Large language models are increasingly being used to forecast stock prices and guide investment decisions. But what happens when these models cross borders? This paper shows that U.S.-based LLMs, like ChatGPT, systematically produce more optimistic forecasts for Chinese firms than Chinese-based models. The bias isn’t about fundamentals – it stems from asymmetries in media coverage and training data. By unpacking this “foreign bias,” the authors highlight a new source of risk for global investors: AI models may amplify information gaps rather than close them.

We’ve previously seen research on how AI stacks up against human analysts in stock return prediction — see Stock analysis: How does AI perform vs. humans?. The current paper complements that by showing how AI’s predictions also vary depending on geography and media exposure.

When LLMs Go Abroad: Foreign Bias in AI Financial Predictions

- Cao, Wang, Yi

- Harvard working paper, 2025

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

US-LLMs Show Optimism toward Foreign Firms

When comparing ChatGPT (US-based) vs DeepSeek (China-based), the authors find that ChatGPT gives higher end-of-year price predictions and more “buy” recommendations for Chinese firms. This is unexpected- because usually the “home bias” means domestic assets are favored. Here, we see almost the opposite in the AI realm.

Bias Tied to Asymmetric Media Exposure

The bias appears strongest when U.S media silences negative news about Chinese firms, while Chinese media covers them more fully. When ChatGPT sees less negative coverage from U.S. sources, it remains optimistic. The reverse asymmetry is a key mechanism.

Synthetic Control & Prompting Show Missing Data Is Key

The authors construct placebo firms with synthetic data: ones where media coverage is balanced. For those, the optimism gap between ChatGPT and DeepSeek disappears. Also, when you prompt ChatGPT with Chinese-media negative news (even though you can’t change its internal weights), the bias vanishes. That tells us the issue is missing or skewed training data, not model architecture per se.

Diverging Forecasts May Worsen Global Information Asymmetry

Because different countries’ LLMs pick up different biases in training data, financial forecasts for the same firm may diverge depending on which model or language domain is used. That means AI might amplify rather than close information gaps between investors in different jurisdictions.

Practical Applications for Investment Advisors

- Before relying on LLM forecasts, especially cross-border, check which model is used, and what datasets it has been exposed to. A U.S-model may miss negative local coverage; local models may have biases of their own.

- Use prompts or supplement sources: if a U.S-LLM seems overly rosy about a foreign firm, include local news sources (negative and positive) in your prompt to counteract possible missing data effects.

- Diversify model sources: cross-validate predictions from an LLM trained in the target country (or language) to see if there are systematic discrepancies.

- Regulatory and compliance teams should demand transparency about LLM training data, so investors/clients understand what “news exposure” the model had—or lacked.

How to Explain This to Clients

“Imagine two reporters covering the same company. One works in New York, sees mostly rosy headlines, or perhaps doesn’t get access to the critical local press. The other stays in the company’s home country, sees both praise and negative criticism. Their stories will be different. LLMs are like those reporters. If the U.S. model saw less critical Chinese media, it tends to give you a sunnier view of Chinese firms than the China-based model. That doesn’t mean the firm is doing better—it just means the model saw less bad stuff. So use multiple ‘eyes’ to judge.”

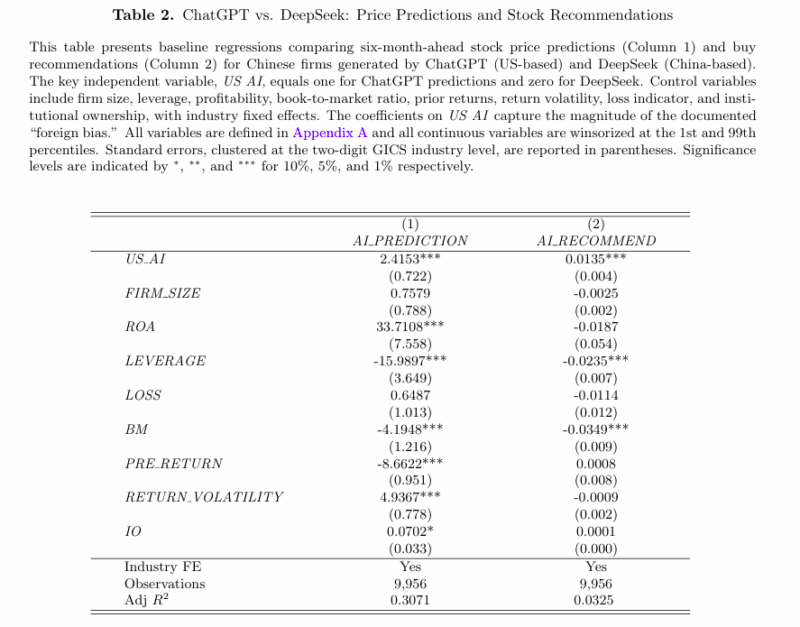

The Most Important Chart from the Paper

TABLE 2: ChatGPT vs. DeepSeek: Price Predictions and Stock Recommendations

This chart plots the difference between ChatGPT’s predicted end-of-year stock price (or “buy” recommendation rate) vs DeepSeek’s, across Chinese firms. It shows that when U.S. media coverage of negative events is lower (relative to Chinese media), this gap widens significantly. Once negative Chinese news is added to prompts, the gap collapses almost fully.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

We document foreign biases in AI-generated financial predictions: ChatGPT (US-based) is systematically more optimistic about Chinese firms than DeepSeek (China-based), predicting higher end-of-year stock prices and generating more buy recommendations. This AI-specific phenomenon contradicts the traditional home bias in which investors favor domestic assets. We trace this bias to differential information access: ChatGPT’s optimism increases when US media coverage of Chinese firms’ negative news is scarce relative to Chinese media. Supporting this mechanism, placebo tests with synthetic Chinese firms without such asymmetries show no prediction gap between models. Crucially, providing ChatGPT with Chinese news through prompts-which cannot alter model weights-completely eliminates the prediction gap, demonstrating that the bias stems from missing training data. Our findings imply that the parallel development of LLMs in different countries can create divergent financial forecasts, potentially amplifying rather than reducing cross-border information asymmetries as these tools shape investment decisions globally.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.