↑3 | For more on hedging left tails and crisis behavior, browse our Crisis Alpha archive and this classic overview: Strategies to Reduce Crash Risk in Stocks. |

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.